Coal, gas lead 2022 commodities rally

Coal and natural gas markets were poised on Friday to end 2022 with strong gains after a global energy crisis triggered by the Russia-Ukraine war stoked prices, and tighter supplies expected in 2023 could fuel more gains.

Industrial metals, iron ore and rubber are on track to finish in negative territory, pushed down in 2022 by China’s strict zero-covid policy and fears of a world recession.

Agricultural markets, including grains and palm oil, jumped to all-time highs in March on adverse weather and pandemic-related supply disruptions, triggering food inflation, but those commodities gave up much of their gains in the second half.

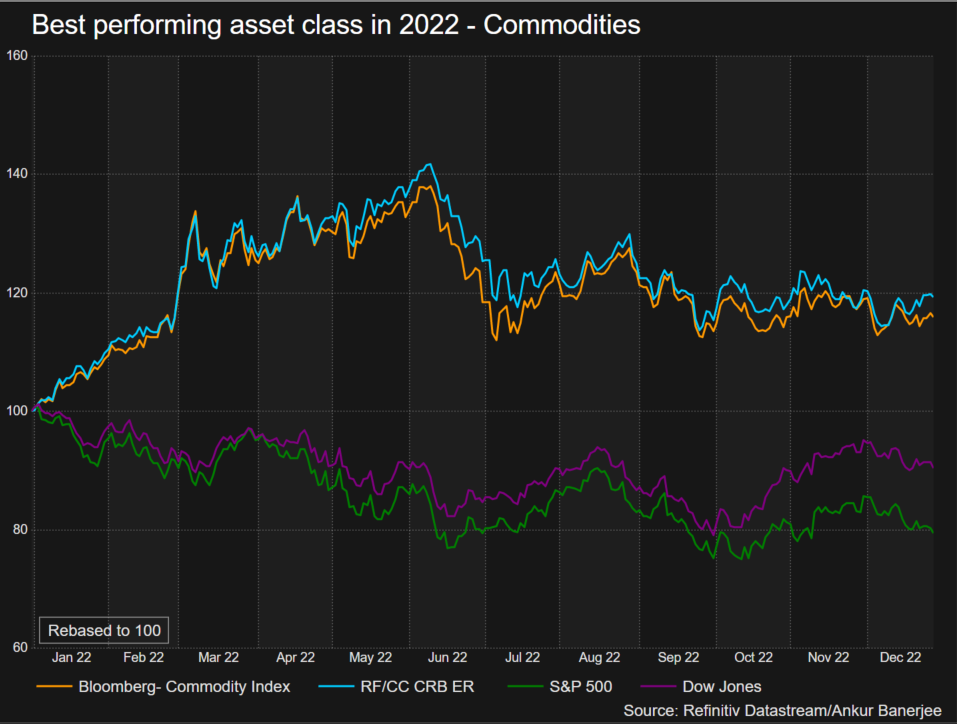

“Despite the recent price declines, commodities will still likely finish the year as the best performing asset class,” Goldman Sachs said in its 2023 commodity outlook.

“From a fundamental perspective, the set-up for most commodities next year is more bullish than it has been at any point since we first highlighted the supercycle in October 2020.”

Supply strain

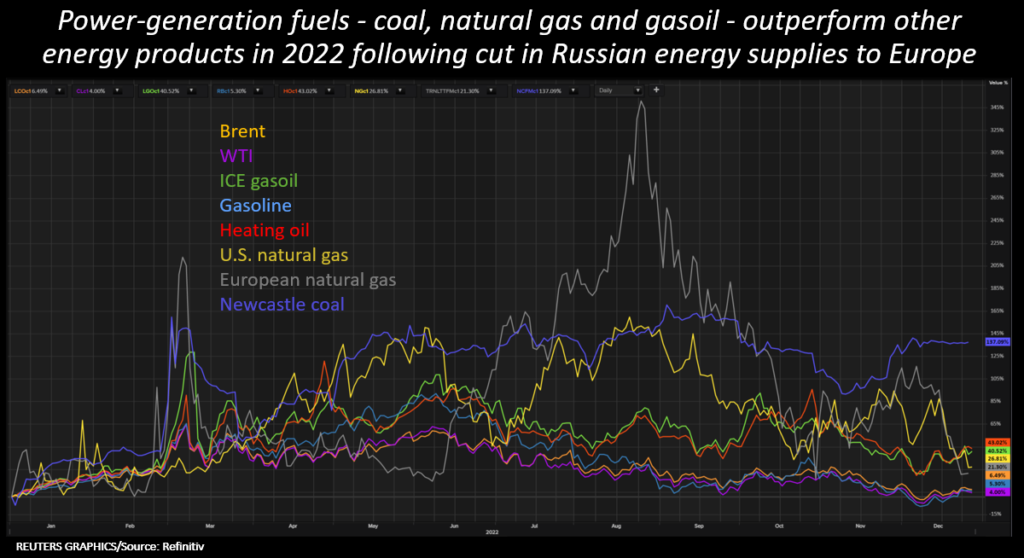

Global gas markets were roiled this year after Russia cut supplies to Europe and a major pipeline was damaged amid the war in Ukraine, leading European countries to import record volumes of non-Russian gas to ensure winter supplies.

The additional demand for liquefied natural gas (LNG) and tighter supplies of piped gas placed enormous strain on the global market, spurring an energy crisis that pushed gas prices to historic highs.

Newcastle coal futures have soared almost 140% in 2022, the biggest jump since 2008.

In the European market, the benchmark Dutch front-month gas contract was poised to end 2022 almost 8% higher but has plummeted around 75% from record highs seen earlier in the year after Europe successfully built up gas stocks.

US gas futures jumped by more than 20% and Dutch wholesale gas prices rose by almost 8%, both rising for a third consecutive year.

Because Europe will continue to import LNG to rebuild gas inventories next year after winter, gas prices are expected to remain elevated as limited new supplies come onstream.

The dismantling of tight pandemic controls in China, the world’s second-largest LNG importer, could also promote economic recovery and greater LNG consumption next year.

However, a European cap on gas prices starting in February could keep a lid on the market and reduce the volatility seen this year.

Oil prices are on track for a second annual gain, with Brent up almost 6% and US crude rising nearly 5%.

Brent oil futures have risen above $139 per barrel earlier in 2022, not far off their all-time high seen in 2008, but have since dropped to around $85 per barrel on a weaker economic outlook and modest Russian export disruptions.

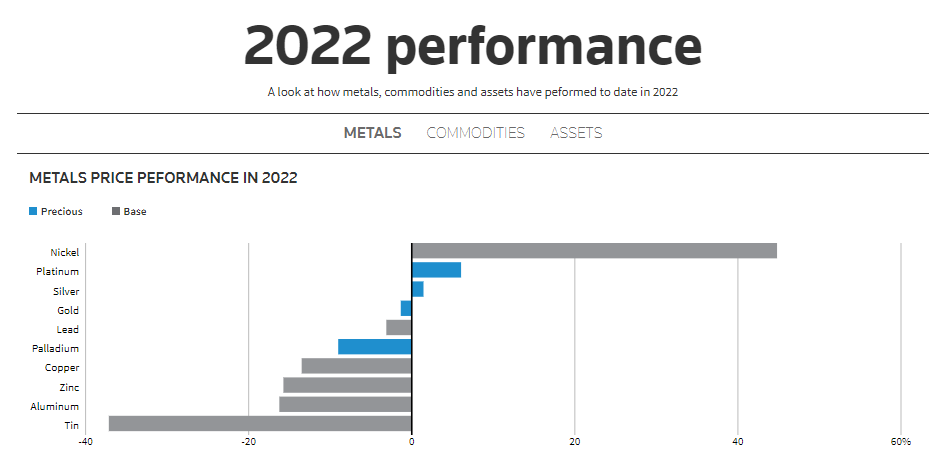

In industrial metals, copper on the London Metal Exchange is on track to fall 13% this year and aluminum is down about 15%. Both reached record highs in March.

Spot prices of iron ore bound for China , which consumes about two-thirds of global supply, have fallen about 5% this year, ending near $115 per tonne.

Citi analysts are bearish on nickel and zinc for the next six to 12 months, seeing strong supply growth, and bullish on iron ore and aluminum.

“Iron ore is expected to remain strong in the near term and could follow through in the bull case of a major China credit easing,” they said in a note.

China’s U-turn on covid policy and its pledge to increase support for the real estate sector helped to support ferrous and non-ferrous metals in December.

Still, optimism has been tempered by the country’s surging covid infections and risks of global recession in 2023 if central banks, as expected, keep hiking rates.

Nickel, the outperformer in metals, is on course for a 45% rise, its largest since 2010, partly because of a shortage of metal that can be delivered against the LME contract and partly because of volatility created by low volumes and liquidity after a trading fiasco in March.

(By Naveen Thukral, Florence Tan, Emily Chow, Enrico Dela Cruz and Pratima Desai; Editing by Bradley Perrett and Barbara Lewis)

More News

Bomb attack damages Ecuador mining agency probing illegal gold

It’s the second blast in recent weeks affecting Arcom offices.

June 29, 2026 | 12:28 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments