Mining’s nuclear reality check: SMRs are still not on miners’ shopping lists

In theory, small modular reactors look almost purpose-built for mining. Remote mines need reliable power. Off-grid operations still rely heavily on diesel. Electrification of operations will increase loads. Downstream customers want cleaner, traceable supply chains. Nuclear offers firm, low-carbon electricity and heating without the intermittency of wind and solar and a much smaller footprint.

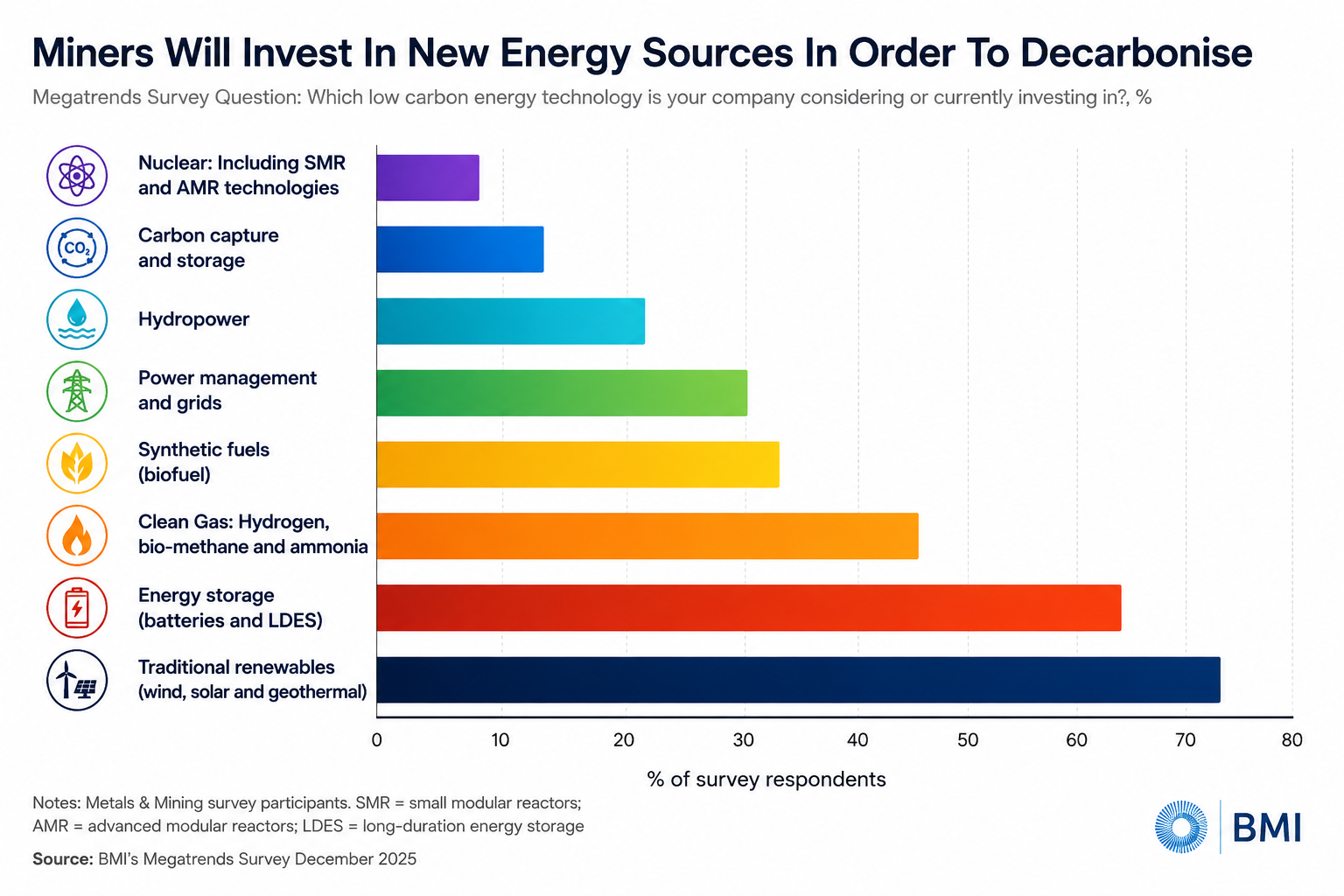

Yet BMI’s Metals And Mining Megatrends To 2050: Navigating A New Era Of Technology, Geopolitics And Green Transformation suggests mining companies are not rushing to nuclear. In its survey of low-carbon energy technologies under consideration or investment, nuclear — including SMR and AMR technologies — ranks last, below 10%.

That puts nuclear well behind traditional renewables (just over 70% of miners surveyed are considering or currently investing in wind, solar and geothermal), energy storage like battery or other long duration storage technologies (nearly 65%), clean gas, synthetic fuels (almost half), power management and grids, hydropower and carbon capture.

For a mine operator, a solar project, wind contract, battery system or grid upgrade sits inside a relatively familiar commercial framework while even a small reactor brings nuclear licensing, long approval timelines, site security, fuel supply, waste handling, emergency planning, community consultation and long-term liability. Traditional renewables may not solve every off-grid power problem, but they are modular, financeable and familiar. For a company under pressure from automakers, battery makers and technology customers to show near-term emissions cuts, waiting for SMRs is difficult to justify.

Moreover, many of the most advanced SMRs are 300 MW-class units, far larger than the needs of most standalone mines. Microreactors in the 1-20 MW range are closer to mine-site scale, but they are in the early stages of commercialization, although a trend towards factory-built units may accelerate the pace.

A 300 MW-class SMR would be oversized for most mines, especially smaller off-grid operations with limited processing loads and, perhaps more importantly, shorter mine lives. But it is not automatically too large for the biggest copper complexes. In northern Chile, large mines that combine high-throughput concentrators, desalination plants, high-altitude water pumping, conveyors, port infrastructure and future fleet electrification can require power in the hundreds of megawatts.

Teck’s Quebrada Blanca Phase 2 renewable contracts imply total operating power needs of a few hundred megawatts, while BHP’s Escondida and Spence renewable contracts total 6 TWh/year, equivalent to an average load of about 685 MW across the two operations.

Natural fit

The appeal is not hard to understand. Off-grid mines often pay high costs for diesel generation, fuel transport and backup power. In Canada’s backcountry, the outback of Australia and other remote regions, weather and logistics can turn fuel supply into a strategic risk.

That case has been made for years. The Canadian Nuclear Association has argued that small modular reactors could produce clean electricity for mining and other heavy industries, particularly at off-grid northern operations trying to cut diesel use. The same argument also points to nuclear heat for extraction industries and hydrogen production, with SMRs supporting renewables when wind or solar output falls.

Uranium producers have also been positioning around the SMR opportunity. As far back as 2021, Cameco signed agreements to evaluate uranium fuel supply chains for small modular reactors, including the GE Vernova Hitachi BWRX-300 and X-energy’s Xe-100, aiming to become a fuel supplier for the emerging SMR and advanced reactor market.

There are also more mine-scale concepts. Eagle Energy Metals has combined uranium exploration with reactor technology, saying its micro modular reactor could deliver up to 3.3 MW and be deployed at mine sites, military outposts and disaster relief areas. The company’s Aurora project anchors a broader strategy around domestic uranium resources and SMR technology.

Big tech’s hunger for power

Ontario has started construction on the first small modular reactor in the G7 at Darlington, where Ontario Power Generation is building the first of four planned 300 MW units, a major milestone for the SMR industry.

Ontario’s broader energy plan reinforces the same point. The province expects electricity demand to rise sharply by 2050 and has aligned its strategy with OPG’s C$20.9 billion commitment to small modular reactors. The plan could include 10,000 MW of additional nuclear capacity and transmission expansion to support industrial growth and mining districts such as the Ring of Fire. That means Ontario’s nuclear plan could boost uranium mining and eventually supply mining regions through the grid, but it does not mean miners are buying reactors themselves — not yet anyway.

Saskatchewan is moving in a similar direction. Cameco, SaskPower and Westinghouse are evaluating reactor technologies, including the AP1000 and AP300 SMR, for long-term electricity planning. SaskPower is expected to make a final investment decision in 2029 on whether to proceed with its first SMR facility, and the utility intends to use Saskatchewan-produced uranium if reactors are built in the province. The work around nuclear reactor technology for clean electricity is highly relevant to uranium miners, but again the customer is the power system.

In the US, the pattern is even clearer. Louisville Gas and Electric and Kentucky Utilities are exploring X-energy’s Xe-100 SMRs to meet growing demand from the grid and large-load customers, including data centres.

New York-based investment firm Goehring & Rozencwajg’s latest Natural Resource Market Commentary highlights a string of nuclear demand signals from the technology sector, including Google’s collaboration with Kairos Power and the Tennessee Valley Authority, a novel power purchase agreement under which Kairos Power’s Hermes 2 reactors would deliver up to 50 MW into the TVA grid for Google data centres in Tennessee and Alabama.

Google has also moved on conventional nuclear. Its agreement with NextEra Energy to restart the Duane Arnold Energy Center in Iowa under a 25-year power purchase contract shows that hyperscalers are not waiting for mine-site SMRs to prove the model. They are locking in firm nuclear power wherever they can get it.

Meta has gone even bigger. Agreements covering up to 6.6 GW of power with Vistra, TerraPower and Oklo would support Meta operations and its Prometheus AI supercluster in Ohio, while extending the life of existing reactors and accelerating new reactor technologies. The deals make Meta one of the most important corporate buyers in the nuclear market and show how Meta and Sprott are helping power the nuclear revival.

TerraPower is also moving from concept to construction. The Bill Gates-backed company has started work on its flagship Natrium plant in Kemmerer, Wyoming, a 345 MW sodium-cooled fast reactor with molten salt-based energy storage that can lift output to 500 MW when needed. The project follows a US Nuclear Regulatory Commission construction permit and is on track to become the first utility-scale advanced nuclear power plant in the US.

Uranium demand is accelerating

The World Nuclear Association expects uranium demand for reactors to climb 28% by 2030, reaching nearly 87,000 tonnes annually before more than doubling to over 150,000 tonnes by 2040. Existing mine supply may be enough in the short term, but output from current mines is expected to fall sharply after 2030, and new uranium projects can take 10 to 20 years to develop.

AI is adding a new layer to the demand story. Investor surveys and asset managers increasingly see data-centre electricity demand as a structural driver for nuclear generation and uranium procurement. That has shifted how uranium is viewed: less as a niche reactor fuel and more as a strategic energy-security commodity. The result is a market where AI-driven power demand could tighten uranium supply.

Japan is another demand signal. Goehring & Rozencwajg point to the restart momentum in Japan’s nuclear industry, including Tokyo Electric Power’s restart of Unit 6 at Kashiwazaki-Kariwa. Japan’s broader policy shift back toward nuclear (following the Fukushima disaster 15 years ago) has been building for several years, with uranium added to the country’s critical minerals list as part of an effort to reduce dependence on foreign sources. That move marked another sign of uranium’s return to strategic status.

Life extensions may be just as important as new builds. Meta’s agreements with Vistra improve the outlook for Perry, Davis-Besse and Beaver Valley, plants whose long-term futures had previously been uncertain. If more reactors that once looked at risk of closure receive long-term corporate power contracts, uranium demand rises without waiting for new nuclear construction to catch up.

The supply base is fragile

The bullish uranium story still has a weak point: mine supply.

Boss Energy’s Honeymoon mine in South Australia is a warning. The project restarted in 2024 and had been seen as evidence that Australia’s uranium industry was returning to growth. But Boss later withdrew its 2021 Enhanced Feasibility Study after the mine performed materially below earlier assumptions.

Instead of ramping toward roughly 2.4 million lb. per year, with a potential expansion to 3.3 million lb., the mine is now expected by the firm to produce closer to 1.5 million lb. annually, with a shorter mine life than originally anticipated.

The tonnage shortfall is not huge in global terms but points to the fact that uranium mine restarts and greenfield projects are technically difficult, capital intensive and vulnerable to geology, leachability, permitting, construction delays and cost inflation. If smaller restart projects struggle, the industry’s ability to respond quickly to a demand surge becomes more doubtful.

US reactor operators face possible uranium shortages over the next decade, with the Energy Information Administration warning that the supply gap could widen to a combined 184 million lb., equivalent to more than three years of consumption. More than 90% of the uranium consumed by US reactors was sourced internationally, highlighting the vulnerability of the US nuclear fuel supply chain.

Enrichment is another constraint. Urenco USA, the only commercial-scale nuclear fuel producer in the US, plans to lift enriched uranium capacity by almost 50% through a multibillion-dollar expansion in New Mexico, but the first new centrifuge sets are not expected until 2032. The expansion is meant to reduce exposure to Russian uranium and fuel services, but it also shows that nuclear fuel supply chains cannot be rebuilt overnight.

Advanced reactors add another fuel challenge. Many designs need HALEU, high-assay low-enriched uranium, which is not yet available at commercial scale outside Russia. The US has awarded contracts to boost domestic HALEU production, with up to $2.7 billion available, because higher-enriched uranium is expected to be needed for a wave of advanced reactors.

Europe is also trying to diversify. Pressure is mounting for the EU to phase out Russian uranium and nuclear fuel services, a shift that could strengthen Canadian suppliers such as Cameco. Canada supplied more than 30% of the EU’s uranium imports in 2024, but replacing Russian enrichment services could take years. The push to move away from Rosatom has already become a potential tailwind for Canadian uranium exports.

Speed a selling point

Energy Fuels expects to meet its 2026 uranium production guidance by midyear, with U3O8 production forecast to reach 1.6 million lb. by the end of June. The company is positioning itself as a leading US uranium producer, helped by the White Mesa Mill in Utah, currently the only fully licensed and operating conventional uranium mill in the US.

Cameco is consolidating high-grade supply in Saskatchewan. The company is paying C$115.75 million to lift its stake in Cigar Lake, described as the world’s highest-grade uranium mine. The transaction increases Cameco’s ownership to 57.418%, while Orano’s stake rises to 42.582%.

New Canadian supply is also advancing. NexGen Energy plans to begin construction at Rook I in northern Saskatchewan, a C$2.2 billion project with the largest development-stage uranium deposit in Canada. The Arrow deposit hosts probable reserves of 240 million lb. U3O8, making Rook I one of the most important new uranium projects in North America.

Denison Mines is building Phoenix, Canada’s first in-situ recovery uranium mine, with first production targeted for mid-2028. The ISR method can reduce surface disturbance, costs and construction timelines compared with conventional mining, positioning Denison among the few suppliers able to provide meaningful new uranium supply before the end of the decade.

Private developers are trying to move faster too. Triton Uranium has begun development activities at its Atlas project in Uranium City, Saskatchewan, arguing that AI data centres and renewed US nuclear buildout are accelerating demand before most uranium projects can respond. Its strategy reflects the broader market pressure: speed has become a selling point in North American uranium supply.

Goehring & Rozencwajg argue that investor demand for physical uranium continues to build, with the Sprott Physical Uranium Trust building holdings to more than 81 million lb. The price story is more mixed: spot uranium surged above $100/lb in January, but has since cooled to the mid-$80s, still up more than 12.4% year-on-year

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments