Will the copper price supply cut rally last?

Codelco’s El Salvador – to continue blasting for now

In New York trade on Friday copper for delivery in December consolidated recent gains jumping to a nearly 8-week high of $2.4645 per pound or around $5,430 a tonne for a 6.5% rise during the holiday shortened week.

The red metal has recovered strongly from six-year lows struck late August, but remains down 13% year to date after a 16% fall in 2014.

The latest rally was inspired by the announcement of steep production cuts by Glencore (LON:GLEN), the world’s number four producer of the metal.

Glencore’s move followed news that US-based Freeport-McMoRan (NYSE:FCX) which vies with Codelco as the world number one copper miner in terms of output, is cutting in half output at is El Abra mine in Chile and idling two US mines. Freeport also predicted lower output at its giant Grasberg mine in Indonesia.

For its part Chile’s state-owned Codelco has vowed to “cut costs to the bone” and delayed several expansion projects including going underground at Chuquicamata and pushing back expansion of the Andina complex by two years.

A new study by Capital Economics asks whether these cuts will be enough to change fundamentals in the industry and sustain the upward momentum in the copper price.

The short answer is yes. That’s mainly because the London-based independent research house believes mine supply will only grow by an anaemic 1.7% this year before contracting next year. That’s very much at the low end of forecasts.

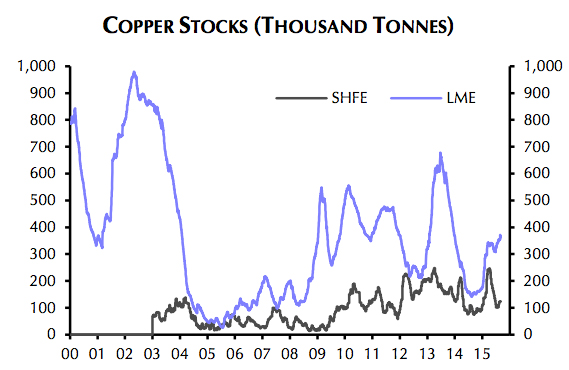

“Lower copper mine and refined output can only exacerbate what is already a relatively tight market, at least compared to some other metals. While copper stocks have been rising for much of this year, they remain low in a historical context,” says the author of the report Caroline Bain.

Inventories at LME Warehouses still only account for just over 2 weeks of annual usage according to Capital Economics’ 2015 demand estimates and coincides with a sharp slowdown in refined copper production growth from 6% to 3% during the first five months of the year.

Source: Capital Economics

Given the fact that many of the proposed closures are at SX-EW operations, supply growth in the refined market could be dampened further.

On the demand side that should close the gap between concentrate and refined imports from China, which consumes more than 45% of the world’s copper supply.

Chinese customs data for August showed while imports of refined and semi-finished copper products were flat imports of concentrate surged nearly 20% from a year ago and 18.6% from July. Year to date concentrate imports are up 12% to 8.12 million tonnes, while refined copper imports are down 8%.

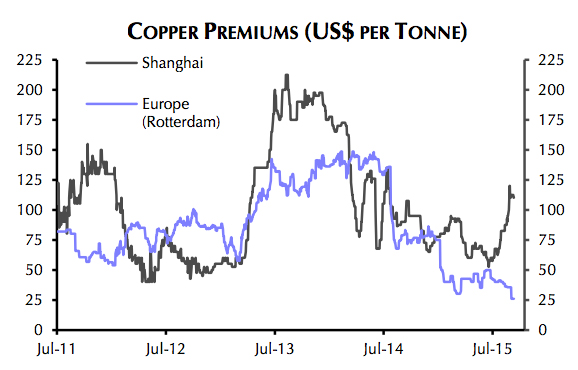

Market conditions in China is already tightening as evidenced by the recent surge in copper premiums for physical delivery inside the country.

Capital Economics is sticking to its end-2015 forecast for copper of $6,250 per tonne ($2.80 a pound) although it admits it “looks a bit of a stretch”.

But if the estimate does not pan out, suppliers won’t be to blame: “The main risk to this forecast is that demand fails to pick up in the final quarter of this year,” says Bain.

Source: Capital Economics

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments