Rio Tinto Group’s Australian and New Zealand aluminum smelters have been on the block, on and off, for the past six years or so. The business, dubbed Pacific Aluminium, has got a for-sale sticker on it again: Rio Tinto has hired UBS AG to explore a possible initial public offering on the Australian Securities Exchange after planned trade sales came up short, Reuters reported last week, citing two unidentified industry sources.

It’s not a bad time to be wheeling these assets out again. Aluminum forwards on the London Metal Exchange touched their highest levels in almost six years in December and premiums for prompt delivery of metal in Japan — one of the main end-markets for the Australian smelters — are up almost a quarter so far this year.

With China continuing to rein in capacity additions and President Donald Trump imposing a 10 percent tariff on imports to the U.S., the supply side of an industry that’s tended toward gluts looks tighter than it has in years.

Still, there’s a reason this business has remained on the shelf for so long. Aluminum smelting is an energy-intensive business that largely lives and dies on its electricity costs, making Australia’s chaotic, bitterly politicized energy policies a major investment risk.

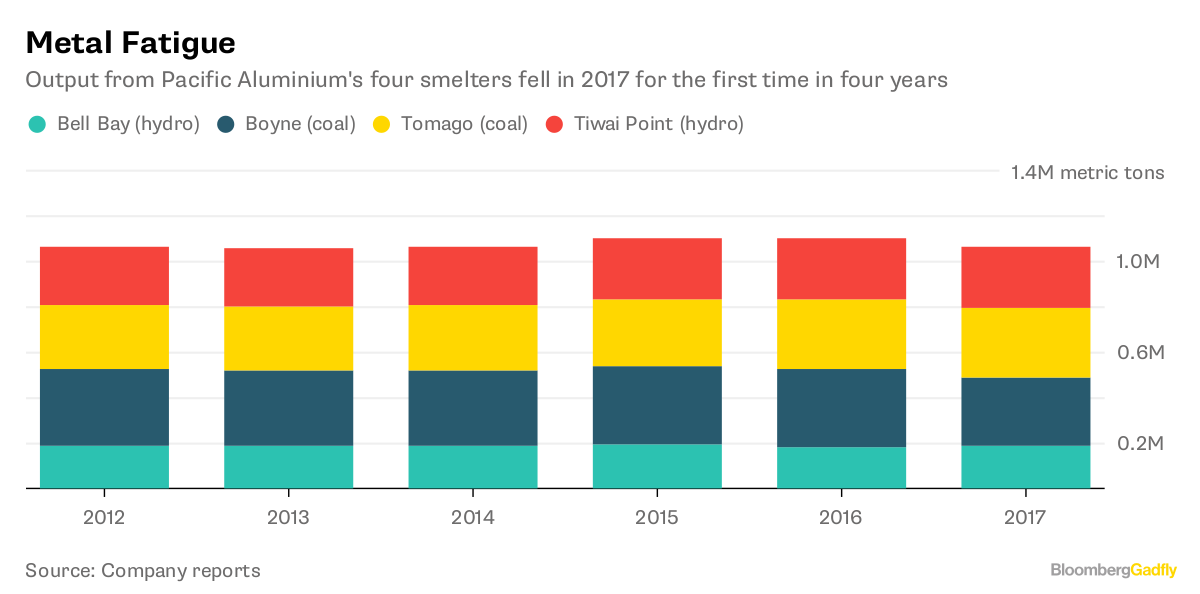

Almost 60 percent of Pacific Aluminium’s tonnage depends on the coal-fired Liddell and Gladstone power stations near Australia’s east coast, which are slated to close in 2022 and 2029 respectively. Its Boyne smelter cut output last year due to high prices for the roughly 15 percent of power it buys in the spot market, causing Pacific Aluminium’s production to slip for the first time since 2013.

Of the hydro-powered remainder, only the Bell Bay smelter in Tasmania seems secure for the long term, with an electricity contract running to 2025. Tiwai Point in New Zealand has an agreement with its generator Meridian Energy Ltd. allowing it to close at any time with 12 months’ notice — and Meridian certainly talks as if that could happen at any time.

Pricing such a deal is made more complicated by the uncertainty about the aluminum market and long-term energy prices, and also by the question of whether parts of Rio Tinto’s alumina business — which lost money for at least five years before finally turning a profit in 2017 — would be thrown into the mix as well.

Macquarie Group Ltd. analysts have put the tag anywhere between $2 billion and $3.9 billion, while the Reuters report quoted a price of $1 billion for the smelters and double that if the alumina refineries are thrown in. Such numbers are certainly plausible — at the median multiple of 7.9 for aluminum businesses in developed markets and three-year average Ebitda, the smelters and refineries could have an enterprise value as high as $4.1 billion.

That’s as much a problem as a benefit. The Australian equity markets have shown little appetite for new equity in recent years, with about $6 billion raised in initial public offerings last year and $6.5 billion the year before that.

To break that drought would require a truly compelling and unique proposition. Even at a time of robust commodity prices, Pacific Aluminium isn’t that.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

(Written by David Fickling)

Comments