Op-ed: The paradigm shift in critical mineral investment –Tungsten is just the beginning.

Every critical minerals strategy today is built on a massive, expensive assumption: If governments invest enough money into processing, refining and domestic supply chains, eventually they’ll catch up (and maybe even out-compete) with China.

I’ll say it plainly, that approach will not work.

The Ecosystem Problem

Look at the tech sector. Imagine trying to launch a new search engine to compete with Google today. Technically, it’s possible. Given enough money, engineers and infrastructure, you could probably build something just as good.

But would you? Of course not. Because Google didn’t become dominant simply by building a better search engine. It became dominant by building the ecosystem first. By the time everyone else realised how valuable that position was, the market had already evolved around it.

Yet, as logical as this sounds at face value, this is the exact strategic mistake Western governments are repeatedly making in the global race for critical raw materials (CRMs). Policymakers assume that supply chains can simply be systematically dismantled and rebuilt through diversification, reshoring and investment, failing to recognise when a race is already functionally over.

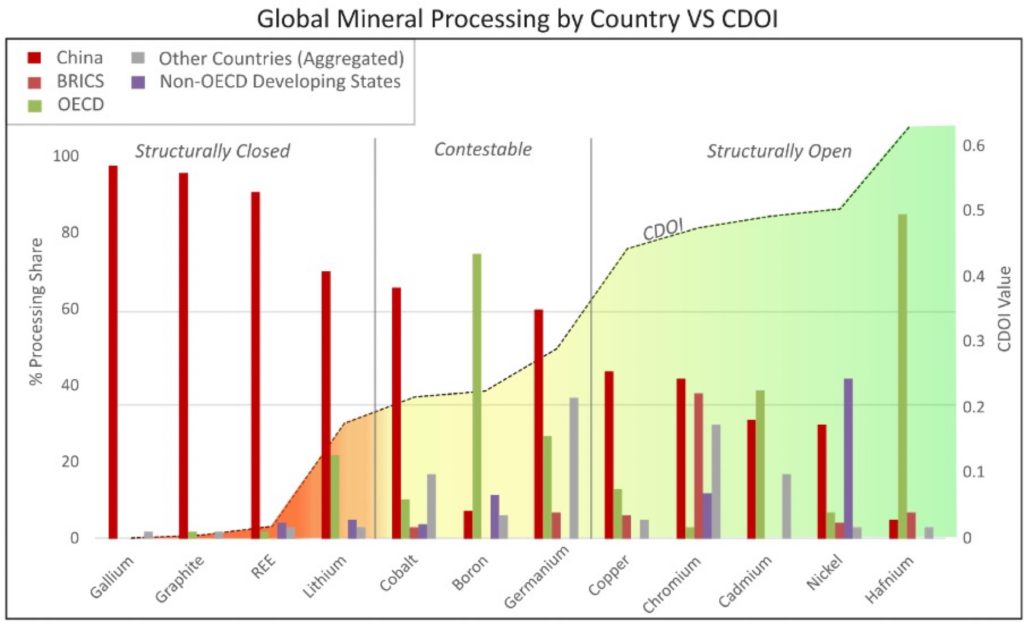

Simply put, some markets eventually reach a point where they become structurally closed. New entrants can still build capacity, but displacing them becomes progressively more expensive, less profitable and strategically less meaningful.

In other words, there comes a point where it is no longer economically rational to invest in certain midstream market, and that doing so becomes an expensive lesson in path dependency. It forces Western capital into a continuous cycle of playing catch-up, giving dominant players like China the necessary headroom to quietly monopolise the next generation of commodity value chains.

This is where much of the current debate falls short. We tend to think of processing as a collection of individual plants that can simply be replicated elsewhere. In reality, processing dominance is an ecosystem, built on decades of experience and integrated supply chain logistics. By the time a country controls most of a processing market, it has usually accumulated thousands of small competitive advantages that are extraordinarily difficult to recreate.

Calling it “critical” doesn’t make it feasible

To bridge this analytical blind spot, we must look beyond current market concentration and apply a new metric. This is the Critical Dominance Opportunity Index (CDOI). Rather than taking the typical approach to investment by measuring where processing is concentrated today, it asks a different question:

How much room is actually left for new players to successfully enter a market and build strategic leverage?

When seen through this lens, the realities of the global transition become starkly visible. The processing markets for elements such as gallium, graphite, rare earth elements, and even lithium are already structurally closed. China isn’t just the largest processor, it occupies a midstream position that cannot logically be broken. Could Europe or the United States still build processing plants? Absolutely, but could they realistically overturn China’s position? That is a very different question.

On the other hand, despite having visually intimidating market shares held by single nations, the midstream markets for base metals such as copper, nickel and chromium remains comparatively open. No single global actor has yet achieved overwhelming control. The double-edged reality, however, is that whilst these markets are open to Western positioning, they are equally vulnerable to hostile monopolisation if left ignored.

Then lies the institutional blind spot, and arguably the most interesting area: a market that appears securely closed, until it suddenly isn’t. Markets like hafnium and boron appear protected because they are dominated by OECD nations, but that dominance is an illusion that is entirely dependent on institutional coordination across allied countries. Simply put, if cracks emerge within that coordination, a backdoor opens for strategic competitors to rapidly buy up control.

This distinction fundamentally shifts the paradigm. For the past decade, governments have largely obsessed with identifying which minerals are “critical”, but that is only half the story. The more important question is: which critical minerals remain strategically contestable? These are not the same. One measures today’s dependence, whilst the other measures tomorrow’s opportunity.

The €10 Billion Shift

The solution lies in how we classify “critical”. We tend to treat all critical raw materials as equally actionable. But they’re not. Some markets still have room for new dominance to emerge, and others don’t. That distinction matters.

Imagine two governments each investing €10 billion into refining capacity. One chooses gallium. The other chooses nickel. On paper, both have invested in strategic minerals. In reality, they have made completely different bets. In gallium, they are entering a market where structural dominance has already crystallised. They may improve domestic resilience, but they are unlikely to reshape global market power and remain vulnerable to market shifts beyond their control. In nickel, however, the market remains structurally contestable. The same investment has a far greater chance of creating genuine long-term strategic leverage.

That is why measuring contestability matters. It helps distinguish between investments that improve resilience and investments that can genuinely reshape future market structure. Both have value, but they should never be confused with one another.

China appears to have figured this out. We can see the risk of ignoring this logic in the tungsten market. The midstream processing market (CDOI) for tungsten is effectively closed, comparing well with graphite. But whilst Western nations have failed to recognize this, China has mapped it out perfectly, aggressively campaigning to monopolise the circularity frameworks and secondary processing of tungsten waste streams.

Why would the world’s dominant tungsten processor suddenly become interested in industrial waste? Because they recognise that when a primary processing market is structurally closed, the next contestable frontier automatically becomes secondary supply. China isn’t changing strategy. It is extending exactly the same strategy that built its original dominance. Control every remaining pathway through which future leverage can be created.

If they succeed, they will secure absolute, closed-loop control over the entire global tungsten value chain, from raw extraction to downstream recycling.

A New Architecture for Industrial Policy

This is where contemporary Western industrial policy makes its most costly mistake. Much of today’s geopolitical discussion still revolves around “catching up”. But catching up assumes the race is still being run. In many markets, it isn’t.

Pouring billions into structurally closed processing markets might improve local resilience, or create domestic jobs, but it does so at an unsustainable opportunity cost. It demands permanent capital subsidies to survive and leaves fewer resources available to compete where genuine opportunities still exist.

That doesn’t mean governments should abandon these markets. Resilience, recycling and strategic stockpiling do matter. But defensive resilience should not be mistaken for competitive advantage. There is an important difference between reducing dependence and building dominance, and successful critical minerals strategies need to recognise when each objective is appropriate.

If the US, EU, and wider OECD bloc proactively adopt a structure-aware approach, it will fundamentally transform the mining and investment landscape. The implications here are profound. If governments begin focusing capital according to contestability rather than simple criticality, today’s investment landscape changes dramatically. Projects targeting already-consolidated processing markets may continue attracting public funding for resilience, but they are less likely to reshape global market power. Meanwhile, companies positioned within still-open markets could suddenly find themselves aligned with an entirely new generation of industrial policy. In other words, the next mineral winners may not be those producing the most fashionable critical minerals, but those operating in the “dull” markets that remain open.

But to do this, we must first accept a harsh dose of realism. We must acknowledge where the race has already been lost, so we can focus capital on where the greatest gains are yet to be made. This is not an admission of defeat, but a tactical recognition of reality. If we can do this, the change will be significant. Capital will stop blindly chasing the same handful of over-saturated, “obvious” battery metals, Policy will become ruthlessly selective, and industry will pivot toward massive, currently under-recognized value chains.

Because strategy has never been about stubbornly trying to win every race, but rather about recognising which races are still worth running.

Bio

Dr. Nicholas Vafeas is an economic geologist specializing in critical raw materials, mineral value chains, and strategic resource investments.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments