Why Tesla isn’t a “battery company”

Martin Eberhard and Marc Tarpenning founded Tesla Motors in 2003. The first production model rolled off the line five years later, and shortly thereafter Elon Musk became CEO.

Traditional carmakers remained asleep at the wheel of their oil burners for almost a decade after the first Tesla hit the road.

Tesla’s relative valuation shows investors regard the age of the internal combustion engine as well and truly over

Astonishingly, it wasn’t until 2017 that executives at the world’s largest auto companies identified battery electric vehicles as the top trend in the industry.

While announcements by incumbents of going electric and spending x amount of billions doing so have come thick and fast since then, Tesla is still way out front.

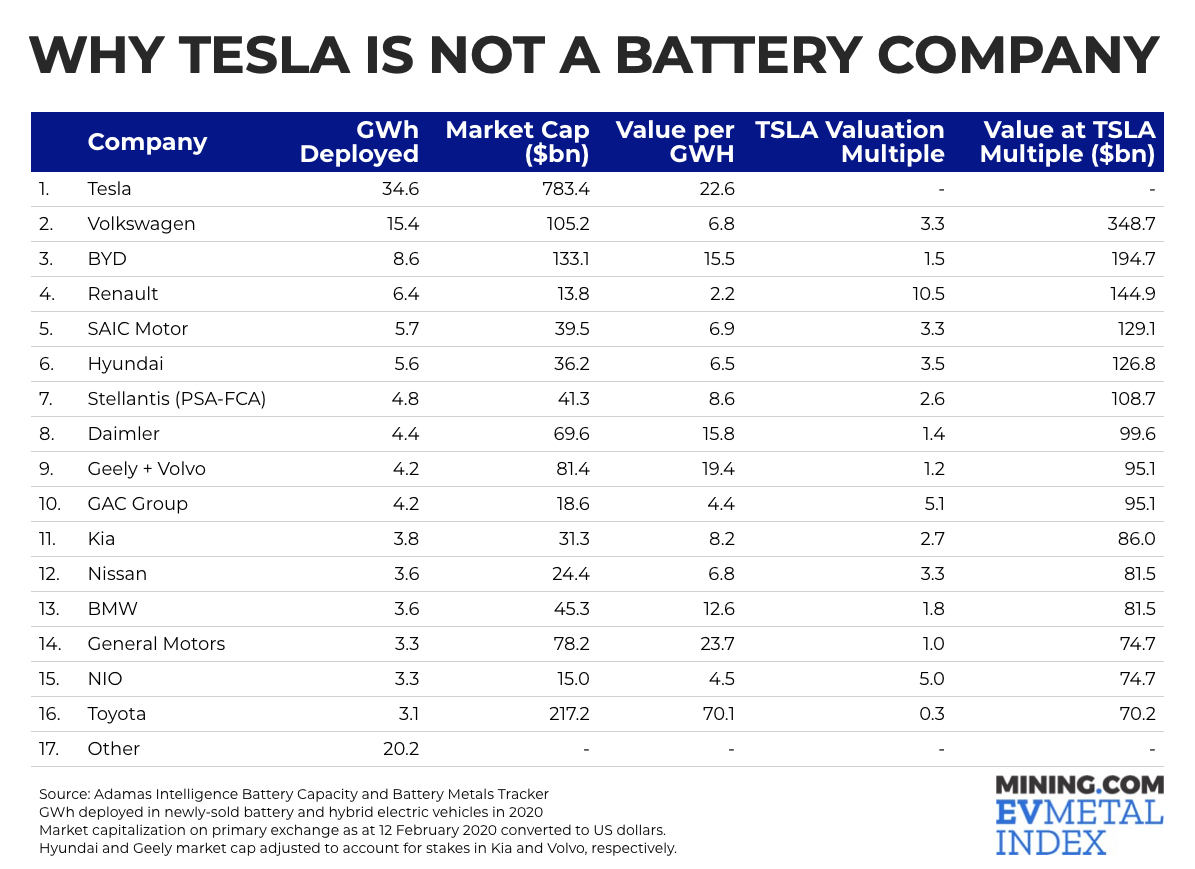

Last year the company was responsible for one in every four MWh hours in passenger cars hitting the road. In 2020, Tesla deployed more battery capacity than its four nearest competitors combined.

ICE, ICE bye bye

Shorting Tesla has been a widowmaker trade and fans of the company and its CEO amped up the stock over 700% in 2020, and double digits so far this year.

With a market capitalisation around $800 billion, TSLA is worth more than the next nine auto companies combined.

Tesla’s relative valuation shows investors regard the age of the internal combustion engine as well and truly over.

No matter how many diesel and gasoline cars the likes of Toyota, Volkswagen, GM, Renault, Hyundai et al sell – around 64 million in 2020, the worst year in decades – it’s all for naught.

To test this theory, MINING.COM assigned a value of zero to Tesla competitors’ traditional vehicle business.

This way investors can compare traditional automakers with Tesla based on their ability to compete in the battery powered light duty vehicle market.

Giga whaaat?

Longs love the company so much they rate Tesla batteries as having more value than those in the EVs of competitors – often supplied by the very same cell manufacturers.

At Tesla’s current market valuation, every GWh in the company’s cars sold last year is worth nearly $23 billion in market cap.

The company’s closest competitor Volkswagen attracts less than $7 billion for the same achievement.

Volkswagen would be worth $350 billion if investors were as charged up about its electric cars as they are about Tesla’s.

Again, it’s electric cars only – anything else Wolfsburg produces is worthless under this scenario.

Those Bugattis and Bentleys? Not even worth anything as scrap metal.

iPhones with wheels

BYD, which unlike Tesla, already manufactures its own cells, is significantly higher valued than the European marques on a cell-for-cell basis.

But if investors built their dreams around BYD like they do around Tesla, the Chinese company beloved by Buffett would be worth $60 billion (or 4.5 Renaults) more.

Renault is the most underrated EV-maker (maybe investors just don’t believe it’s Avantime enough).

Apple-Hyundai rumours became Apple-Renault rumours last week, but even the idea of French-made iphones on wheels could not grab the imagination of investors or attract dollars to Boulogne-Billancourt.

Renault’s Zoe last year also overtook the Model 3 to become the best-selling electric car in Europe, but investors believe the Zoe’s 52KWh is worth a tenth of the 50KWh in the Model 3 (granted, the Zoe’s touch screen is only a 7-inch and it doesn’t have Mode Ridicule).

China’s Tesla and… did you say Stellantis?

NIO, which almost always gets called China’s version of Tesla, hasn’t been able to get much of that valuation magic rub off either. If anyone really thought NIO was China’s Tesla it would be worth $58 billion (or 4.5 Renaults) more.

Then there’s Stellantis – freshly formed from Peugeot, Chrysler and Fiat.

Stellantis.

Sounds like an electric car company. Clearly investors don’t think it is.

Conspicuous by their absence are Ford and Honda, which between them could only muster little over 1 GWh last year.

Like Toyota, the relative size of the companies and the limited number of battery-powered cars they sell, inevitably assign a high value to these company’s on a GWh basis.

In the upside down world of electric car company valuations, once the Fords, Hondas and Toyotas start to catch up, expect the ratio to go in reverse.

(Toyota and Honda’s “mind-bogglingly stupid, staggeringly dumb” fuel cell vehicles are not accounted for in this analysis.)

TSLA la land

When confronted with talk of a bubble in Tesla stock, fans would often counter that Tesla is not a car company, it’s a battery company.

Of all the justifications for Tesla’s sky-high market cap, robotaxi is the one trotted out most frequently

Don’t know what that makes Tesla’s cell suppliers Panasonic, CATL and LG Chem, but okay.

Also, the accompanying table.

When that doesn’t work it becomes: Tesla is not a car company, it’s a tech company (or an insurance and HVAC company).

Full self driving, over the air updates, really really big touch screens, yottabytes of driving data fed into AI, factories you can see from space, cars you send into space, bitcoin, Plaid+ and all that.

The robotaxi rationale

Of all the tech justifications for Tesla’s sky-high market cap, robotaxi is the one trotted out most frequently, including by Musk, who recently mused that using Teslas as robotaxis increases the cars’ utility by a factor of five and by extension, the company making them.

“There is a more than 30 per cent chance in our view that Tesla is the autonomous taxi network of the US,” ETF superstar Cathie Wood of Ark Investment Management, and Tesla cheerleader in chief told the FT last week.

Only more than 30%?

Perhaps Wood saw this video from September of a Model 3 navigating the Consumer Reports parking lot.

One of the many arguments against the robotaxi rationale for Tesla at $800 billion and beyond is that fully self-driving cars are at least 10 years away.

Judging by the video, it could take a little longer.

More News

Codelco debt and high costs hurt competitiveness, document says

July 02, 2026 | 07:28 am

Congo plans first stock market as AI mineral boom draws interest

July 02, 2026 | 06:49 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

2 Comments

Gaetano

Of course this bear has a huge short bet against Tesla and links directly to a paid for consumer reports video link. Thanks for helping us get Tsla shares on sale.

Ian

It’s not just about the cars. It’s about thr total solution that Tesla offers. Range is critical – something other manufacturers are finally doing something about. Charging infrastructure is also critical to EV adoption – something no other automotive manufacturer seems to accept. If you’ve owned and driven a non Tesla EV, and tried to go on a longer trip, you have to plan carefully for charging, and hope and pray the 3rd party that owns that one lone charger has kept it in working condition. With a Tesla, that big picture is a fundamental part of the overall systems’ plan and design.