Iron ore price rally built on China hope, not fundamentals

(The opinions expressed here are those of the author, Clyde Russell, a columnist for Reuters.)

The spot price of iron ore for delivery to north China has surged almost 25% in the past three weeks, bouncing off a 19-month low as the market takes an optimistic view on Chinese steel demand next year.

The benchmark 62% grade , as assessed by commodity price reporting agency Argus, ended at $108.60 a tonne on Wednesday, up from $87 on Nov. 18, which was the lowest since May last year.

Iron ore is still well below the record $235.55 a tonne hit on May 12 this year, but the recent rally underscores that the market believes the worst is over for the steel-making ingredient.

China buys about 70% of seaborne iron ore and, as is customary, it’s China that is driving the current rally. But it’s worth questioning whether the jump higher in prices is based more on hope than reality.

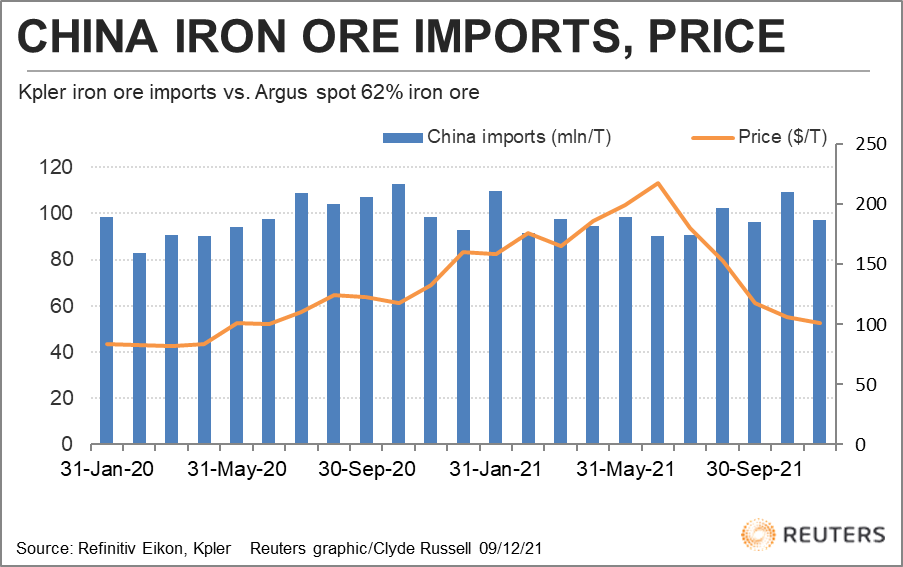

One of the factors kicking the price up was the release of customs data on Dec. 7 that reported November iron ore imports of 104.96 million tonnes, up 14.6% from October and the strongest month since July 2020.

On the surface, this does indeed look like a robust outcome and suggestive of a demand-led rally for iron ore.

However, there are some factors that make the November imports look somewhat less bullish.

The sharp jump may be a result of the timing of when China’s customs clears cargoes, and thus assesses them as having been officially imported.

The official data was well above the imports tracked by commodity consultants Kpler, which estimated November arrivals at 97.01 million tonnes, almost 8 million tonnes less than the official number.

However, Kpler pegged October arrivals at 109.14 million tonnes, which was 17.5 million higher than the customs figure of 91.61 million.

For September, Kpler had China’s imports at 96.46 million tonnes, compared with 97.49 million for the customs data.

Over the past three months, Kpler has estimated China’s iron ore imports at 302.6 million tonnes, while the official figure stands at 292.2 million.

This isn’t a massive gap, but the differences in when cargoes are assessed as having arrived can distort the true market picture.

Inventories gain

The other factor to consider on imports is whether they are rising because of demand from steel mills, or because traders anticipate higher demand next year, or whether traders are simply building inventories having taken advantage of the collapse in prices after May’s record high.

Certainly, there doesn’t seem to be increased demand from steel mills, some of which are still curtailing production to meet pollution and energy targets.

Port inventories in China have also been steadily gaining in recent weeks, hitting 154.4 million tonnes in the week ended Dec. 3, according to consultants SteelHome.

This is up from the 2021 low of 123.95 million in late June, and while inventories follow a seasonal pattern of building ahead of the northern winter and drawing down into the summer construction season, it’s worth noting that the current level is the highest for this time of year in data going back to 2012.

The market appears to be positioning for a rebound in steel demand in the first half of 2022, built on expectations that Beijing will once again open the stimulus taps to boost economic growth.

There is some evidence of this happening, with the authorities on Dec. 6 cutting the amount of cash that banks must hold in reserve for a second time this year, a move that releases 1.2 trillion yuan ($188 billion) in long-term liquidity.

Overall, it would appear that iron ore prices are rebounding on the expectation of future demand, and are happy to ignore the current signs that there is too much of the raw material arriving in China.

(Editing by Richard Pullin)

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments