Column: European smelter hits mean another year of zinc shortfall

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

The global refined zinc market is expected to register a supply shortfall of 292,000 tonnes this year, according to the International Lead and Zinc Study Group (ILZSG).

It will be the second consecutive year of deficit after global production fell short of demand to the tune of 193,000 tonnes in 2021.

The Group’s latest twice-yearly analysis of the statistical landscape marks a major reassessment of zinc market dynamics. In October last year it forecast a cumulative surplus of 261,000 tonnes over 2021 and 2022.

Such are the perils of trying to capture a snapshot in time of zinc’s fast-moving fundamentals.

The big change in the intervening six months has been the powering-down of European smelters in the face of historically high power prices made worse by the war in Ukraine.

Europe accounts for around 15% of global zinc refining capacity, meaning it is now acting as a major drag on global run-rates.

[Click here for an interactive zinc price chart]

Such a significant smelter bottleneck is unusual in the zinc market, which has historically priced around mine production not refining cycles.

Refined production hit

Both mined zinc production and usage enjoyed a strong post-covid recovery last year, rising by 4.1% and 5.7% respectively, according to ILZSG.

Refined metal production, however, didn’t, global output rising by an anaemic 0.4% relative to 2020.

Power constraints in China were followed by much bigger problems in Europe, where energy costs were soaring even before Russia began its “special military operation” in Ukraine.

Glencore idled its Portovesme plant in Italy and both it and Nyrstar have been running other European smelters below capacity during peak power pricing periods.

Analysts at Citi estimate that 660,000 tonnes of annual smelter capacity is being restricted to some extent. (“Global Commodities”, April 29, 2022).

Hopes that power prices would fall with the advent of warmer weather have been dashed by the escalating energy stand-off between Europe and Russia.

ILZSG is forecasting another year of highly modest global refined production growth of just 0.9%, not enough to match anticipated demand growth of 1.6%.

With Europe’s smelters struggling and the Flin Flon smelter in Canada coming to the end of its life, global output will be driven by Chinese smelters this year.

China is expected to produce 2.5% more refined zinc this year after 1.0% growth in 2021, when many operators curtailed operations during a rolling power crunch.

That forecast comes with an important covid-19 caveat given China’s current round of lockdowns is causing all sorts of logistical problems for zinc smelters with national output actually falling by 1.0% year-on-year in the first four months of 2022.

Mine boom

World mine production of zinc is currently going through a boom phase with 2022 expected by ILZSG to be another year of robust 3.9% growth.

Most of that extra production will come from outside China, where mine production growth is expected to accelerate from last year’s 1.9% but only to 2.3%.

The shift to surplus in the zinc concentrates market was captured by this year’s benchmark smelter treatment charges, which rose to $230 per tonne from $159 per tonne in 2021.

Lower smelter production in Europe has added to that surplus and China’s smelters were charging as much as $300 per tonne to process concentrates into metal in late April, according to Fastmarkets.

Spot charges have since eased but only slightly and it looks like it’s going to be a good year to be in the zinc smelting business.

Or it is for those producers who don’t have to worry about record-high power prices.

Metal shortage

Such robust zinc mine production would in times past have shaped the market narrative, the assumption being that greater availability would lift smelter treatment terms and incentivise higher refined output.

Mine surplus should be a leading indicator of metal surplus subject to shipping and processing time.

However, it’s not if a significant part of the world’s smelter capacity can’t cover its power costs even with both higher processing charges and elevated physical premiums for metal.

Refined metal availability is currently determining pricing as much as underlying mine balance, both in terms of LME basis price and super-high physical premiums in Europe and the United States.

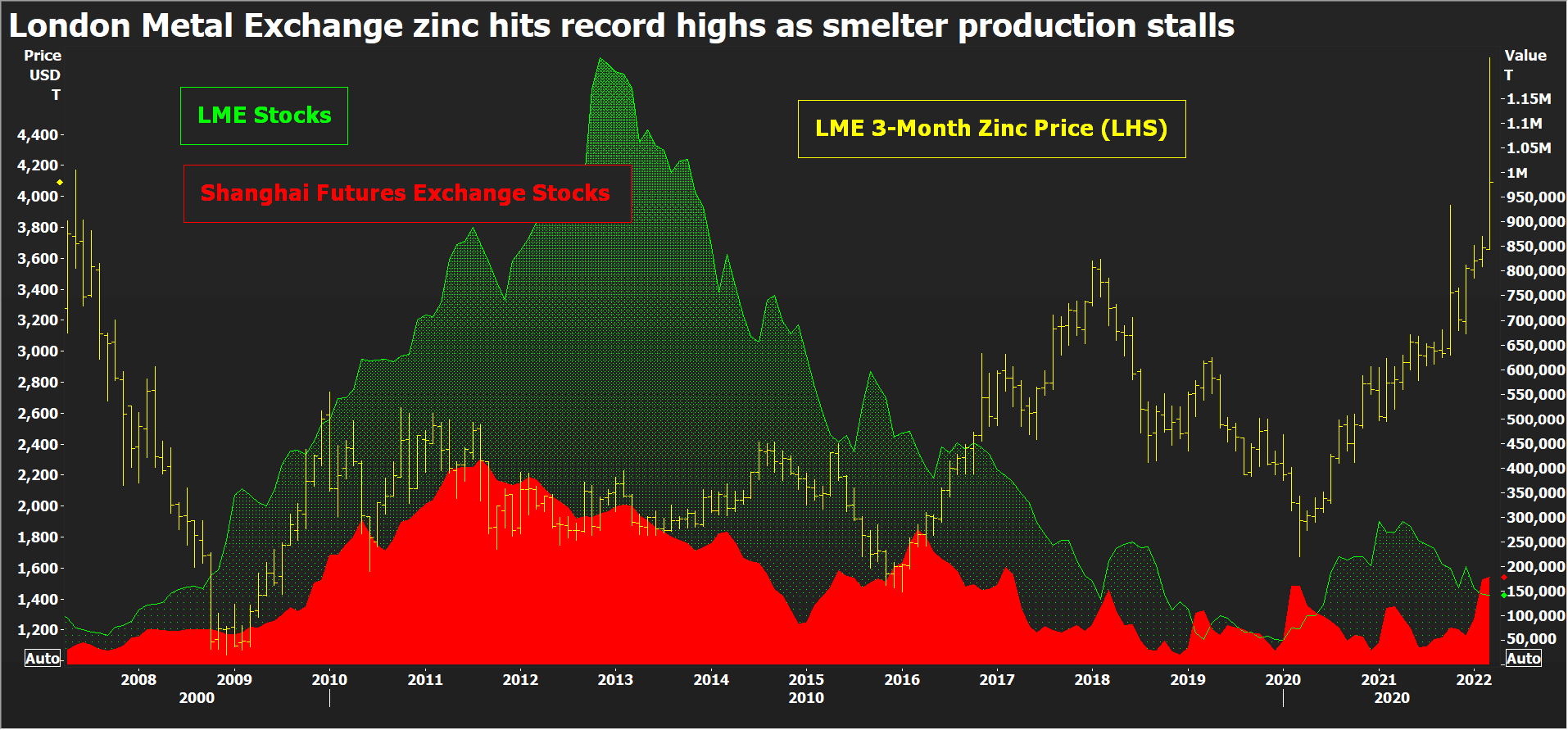

LME stocks, which were largely located in Asia, have been raided as metal is shipped to fill Europe’s depleted supply chain.

Headline inventory has slumped by 57% to 86,225 tonnes so far this year. Most of that is awaiting physical load-out with live on-warrant stocks standing at just 38,325 tonnes.

LME shadow off-warrant stocks have all but evaporated, totalling 3,171 tonnes at the end of March, down from 93,000 tonnes a year earlier.

There is plenty of zinc in China which could be exported to the rest of the world, but continued disruption in global logistics may slow the response time to a favourable export arbitrage opportunity.

A narrative kink?

At the start of the year lower European refined metal production looked to be a transient phenomenon, a kink in zinc’s normal mine-supply narrative.

Five months on and energy prices have only risen further, deferring expectations for a return to full smelting capacity.

The smelter twist in the zinc story isn’t going away any time soon, it seems.

Zinc has this month been caught up in the broader base metals rout with bulls fleeing the sector and bears flexing their muscles as the focus turns to China’s loss of growth momentum.

LME three-month metal at a current $3,575 per tonne is down by 27% from its March peak of $4,896 per tonne.

Even after that precipitous slide, however, zinc is trading just shy of 15-year highs. The fact that it’s doing so despite a full concentrates pipeline speaks to the scale of the smelting bottleneck currently defining the market.

(Editing by David Evans)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments