Hudbay Minerals to buy Arizona Sonoran in $1B deal

Hudbay Minerals (TSX, NYSE: HBM) said on Monday it will acquire Arizona Sonoran Copper Company (TSX: ASCU) (OTCQX: ASCUF) in an all-share deal valued at about C$1.48 billion ($1 billion), creating what the companies say will be the third-largest copper district in North America.

The Canadian miner will issue 0.242 of a common share for each Arizona Sonoran (ASCU) share it does not already own, valuing it at C$9.35 per share based on Hudbay’s Feb. 27, 2026 closing price. The offer represents a 30% premium to ASCU’s closing price that day and a 36% premium to its 20-day volume-weighted average price. Hudbay, which already owns about 9.99% of ASCU’s outstanding shares, said the enterprise value of the transaction, net of its existing stake, is approximately $1.28 billion.

The acquisition will give Hudbay full ownership of the Cactus copper project in Arizona and expand its US growth pipeline alongside its Copper World project. After closing, existing Hudbay shareholders will own about 89% of the combined company, with former ASCU shareholders holding roughly 11%.

Chief executive Peter Kukielski said the deal strengthens Hudbay’s position as a US-focused copper growth platform. He described Cactus as a large-scale development asset in a familiar mining jurisdiction and said the combined projects would form a major copper hub in Arizona while preserving financial flexibility.

Arizona Sonoran chief executive George Ogilvie said the transaction delivers immediate value and allows shareholders to retain exposure to Cactus through Hudbay shares. He added that Hudbay’s balance sheet and Arizona operating experience should reduce development and financing risk.

Strategic rationale

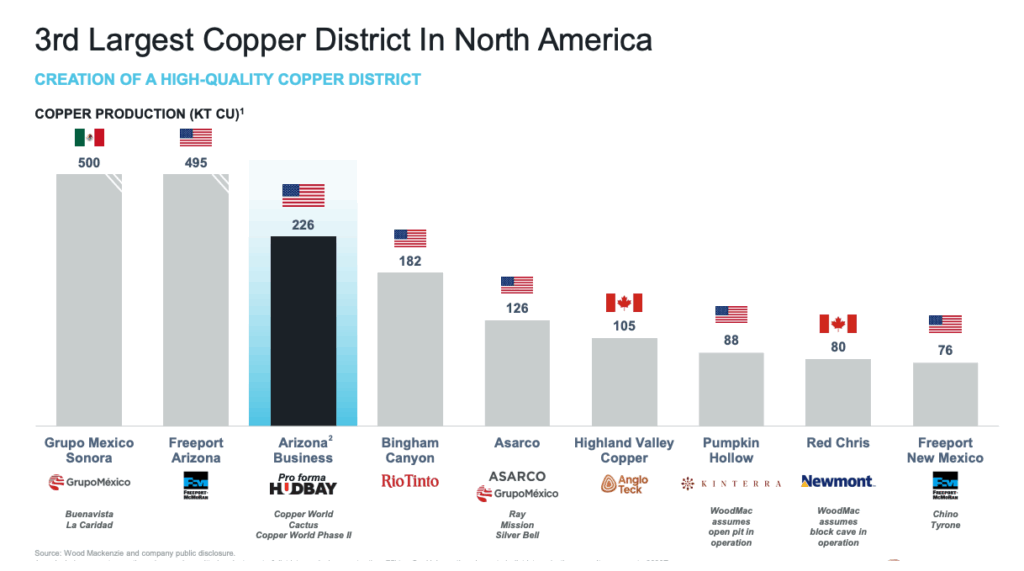

Hudbay said advancing Copper World and Cactus together could also create the second-largest US copper cathode district. Copper World is expected to produce 92,000 tonnes of copper annually by 2030, while Cactus could add a further 103,000 tonnes a year once developed.

Jefferies analysts said the transaction would significantly increase Hudbay’s copper weighting. On a pro forma basis, they estimate the company’s 2030 production mix would shift from about 55% copper, 38% gold and 7% other metals to roughly 87% copper, 10% gold and 3% other. They added that about 80% of the combined asset base would be concentrated in Canada and the US, increasing the company’s North American exposure.

BMO Capital Markets said the deal creates a major US copper producer with cost savings and adds another development project that fits naturally into Hudbay’s pipeline following Copper World.

“Both projects are relatively low risk and assuming the Cactus prefeasibility estimate of about $1 billion is appropriate, Hudbay is adding copper production at a reasonable circa $24,000 per tonne,” analyst Matthew Murphy said in a note Monday. “In conjunction with Copper World, the development of Cactus would lift Hudbay Arizona production to 226,000 tonnes a year, making it a significant U.S. copper business with construction and operational synergies.”

The company also outlined regional synergies, including redeploying the Copper World construction team to Cactus, using sulphuric acid produced at Copper World to leach oxide ore at Cactus, and achieving between $5 million and $10 million in annual corporate savings.

In a project comparison, Jefferies noted that Cactus hosts proven and probable reserves of 5.3 billion lb. of copper, or 465 million tonnes grading 0.52% copper, and is expected to produce 103,000 tonnes annually over a 20-year mine life at cash costs of $1.34 per lb. That compares with Copper World’s 4.6 billion lb. of copper in 385 million tonnes at 0.54% copper, with expected annual output of 93,000 tonnes over 20 years at cash costs of $1.53 per lb.

Advancing Copper World and Cactus together would create North America’s third-largest copper district, with the potential to become the second-largest US copper cathode producer.

The analysts added that Cactus sits on private land in Arizona and is fully permitted under a 2021 preliminary economic assessment, though amendments will be required for the 2025 prefeasibility study.

The companies will complete the transaction through a court-approved plan of arrangement under British Columbia law. The deal requires approval from 66⅔% of votes cast by ASCU shareholders, 66⅔% of votes cast by shareholders and other securityholders voting together, and a simple majority of minority shareholders under Canadian securities rules.

Limited bid risk

Jefferies said it views the risk of a competing bid as low to moderate. While it did not rule out the possibility of an interloper, the firm said the 30% premium, the all-share structure and Cactus’ development-stage profile raise the economic and execution bar for alternative buyers, limiting the likelihood of a superior proposal emerging.

Arizona Sonoran plans to hold a special meeting in May 2026. The transaction also requires US and Canadian regulatory approvals, court approval and stock exchange approvals. Both boards have unanimously approved the agreement and recommend shareholders vote in favour. The companies expect to close in the second quarter of 2026.

Shares in Hudbay Minerals fell 6.8% to C$36.03 apiece in Toronto on Monday morning, valuing the company at C$14.2 billion ($10.4 billion). The stock has traded in a 52-week range of C$8.49 to C$38.94.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments