World’s largest mining project takes $1 billion hit

In May 2014, the Guinea government and Rio Tinto (LON:RIO) and its partners – China’s Chalco together with the World Bank – inked a $20 billion deal for the southern section of the Simandou iron deposit in Guinea.

The agreement calls for a new 650km railway across the West African country to Conakry, Guinea’s capital in the north, plus a new deep water port at a conservatively estimated cost of $7 billion; infrastructure investments that will transform the economy of the impoverished country.

Rio, the world’s second largest mining company, posted a net loss of $866 million on Thursday and abandoned its promise to maintain its dividend. CEO Sam Walsh also promised the firm will reduce capital expenditure to $4 billion this year and $5 billion in 2017, which is $3 billion below previously announced targets.

The swing into the red was primarily due to a $1.1 billion writedown in the value of its investment in Simandou, but Reuters reports that does not necessarily mean the project is being pushed out further into the future. Neither should it “impede the hunt for funding” according to the company and its investors and advisors:

“This is just an accounting adjustment,” said Rio Tinto’s Alan Davies, president of the Simandou project. “Today’s decision has no impact on the timing of the project.”

The Guinean government also put out a statement in support of the project saying it’s “an essential opportunity for investors” and that it’s “fully confident in the success of the project”.

A feasibility study was due to be completed by July last year, but the ebola outbreak halted work at the site for months with hundreds of contract workers pulling out of the country

Simandou with over two billion tonnes of reserves and some of the highest grades in the industry (66% – 68% Fe which attracts premium pricing) has a back-of-the-envelope calculation value of more than $80 billion at today’s prices. It’s also one of the most easily exploitable iron ore fields outside of Australia’s Pilbara region and top producer Vale’s Brazilian home base.

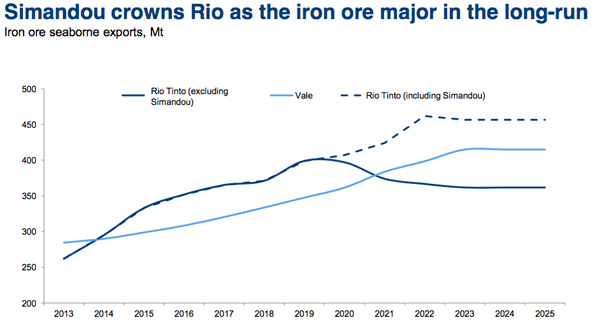

At full production Rio’s Simandou concession would export up to 100 million tonnes per year – that’s a third of Rio’s total capacity at the moment – and would catapult Rio past Vale as world number one. Simandou would by itself be the world’s fifth-largest producer behind Australia’s Fortescue Metals and BHP Billiton.

A producing Simandou mine would add nearly $6 billion to the country’s GDP which means the project has the potential to nearly double the size of the impoverished country’s economy in nominal terms. Guinea relies on exports of bauxite ore for the manufacture of aluminum for 80% of its export earning today.

Rio acquired the rights for the vast mountain deposit more than 15 years ago and has already spent more than $3 billion on the project. A feasibility study was due to be completed by July last year, but the ebola outbreak halted work at the site for months with hundreds of contract workers pulling out of the country.

At the end of 2015 Rio submitted an initial feasibility study on the mine and associated infrastructure to be built by Chinese construction firms and hopes to provide a comprehensive study in May this year “after downsizing the investment and enhancing the project economics.”

But with the price of the steelmaking raw material languishing not far off decade lows just above $40 a tonne and global mining companies in belt-tightening and cost cutting mode even flagship projects like Simandou are being placed on the backburner.

The country’s frustration with the lack of progress boiled over in October last year. Bloomberg quoted Cece Noramou, the government official overseeing the infrastructure project as saying Rio is “giving us the runaround. We’re running out of patience. We can’t spend our whole lives without any development”:

President Alpha Conde’s government is considering what mining policy to pursue, he told reporters Aug. 27 in the capital, Conakry. “There have been people at Simandou for 15 years, 20 years, and they’ve never produced a tonne of iron,” he said. Conde’s taking a new tender for another part of the deposit slowly because “we don’t want our minerals to be put out to pasture anymore,” he said.

There is little incentive for Rio to speed up development of Simandou with the global iron ore market in oversupply, Chinese demand moderating and its mines in Australia producing at full tilt (and enjoying the fattest margins in the industry).

“There have been people at Simandou for 15 years, 20 years, and they’ve never produced a tonne of iron”

And whether Guinea really has leverage to make the Anglo-Australian giant shift focus from existing operations is an open question. Even at the current development clip, it’s highly unlikely Simandou will ship ore this decade.

Glencore was said to be eyeing the Simandou North deposit, but in the 18 months since high-level representatives of Glencore travelled to Conakry to meet with government officials, the financial situation of the Swiss commodities trader and miner has been turned on its head. Anglo American at the time also said it has no plans to take on a project of this size.

President Conde inspects plans for the new port in July 2014

Simandou’s chequered history

Rio Tinto held the licence for the entire deposit since the early 1990s, but was stripped of the northern blocks in 2008 by a former dictator of the country.

BSG Resources, a company associated with Israeli diamond billionaire Beny Steinmetz acquired the concession later that year after spending $160 million exploring the property.

Rio filed a lawsuit for billions of dollars against both Vale and BSGR for what it called a “steal” of its concession

In 2010 BSGR sold 51% to Vale (NYSE:VALE) for $2.5 billion. The Rio de Janeiro-based company stopped paying after the first $500 million after missing a number of development milestones. Then the new Guinean government under Conde launched a review of all mining contracts awarded under previous regimes and launched an investigation into the Vale-BSGR joint venture.

The Guinea government withdrew the mining permit in April, accusing BSGR of obtaining its rights through corruption. BSGR has denied wrongdoing and filed an arbitration request in an attempt to win compensation from the Western African nation.

Shortly after BSGR’s rights were stripped Rio filed a lawsuit for billions of dollars against both Vale and BSGR in New York courts for what it called a “steal” of its previously-owned concession. Rio alleged BSGR paid a $200 million bribe to Guinea’s former minister using funds from Vale’s initial payment.

The US district court threw out the case in November saying Rio “had waited too long to file the lawsuit” under the Racketeer Influence and Corrupt Organizations Act, which calls for a four year time limit.

Photos courtesy of Rio Tinto Simandou. Graph source by CRU.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

2 Comments

Consulate of Guinea

You are interested in Guinea mining sector contact us: info@consulateofguinea.com http://www.consulateofguinea.com

Altaf

There is a lot of scope to develop mining, manufacturing in Guinea. But if each project is taken individually, they do not have the advantage. For example, currently iron ore prices are low. Therefore govt and miners should look for possibilities of refining ore to pig iron before exporting. It is a win win for every one involved. If Guinea invites Chinese investment in pig iron making, it is good for China. As China is moving up the value ladder, they might prefer importing pig iron to iron ore (reduction of need to have coking plants, blast furnace). It is good for environment as a third of shipping logistic is taken off (2 toms of iro makes 2 tons of pig iron) The savings in shipping can save the day for suppliers. Pig iron plants generate employment for Guineans.

If you consider bauxite exports, they can make aluminum using low cost hydro power which has great potential locally. Once again creating employment for the country, export value added products, good for developing nations as they are more concerned about their carbon foot print.