Zinc 2020 price forecast revised down over supply deficit – report

In its latest market outlook report, analysts at Fitch Solutions have revised down their 2020 zinc price forecast from $2,450/tonne to $2,250/tonne as an “amalgam of market forces,” put in motion by the Covid-19 outbreak, weighs on prices in the short term.

Since prices peaked in January at $2,454/tonne following the signing of the Phase one trade deal between the US and China, zinc prices have cratered below the $2,000/tonne mark on the London Metal Exchange.

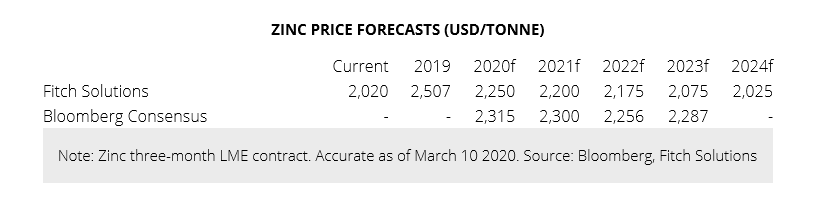

Fitch analysts expect prices to average lower in 2020 closer to $2,250/tonne compared to the 2019 average of $2,507/tonne

Over the recent weeks, zinc prices were pressured lower as the ongoing coronavirus outbreak led to numerous factory shutdowns in China and quarantines across the globe. With demand constrained, zinc inventories have increased significantly, resulting in lowered optimism from market participants, as evidenced by the decreasing net speculative position amongst traders on the LME.

As such, Fitch expects prices to remain subdued in the coming weeks as nations worldwide continue to grapple with how to best contain the spread of the virus while minimizing the impact on their domestic economies.

Zinc producers have already begun taking precautionary steps in face of the global spread of the novel virus. Earlier, Canada’s Lundin Mining put a temporarily halt on expansion activities at its Neves-Corvo zinc operations in Portugal.

However, Fitch analysts foresee the zinc market to improve later this year, under the assumption that the economic activity in China ramps up fully in the second half.

The Chinese government had extended Lunar New Year factory shutdowns in efforts to contain the spread of Covid-19, as well as locking down some of the largest and most economically significant cities where steel smelters are located such as Tangshan, the largest steelmaking hub in China.

Currently, it is reported that the number of new coronavirus cases has been tapering off in China, leading to a relaxation of city-level lockdowns, and workers are starting to return to work, which should bode well for economic activity.

As factories resume operations and construction activities pick up, Fitch believes this will lead to increasing demand for raw materials such as steel, and thus filter into higher demand for zinc over the coming quarters. Development should gradually lead traders back to their more bullish position, providing some additional support to prices as well.

Nevertheless, Fitch analysts expect prices to average lower in 2020 closer to $2,250/tonne, compared to the 2019 average of $2,507/tonne.

Prior to the Covid-19 outbreak, zinc treatment charges had remained elevated throughout 2019 and into 2020 as an increase in available zinc concentrate has allowed smelters to charge higher rates. While Chinese smelters had ramped up operating rates to capitalize on the profit opportunity, with the average rate across all producers in China reaching 87.9% in January, Fitch believes the virus outbreak has since caused a reduction in those rates due to the lockdowns. Consequently, treatment charges have reached highs of $300/tonne, a level not seen since 2008.

Assuming Chinese zinc smelters will ramp up operating rates over the year once again to capitalize on the higher treatment charges, Fitch expects this will lead to increased primary zinc output in 2020 and allow the supply deficit to loosen. Over 2020, it is estimated that global primary zinc production will grow by 2.8% y-o-y compared to 2.4% y-o-y in 2019.

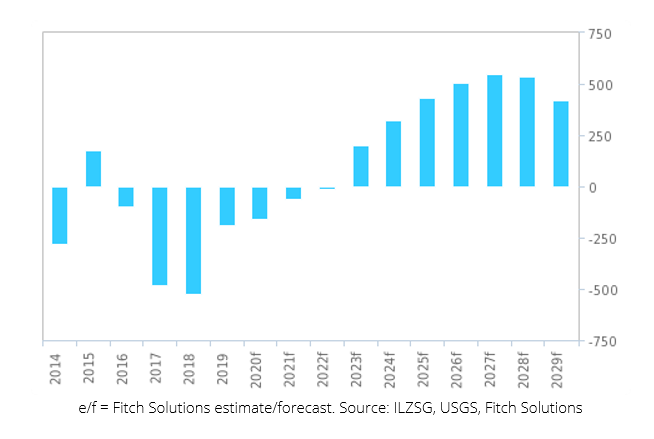

Global refined zinc production balance (‘000 tonnes)

In the long term, Fitch forecasts prices to remain on a gradual downtrend as the production balance shifts to surplus due to waning zinc demand, underpinned by sluggish growth in global steel production.

Read the full report here

More News

Column: Battery metals recovery runs into stop-start EV market

Prices of lithium, cobalt and nickel have all recovered from their 2024-2025 lows.

July 05, 2026 | 10:09 am

Zimbabwe lab sees regional gold hunt accelerate as prices soar

July 03, 2026 | 11:49 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments