Op-Ed: Brazil’s rare earth dilemma — strategic autonomy or another raw-material export cycle?

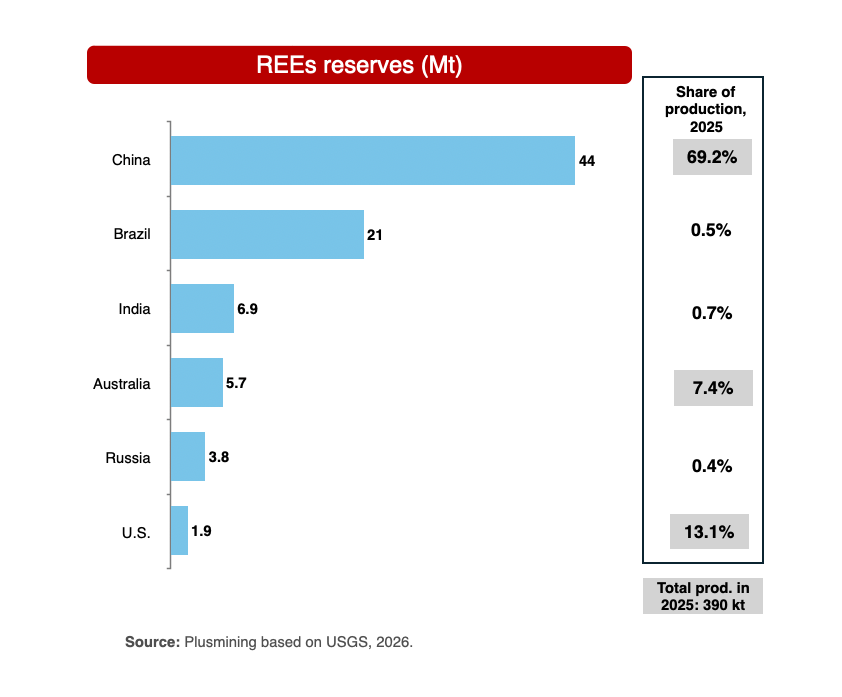

Brazil has one of the world’s largest rare earth resource bases. But in critical minerals, geology is not power. Power comes when reserves are converted into permitted projects, processing capacity, long-term offtake, industrial know-how and bargaining leverage.

That is why the proposed acquisition of Serra Verde by USA Rare Earth is more than a corporate transaction. It is a test of Brazil’s critical minerals strategy, and of the West’s ability to build a rare earth supply chain outside China.

Serra Verde’s Pela Ema operation, in Goiás, is not just another mining asset. It is Brazil’s only producing rare earth mine and one of the few ionic clay projects outside China capable of supplying the magnetic rare earths that matter most for the energy transition, defense systems and advanced manufacturing: neodymium, praseodymium, dysprosium and terbium.

These are not abstract inputs. They are essential for permanent magnets used in electric vehicles, wind turbines, robotics, defense applications, advanced electronics and high-performance motors. The strategic bottleneck, however, is not simply mining. The real choke points are separation, processing, alloying and magnet manufacturing, the industrial middle of the chain where China remains dominant.

That is what makes Serra Verde strategically important. It is not just about Brazil producing rare earth concentrate. It is about whether Brazilian rare earths become part of a functioning non-Chinese mine-to-magnet chain.

The USA Rare Earth proposal points exactly in that direction. The logic is to connect Brazilian upstream supply with processing, separation and magnet manufacturing capacity in the United States and allied jurisdictions. In theory, this is precisely the kind of integration Western governments say they want: secure supply, reduced dependence on China and a more resilient industrial base.

But for Brazil, the transaction poses a harder question: will the country use this moment to build strategic autonomy, or will it repeat the familiar Latin American pattern of exporting raw materials while others capture the industrial value?

This is the core dilemma.

On one hand, Brazil needs capital, technology, offtake agreements and industrial partners. Rare earth projects are technically complex, capital intensive and commercially difficult. Without credible buyers and downstream integration, even world-class resources can remain stranded. Foreign capital is not the problem. In fact, it may be essential.

On the other hand, Brazil does not want to become merely the upstream supplier in somebody else’s industrial strategy. President Luiz Inácio Lula da Silva’s policy direction has increasingly emphasized domestic value addition, local processing and greater state capacity around strategic minerals. Brazil’s emerging National Policy on Critical and Strategic Minerals reflects that ambition: the country wants to move beyond a geology-led approach and toward an industrial policy framework.

That is why the CADE antitrust review of the USA Rare Earth–Serra Verde transaction deserves to be read in a broader context. The issue is not only whether the transaction reduces competition in a narrow market. The more important question is whether Brazil can attract strategic capital while preserving enough leverage to shape the development of its own critical minerals industry.

If Brazil blocks or delays transactions without clear rules, it risks scaring away the very capital and technology needed to develop its rare earth potential. But if it approves strategic deals without demanding a credible pathway for local value creation, it risks locking itself into a subordinate role in the global supply chain.

Neither extreme serves Brazil’s interest.

A smarter approach would be to treat Serra Verde as a test case for a new model of critical minerals development: open to foreign capital, but anchored in transparent commitments on local processing, technology transfer, environmental standards, workforce development and long-term industrial participation.

That does not mean forcing every stage of the value chain to be built in Brazil immediately. Rare earth separation and magnet manufacturing are specialized, technically demanding and difficult to scale. But it does mean ensuring that Brazil does not lose strategic optionality at the very moment its resources are becoming geopolitically valuable.

The timing matters. The United States is urgently trying to reduce dependence on China for magnet materials. China is reinforcing its dominance through processing capacity, pricing power and export controls. Europe wants resilience but still lacks sufficient upstream and midstream capacity. Brazil, meanwhile, has resources, political relevance and a growing desire to be treated as more than a commodity exporter.

This triangular dynamic gives Brazil leverage. But leverage only exists if it is used with discipline.

The broader lesson extends beyond Brazil. Latin America has often been rich in minerals and poor in industrial capture. Copper, lithium, iron ore and now rare earths all point to the same challenge. Countries with mineral endowments can gain influence only if they build institutions, permitting capacity, infrastructure, financing mechanisms and commercial strategies that turn geology into industrial power.

Chile’s Penco Module, developed by Aclara Resources, illustrates the same point from another angle. It is one of the few advanced rare earth projects in the Western Hemisphere with the potential to connect upstream supply to a non-Chinese value chain. But like Serra Verde, its relevance depends not only on the orebody. It depends on permitting, financing, processing routes, environmental credibility and downstream integration.

The scarcity of such projects is precisely what makes Brazil’s decision so important. The West does not have a deep pipeline of ready-to-scale rare earth assets. If Serra Verde can be integrated into a credible mine-to-magnet platform while also supporting Brazil’s industrial ambitions, it could become a model. If not, it may become another example of how resource-rich countries miss moments of strategic opportunity.

Brazil’s rare earth dilemma is therefore not whether to accept foreign capital or reject it. The real question is how to negotiate from a position of strategic clarity.

The country should not confuse sovereignty with isolation. Nor should it confuse investment attraction with passivity. Strategic autonomy in critical minerals will not come from keeping assets untouched, but from structuring deals that convert natural resources into lasting industrial capabilities.

In rare earths, the next phase of competition will not be won by the countries with the largest reserves on paper. It will be won by those able to build functioning supply chains, from mining and processing to magnets, recycling and long-term industrial demand.

Brazil has the geology. The United States and Europe have demand, technology and geopolitical urgency. China still has the dominant position. What remains scarce is execution.

Serra Verde will show whether Brazil can bridge that gap, or whether rare earths will become the latest chapter in Latin America’s long history of exporting strategic minerals while others define the industrial future.

* Juan Cristóbal Ciudad is senior market and industry analyst at Plusmining consultancy

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments