More iron ore price madness as China’s mom-and-pops pile in

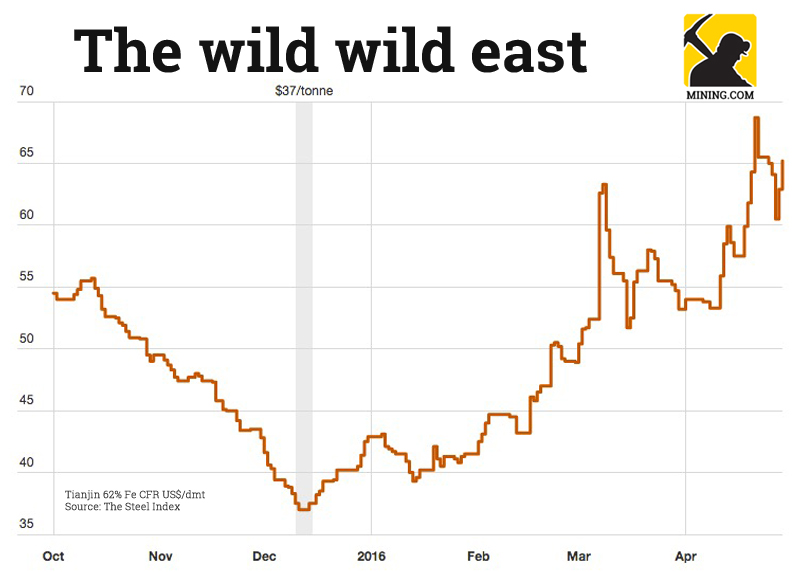

On Friday the Northern China benchmark iron ore price jumped to $65.20 per dry metric tonne (62% Fe CFR Tianjin port) bringing gains since Wednesday to 7.8% as commodity investment fever grips Chinese investors. Last week iron ore hit a 16-month high following an 11% jump over just two trading days according to data supplied by The Steel Index.

The steelmaking raw material has enjoyed a 52% rise in 2016 and a 76%-plus recovery from nine-year lows reached mid-December. On the Dalian Commodities Exchange the price swings are much wilder.

Despite a clampdown on rogue traders, higher margin requirements and trading fees, circuit breakers on Dalian iron ore futures to curb excessive price movement were triggered for the umpteenth time on Friday. That’s despite the exchange in northeast China “temporarily” upping the daily price change limit to 6%. The most traded contract ended Friday at its highs, exchanging hands for 462 yuan or $71.40 a tonne, duly up 5.97% on the day.

Some commentators pointed out that the financial churn on these contracts approached levels of trade seen on the S&P 500 in mid-April

The first signs that the fundamentals of the physical iron ore trade was no longer much of a factor driving prices came on March 7. The TSI benchmark price surged 19.5% in a single day – in absolute terms the day-on-day rise was roughly half of the price of contracted iron ore during the early 2000s under the old annual contract system.

While price movements are stomach-churning, the volumes traded are simply insane. After a very subdued launch scarcely two-and-half years ago, daily Dalian iron ore futures volumes surpassed one billion tonnes for the first time in March. That figure compares to the annual global seaborne trade of around 1.3 billion tonnes. Volumes are up 400% from a year ago.

In April the value of iron ore tonnes bought and sold was more than 2 trillion yaun or $329 billion (the exchange counts both sides of a trade so the Dalian numbers show double that). And that’s down from $477 billion in March.

A fascinating blog post by Ciaran Roe, global markets specialist for metals and mining at S&P Global Platts, points to another factor that makes iron ore and steel trading in China so different. Analysis by the Commonwealth Bank of Australia shows average time a futures contract is held on Dalian and the Shanghai Futures Exchange for rebar is “in and around the four hour mark.”

Risks to investors—both individual/retail and institutional—are clearly high, but so are the risks of misreading the data coming out of China

That compares to around 60 hours for the Comex copper contract or around 70 hours for Nymex natural gas in New York. Coupled with the low levels of open interest it’s clear that “speculative positions are the norm for ferrous contracts listed in China” says Roe:

Some commentators pointed out that the financial churn on these contracts approached levels of trade seen on the S&P 500 in mid-April.

Another defining feature of Chinese financial markets is the high percentage of retail investors. A whopping 80% of investors buy and sell stocks on the Shanghai and Shenzhen stock markets using their own accounts. On US markets that figure is less than 14%. Many of these mom-and-pop investors who had fingers burned shifted their attention from the country’s equity markets to commodity derivatives.

While the plunge on the Shanghai and Shenzen stock exchange had limited effect elsewhere in the world, six out of the world’s ten most active commodity contracts are now traded in Shanghai, Dalian and Zhengzhou.

Roe concludes that the full effects of the feverish retail derivatives trading in China has not been felt on physical markets, not yet anyway:

The exchanges, and by proxy the Chinese government, is aware of the dangers of having hugely volatile futures markets, which some claim have been on occasion more or less disconnected from underlying physical fundamentals.

Risks to investors—both individual/retail and institutional—are clearly high, but so are the risks of misreading the data coming out of China on such a strategic local industry as steel.

Who is to say that some of the surge in China’s steel prices—which prompted a global price recovery in the last two months—is not linked in part to sentiment of individual investors in China?

More News

Column: Battery metals recovery runs into stop-start EV market

Prices of lithium, cobalt and nickel have all recovered from their 2024-2025 lows.

July 05, 2026 | 10:09 am

Zimbabwe lab sees regional gold hunt accelerate as prices soar

July 03, 2026 | 11:49 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Altaf

This seems to be a logical reason why iron ore is going up despite slow down in demand in China. The ultra short term nature of commodity derivatives play by a large number of retail investors is a dangerous development for the iron ore market in general.

Just imagine, some mid scale miner in Australia restarts his mine by borrowing money hoping to cash in on 60+ price. And suddenly the retail investors dump iron ore derivatives market and move to some other lucrative investment opportunity. When iron ore prices crash to below 40, they take down with them the miners. On the other hand, fearing such eventuality, if the mid scale miner sits tight, only the big players will enjoy the high prices.

Looks like the time is right only for big players who have deep pockets. Small players can not have long term plans.