Zimbabwe export ban a temporary dent on lithium supply, says Fitch’s BMI

While Zimbabwe’s ban on raw materials exports is expected to tighten the global lithium market, its impact would not be as prolonged or profound as the Congo cobalt curbs last year, says Fitch’s BMI unit.

In late February, Zimbabwe’s mining minister announced an immediate ban on exports of raw minerals, including lithium concentrates. The ban was previously expected to come into force in January 2027 to align with the commissioning of new processing facilities, which would allow producers to mine and process locally rather than overseas, in particular in China.

“By bringing forward the ban, which follows earlier restrictions on the export of lithium ores introduced in 2022, we expect lithium miners in Zimbabwe to be left with little choice but to curb production until sufficient processing capacity is available,” BMI said in a report released on Tuesday.

Lack of processing

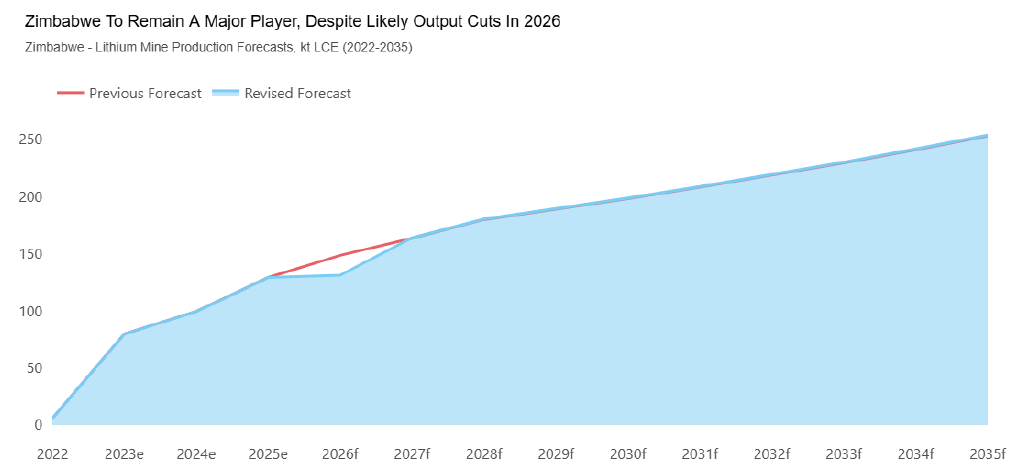

Given the African nation’s growing role in the lithium market, now accounting for about 10% of global production, its export ban would lead to a tightening supply until at least mid-to-late 2027, when local processing facilities ramp up, the firm noted.

Zimbabwe is expecting its first lithium processing facility in the coming months. However, the plant, being developed by China’s Huayou Cobalt, would only have the capacity to process lithium concentrates produced at the company’s own Arcadia mine. Therefore, other miners without access to processing are likely to opt to temporarily scale back production, BMI said.

As such, the firm has revised down its 2026 Zimbabwe mine production forecast to 131,100 tonnes in lithium carbonate equivalent. In 2027, it expects production growth to resume as additional processing capacity comes online, including lithium sulphate plants at Sinomine Resources’ Bikita mine and at the state-owned Kamativi mine.

Different to Congo

Zimbabwe’s ban on lithium follows similar restrictions on cobalt exports introduced by the Democratic Republic of the Congo in February 2025, which have since been modified into a quota.

According to BMI, the Zimbabwe ban would not have an acute impact on end-users like the Congo export curbs did, as its share of lithium production is not high enough to materially trigger demand destruction downstream.

“By contrast, the DRC produces around 75% of the world’s cobalt, meaning its export restrictions will significantly raise costs for end-users, most notably battery makers,” the Fitch unit said.

It also noted that Zimbabwe’s move is more likely to be successful in promoting local processing than DRC, which has seen little-to-no progress on that front and saw massive divestments following its cobalt restrictions.

Higher lithium prices

In response to the near-term supply concerns, BMI has raised its 2026 price forecasts for lithium. Chinese lithium carbonate and hydroxide monohydrate prices are now expected to average $13,500/tonne and $13,000/tonne, respectively, as the market moves to rebalance from a protracted period of oversupply.

As prices start to bottom out in early 2026, the firm noted that a further upward revision might be on the cards in the coming weeks.

“Supply-side swings are set to be central to the lithium market, as swift restarts of idled capacity during a price recovery could prompt production to ramp up quickly, although a protracted bout of disruptions may be sufficient to underpin a sustained upward trajectory,” it said.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments