Cobaltmania

One does not usually expect a sober conference of traders and other players in the battery metals space to go all apocalyptic but that is what happened when the topic of Cobalt arose at the recent Argus Metals Week in London.

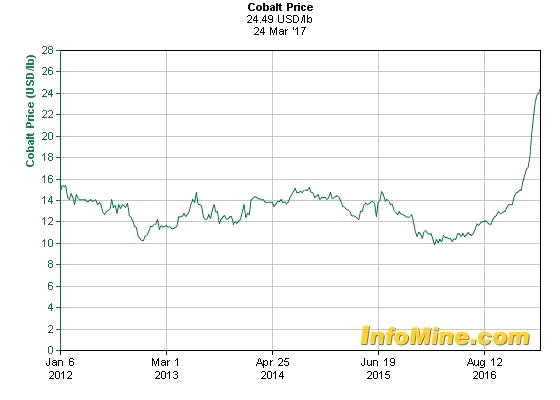

As is well known the price for Cobalt has been on a tear, dragging along prices of Cobalt “stories” in its wake. While much of the move has been attributed to the Lithium ion battery dynamic we would note that long term underinvestment in the metal (particularly in development of primary mines) and the closure of Cu-Co mine capacity by Glencore during its late-2015 near-death experience also played a part.

Lift-Off

The pace of change in the battery space has moved up a gear with the Cobalt crisis moving into centre stage and focusing minds on supply issues in the battery space, particularly as regards the “blue” metal. The Cobalt producers have annual output of around 100,000 tonnes. The price of Cobalt has soared (though still not back to pre-2008 levels) and the chatter in markets has been of an imminent supply crunch in absolute terms that might precipitate rationing by price and possible switching to alternative technologies.

While opinions differed on just how steep the rise in prices might ultimately be we perceived an even bigger threat in that there might be an absolute shortage of Cobalt, transitory or longer, in which case end-users (and by that we mean beyond just the battery space) may not be able to secure Cobalt for “love nor money” as they say in the classics. One might compare it almost to like a situation of war-time shortage when “nylons” or suchlike might have totally disappeared. Clearly in a rationing scenario there will not be governments (except maybe the DRC) in a position to ration supply and thus the advantaged parties will be those for whom the cobalt is only a tiny part of a high cost product (pharmaceuticals and electronics) while the most negatively impacted will be bulk users like paints and glass.

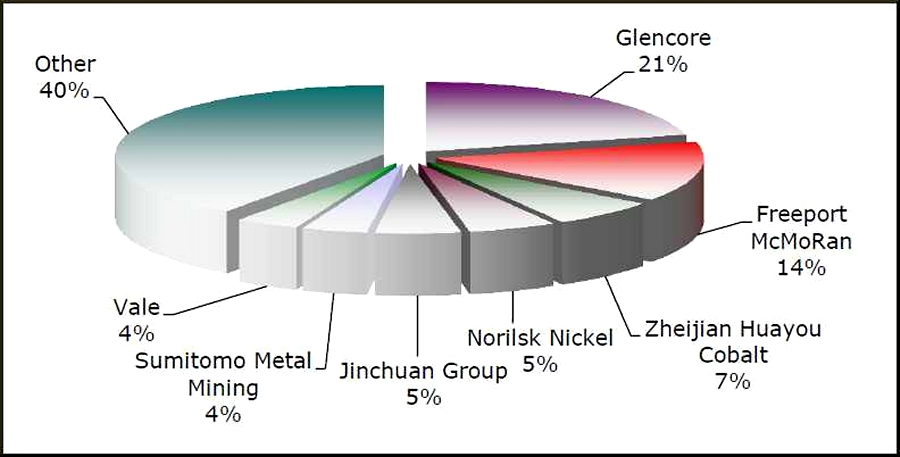

The problem is that while higher prices might produce elasticity in demand (depressing sales of some end products or prompting big price hikes or use of alternatives, where possible) the supply side is totally inelastic because of the lack of “turn-on-able” mines either in the primary or secondary category. Glencore is due, in 2018, to bring the Katanga mine in the DRC back on line after a US$430mn overhaul of its processing system. The operation has the potential to add as much 22,000 tonnes of cobalt. The chart below from Dorfman Anzaplan shows the current breakdown of global producers.

Beyond this there is no substantial pipeline. The long stalled primary mine project of eCobalt (formerly Formation Metals) in Idaho is one of the most advanced towards construction but even then we are talking several years at the least before a sellable product might appear. That company at least (after a long drought) has been able to raise quite a large amount of money in recent months to regain momentum towards production.

There are a handful of other projects in the works (though Dorfner Anzaplan claims that there are 46 active projects now, up from 10 at the same time last year). How many of these are credible is hard to gauge but we know some to be severely lacking in credibility both due to their very nature and also by the people involved with them.

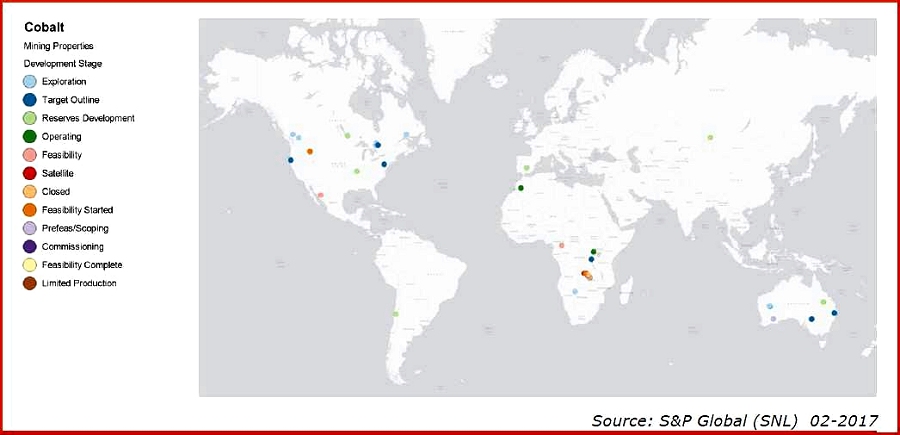

The map below from SNL Global shows the spread of these theoretical projects in the first half of 2017. Geographically the diversification looks good, at least.

So with a growing number of projects the picture for filling the production gap looks auspicious, but in fact it is not. Even if one third of these projects were “good”, most are still very formative indeed. If they went from 10 to 46 in number over 12 months then that signifies most have had little to no work done on them and we would also note that the real price liftoff was only in recent months so the bulk of these projects are of significantly less duration than six months.

That then in its own way confuses the market. It’s like a horse race where virtually none of the runners have seen a racetrack before. There is no “form”. That then means that punters do not know who to back and understandably place very small bets and spread them around. This does NOT make for a great financing environment. We have already seen in the Lithium space that few have put their money where their mouth is. Financings (except for a few choice or advanced names) have been little more than “maintenance” financings that pay to keep the lights on and fund the IR budget. Raises of sub-$500,000 do not pay for meaningful drill campaigns that lead to a resource. We are seeing the same thing happen in Cobalt as occurred in Lithium. That stretches out the timeline for the various staging posts on the way to production. Years to get a resource, then delays the PEA, then the DFS and BFS years later. Production then becomes little more than a twinkle in the eye. This solves no problem at all and will drive end-users insane with frustration at the dysfunctional equity markets in the mining space.

Stampede

The current rash of interest in the Cobalt space is all light and no heat. The situation now seems rather binary with the options being a slump when Glencore production feeds right through into the market OR one in which demand keeps rising, little new supply arrives and a crunch develops. Glencore now is interested in orderly markets and has benefitted massively by enforcing discipline (mainly upon itself) in 2015 that then resulted in the rallies in Zinc and Copper than have put it back on a strong footing. The delayed effect of the 2015 cuts has now washed into the Cobalt space with soaring prices. Glencore are not going to want to damage this new Goldilocks scenario that they have engineered. Even better for them the lack of any up-and-coming producers means that they can now effectively control the market and pricing by being the swing producer for at least another half decade. Primary mines are likely to be smallish and not make a dent in supply even should they get to production. Megamines, particularly in the NiCo space, like Ambatovy are seen as dinosaurs and not likely to spur a rash of lookalikes for a very long time indeed.

This augurs a situation in which end-users end up like frogs in the steadily hotter water that only realise that it’s boiling when they are well and truly cooked. We have had a mini-spike that has doubled the price to something like the levels that reigned pre-2008. There were speakers at the Argus event who mouthed the words “$65 per lb” and it did not rattle the teacups. Even at such a high historical level there is little that such a price could engender in new production, particularly if Glencore just sit back and decide to enjoy the situation, eking out supplies into the market.

Creative Commons image of swimmer from Eli Christman

Content adapted from Hallgarten & Company research report

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments