Sudden jump in zinc stocks threatens bull party: Andy Home

(The opinions expressed here are those of the author, a columnist for Reuters.)

LONDON, March 5 (Reuters) – A bucket of cold water has just been poured on zinc’s bull fires.

The London zinc price has been on a two-year romp, hitting a 10-year high of $3,595.50 a tonne last month.

The bull run has been fuelled by a narrative of tightness, first at the raw materials stage of the supply chain and more recently in the refined metal segment of the market.

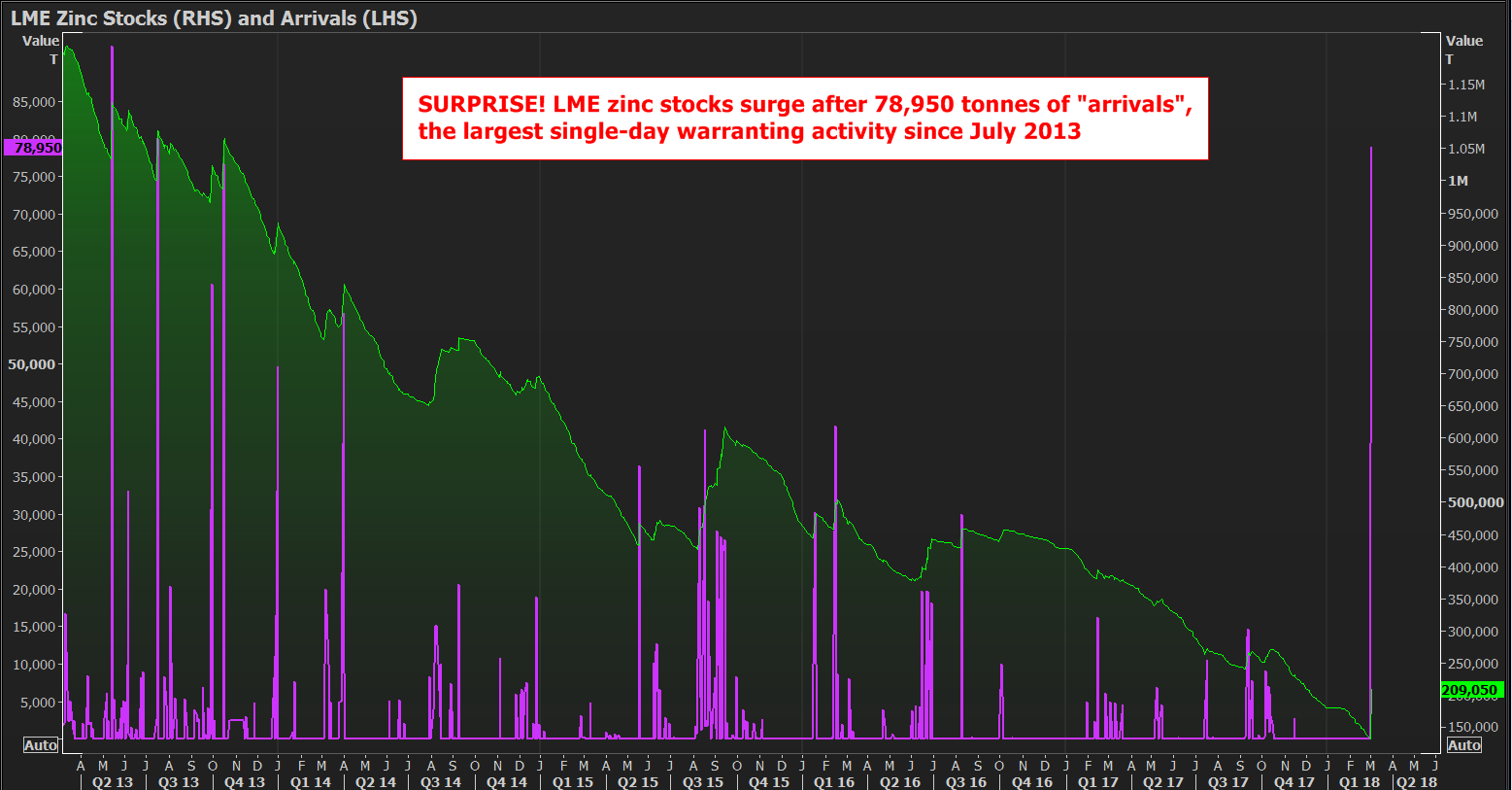

That narrative, however, has just been upended by the delivery of 78,950 tonnes of metal onto warrant at the London Metal Exchange (LME).

The “arrivals” showed up in today’s LME stocks report and break a long-running downtrend in LME stocks.

Headline inventory has bounced back to the levels of early December.

Someone, it seems, is calling time on the zinc party.

Graphic on LME zinc stocks and “arrivals”:

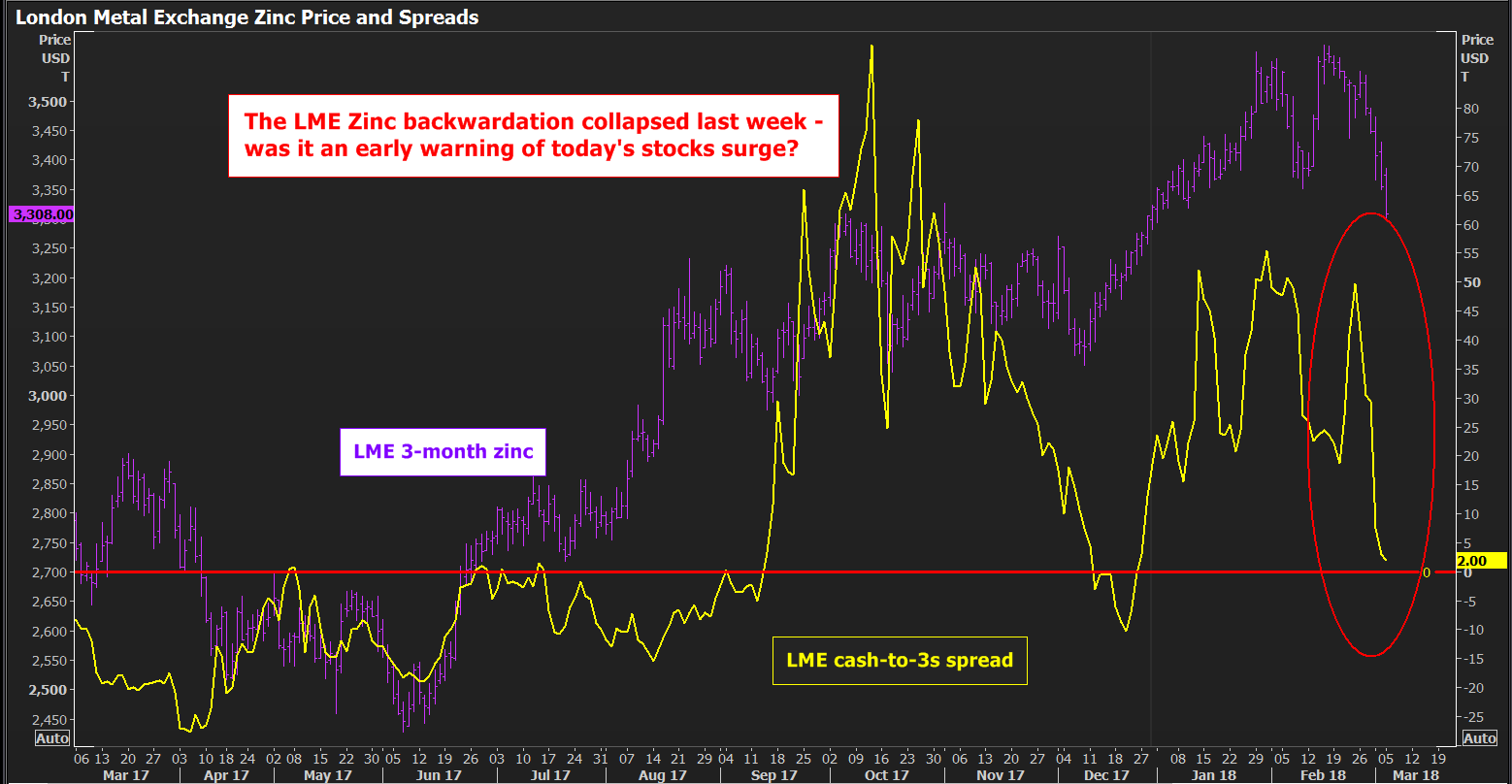

Graphic on LME zinc price and spreads:

Surprise!

Today’s was the largest single-day “arrivals” event in LME zinc stocks since July 2013.

It’s worth remembering that when this scale of tonnage shows up in the LME’s daily stocks reports, the metal hasn’t all just miraculously arrived and been warehoused overnight.

It has probably been accumulating for a while, biding its time until the owner hits a keyboard button to deliver it onto LME warrant, at which stage it “arrives” in the LME warehouse network.

The process still requires a fair amount of logistical coordination and the presumed intention was to spring a bear surprise on a bull market that has spent the past year watching LME inventory tick lower.

To judge by today’s sell-off — LME outright zinc sliding from an early high of $3,386 a tonne to $3,280 — the surprise worked.

There were, however, some clues that something like this was brewing.

The downtrend in LME stocks was starting to look just a bit too neat and managed. Since the middle of November, the traffic has been exclusively one-way, barring a modest 200-tonne inflow on Feb. 26.

The zinc market has a history of this sort of false stocks signal and the apparent relentless draw on LME inventory has been accompanied by growing market chatter as to what might be lurking in New Orleans.

This U.S. port has long been a statistical black hole for physical zinc, with extended periods of LME draws interspersed with sporadic heavy inflow as material oscillates between on-market and off-market storage.

That the city accounted for all of today’s mass warranting merely reinforces the message that nothing is ever quite as it appears when it comes to zinc in the Big Easy.

A second hint that something was pending was last week’s collapse in zinc time spreads.

The LME benchmark cash-to-three-months spread <CMZN0-3> collapsed from backwardation of $50 a tonne to one of only $3 at Friday’s close.

Such dramatic movements in LME spreads can often be an early warning sign of metal being readied for delivery into the LME system.

And so it has proved.

On the move

Today’s reported stocks surge should be a powerful reminder that LME stocks are only ever part of the bigger inventory picture.

There is always more “out there” beyond the exchange’s registered warehouse system. The only question is whether there is sufficient incentive to deliver it to the LME.

One of the curiosities of the recent LME zinc stocks trend was that so little was being delivered despite such a hefty cash premium of up to $90 a tonne last September.

But there again, for a metal in such supposed short supply, a lot of zinc has been on the move in the past couple of months.

China’s official trade figures show a cumulative 291,000 tonnes of refined zinc entering the country over the November 2017 to January 2018 period.

It was the largest three-month total since 2009, which was a year of massive upheaval in metallic trade flows in the wake of the global financial crisis.

The Chinese market shows signs of having trouble digesting the current flood of zinc.

Stocks of zinc registered with the Shanghai Futures Exchange (ShFE) dropped by 84,000 tonnes last year but have rebounded by 46,000 tonnes since the start of January to a current 114,887 tonnes. That’s the highest level since May 2017.

End of the bull party?

The question as to how long zinc could maintain its bull charge was always dependent on how much metal was sitting in the statistical off-market shadows.

The broad analysts’ consensus is that the acute tightness in the mined concentrates part of the zinc production chain is already starting to dissipate as a supply response to high prices builds momentum.

Glencore’s partial restart of mine capacity it mothballed towards the end of 2015 was both a signal that the cycle was starting to turn and served as an accelerator in that process.

But just as raw materials tightness took a year or so to translate into refined metal tightness, improving global mine performance will also take time to work its way down the supply chain.

While that plays out, any shortfall must be met by drawing stocks, both visible stocks registered in exchange warehouses and “invisible” stocks in non-exchange storage.

This is, of course, what appeared to be happening until the LME released its daily stocks bulletin at 0900 this morning.

What should worry zinc bulls now is that metal is showing up in significant quantities in both China and on the LME.

The combination is starting to look like an exit strategy by a player taking the view that we’re at, or very close to, the top of the price cycle.

That doesn’t mean they’re right, but they may have a better idea than the rest of us on how much more zinc might be “out there”. Particularly in New Orleans.

(Written by Andy Home; Editing by David Goodman)

More News

Genesis trumps Regis with $3.9B takeover bid for Vault

July 06, 2026 | 04:49 am

GoldStone surges 36% as Hong Kong miner takes 21% stake

July 06, 2026 | 04:06 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments