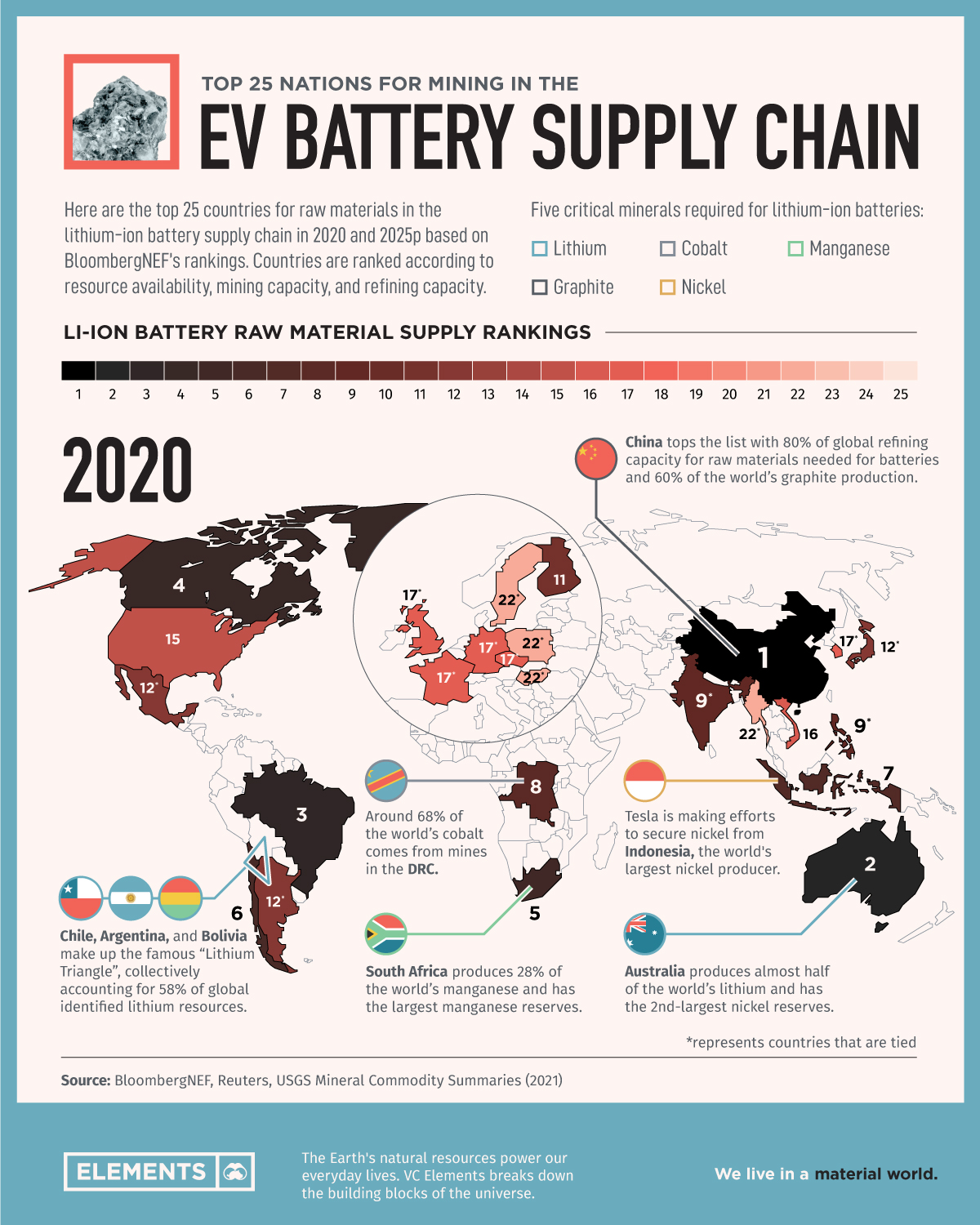

Ranked: Top 25 nations producing battery metals for the EV supply chain

The role of mining in the EV battery supply chain

Batteries are one of the most important and expensive components of electric vehicles (EVs). The vast majority of EVs use lithium-ion (Li-ion) batteries, which harness the properties of minerals and elements to power the vehicles. But batteries do not grow on trees—the raw materials for them, known as “battery metals”, have to be mined and refined.

The above graphic uses data from BloombergNEF to rank the top 25 countries producing the raw materials for Li-ion batteries.

Battery metals: The critical raw materials for EV batteries

The raw materials that batteries use can differ depending on their chemical compositions. However, there are five battery minerals that are considered critical for Li-ion batteries:

- Cobalt

- Graphite

- Lithium

- Manganese

- Nickel

Miners extract these minerals from economically viable deposits and refine them from their raw forms into high-quality products and chemicals for EV batteries.

The Top 25 nations supplying battery metals

Some countries are more crucial than others to the battery metal supply chain. BloombergNEF ranked the top 25 countries according to the following methodology:

- First, they tallied the mineral resources, mining capacity, and refining capacity in 2020 and projected commissioned capacity by 2025 for the five key metals listed above in each country.

- Then, to determine the overall score for each country, BloombergNEF categorized the countries’ capacities into five bands. Countries in the lowest band received a score of 1 and those in the highest band received a score of 5.

- The overall score is the result of averaging the scores across the five categories for each country.

Now that we have a better understanding of how the rankings work, here are the top 25 nations for raw materials in the Li-ion supply chain in 2020 and 2025.

China’s dominance in the rankings shows that refining capacity is just as important, if not more, as access to raw materials and mining capacity.

China does not boast an abundance of battery metal deposits but ranks first largely due to its control over 80% of global raw material refining capacity. Additionally, China is the world’s largest producer of graphite, the primary anode material for Li-ion batteries.

Australia comes in at number two due to its massive lithium production capacity and nickel reserves. Following Australia is Brazil, one of the world’s top 10 producers of graphite, nickel, manganese, and lithium.

On the other end of the spectrum, Poland, Hungary, Sweden, and Thailand are tied at rank 22. However, it’s important to note that these are among the top 10 countries for cell and component manufacturing—the next step in the lithium-ion battery supply chain.

Countries on the rise

Sweden’s rank rises five places between 2020 and 2025p, largely due to an expected increase in its mining capacity with nickel and graphite projects in the pipeline. Argentina is projected to jump up to eighth place thanks to its massive lithium resources and multiple mining projects in advanced stages.

Moreover, Japan is projected to move up four places with its first lithium hydroxide refining plant under construction. In addition, Japanese miner Sumitomo Metal Mining is planning to double battery metal production by 2028.

Although China will likely maintain its dominance for the foreseeable future, other countries are ramping up their mining and refining capacities. Given the increasing importance of EVs, it will be interesting to see how the battery metals supply chain evolves going forward.

More News

Norsk Hydro’s Slovak aluminium smelter to partially restart production

The pact paves the way for the restart of 75,000 metric tons per year of smelting capacity.

July 01, 2026 | 03:07 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments