China on recovery drive, but risk generator in metals markets – report

The Asia mining landscape faced a challenging growth outlook in 2020 with the covid-19 pandemic casting a shadow on mineral production growth as operations slowed and metal prices disappointed, but Fitch Solutions expects the worst to be over, the market analyst said in its latest industry report.

Fitch expects Chinese mining operations to continue in full gear since the ramp-up in H220 as government stimulus towards infrastructure sustains demand and industrial metals prices. Nevertheless, risks are high and Chinese economic data will continue to stoke volatility in metal markets, whether from a price or actual trade flow perspective, Fitch warns.

The pandemic put a dent in Asia’s mineral production growth in 2020, but Fitch forecasts a recovery in 2021 led by China. The analyst forecasts Asia to register a mining industry value growth of 1.8% y-o-y in 2021 after an estimated contraction of 3.4% y-o-y in 2020.

Fitch believes that China will lead the Asian, as well as global mining production recovery in 2021 as the country’s economy continues on the V-shaped recovery path since H220, sustaining demand for metals through a buoyant infrastructure sector boosted by government stimulus to accelerate the post-covid-19 recovery.

China on strong recovery drive, but remains overarching risk generator in metals markets

China has embarked on a strong recovery since lockdowns were lifted in April 2020, ramping up mining production, which Fitch expects to continue in 2021. Chinese macroeconomic policy has attempted to cushion domestic industries from the negative effects of covid-19, and Fitch’s Country Risk team forecasts real GDP to grow by 10.2% in 2021 after slowing to 1.9% y-o-y in 2020.

Fitch expects government stimulus (especially in the infrastructure sector) to continue to support demand for metals and minerals. The Country Risk team believes that stimulus, while targeted and measured, will be sustained in 2021 compared with that implemented in 2018 and 2019.

In regard to this, Fitch believes demand and price outlooks for non-ferrous metals including aluminium and copper will also fare better in 2021 compared with 2020, as the autos and consumer sectors that account for a large portion of non-ferrous metals demand suffered blows in 2020.

As a caveat, Fitch highlights downside risks to this view, as the country’s consumer and autos sectors will face a slow recovery in 2021, with the Autos team expecting vehicle sales to grow by only 5.1% y-o-y in 2021 after a contraction of 18.4% y-o-y in 2020.

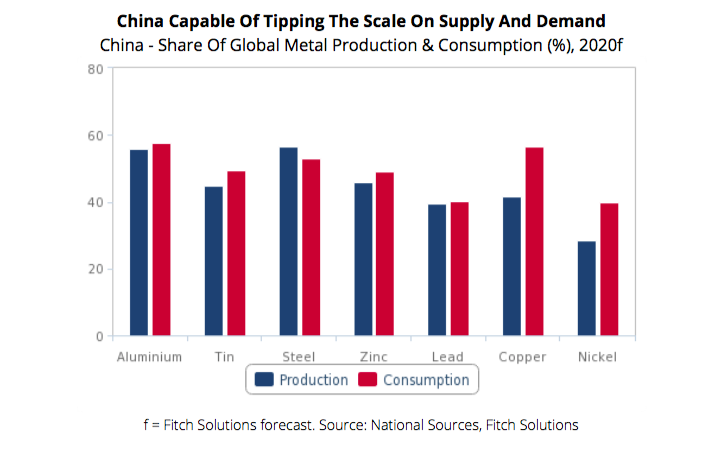

Economic data stemming from China will continue to spur volatility in metals markets, with the country being the largest global producer and consumer of metals, and Fitch will be revising forecasts for mineral and metal production growth in China as data are released.

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments