In charts: EV metal demand accelerated in the second half of 2021

A 62% jump in passenger electric vehicles (EV) registrations in the second half of 2021 to 5.84 million units continues to drive an intensifying demand in the battery metals sector, the latest data release from Adamas Intelligence shows.

According to the market analyst, an 86% increase in passenger EV registrations in the Asia Pacific region positions it as the top EV market, followed by the Americas (51% year-over-year) and Europe (34% year-over-year).

The watt-hours deployed in the Asia Pacific region in the second half of 2021 rose 141% over the same period in 2020, contributing a corresponding 134% increase in lithium, 77% increase in nickel and 75% increase in cobalt consumption over the same period.

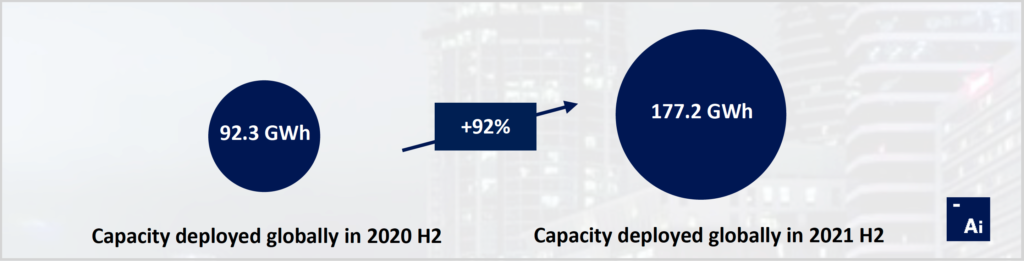

In the second half, the total global battery capacity deployed onto roads in all newly sold passenger EVs combined amounted to 177.2 GWh, 92% more than was deployed globally a year earlier.

Tesla (Nasdaq: TSLA; NEO: TSLA) continued to lead by battery capacity deployed onto roads globally, installing more watt-hours into newly sold EVs than its five closest competitors combined.

Adamas says just seven cell suppliers globally (CATL, LG Energy Solution, Panasonic, BYD, Samsung SDI, SK On and CALB) were collectively responsible for more than 88% of all battery capacity and battery metals deployed onto roads globally in passenger EVs in the second half of 2021.

During the period, global leader CATL deployed 183% more watt-hours of battery capacity onto roads worldwide than the 2020 period, translating to a 171% increase in lithium, 138% increase in nickel, and 114% increase in cobalt deployed onto roads over the same period prior.

The deployment of lithium-iron-phosphate LFP cells (in watt-hours) increased 426% over the last six months of 2020, leading to a drop in the average amount of nickel (-2%) and cobalt (-9%) consumed per EV sold.

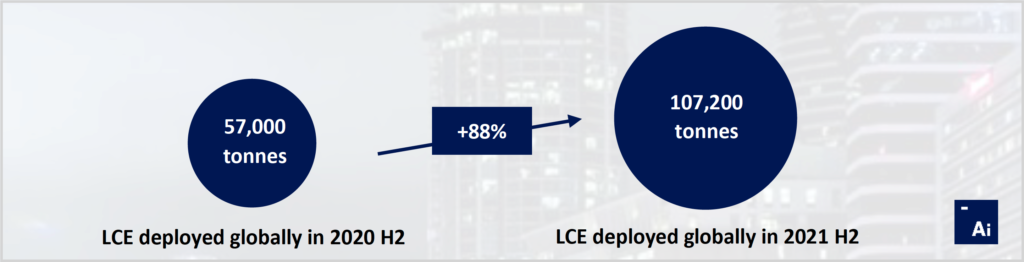

The increasing rates of EV deployment translate into increased metal demand. During the second half of 2021, another 107,200 tonnes of lithium carbonate equivalent (LCE) were deployed onto roads globally in the batteries of all newly sold passenger EVs combined, Adamas says. That is an 88% increase year-on-year. About 56% of all LCE units were deployed as carbonate and 44% as hydroxide.

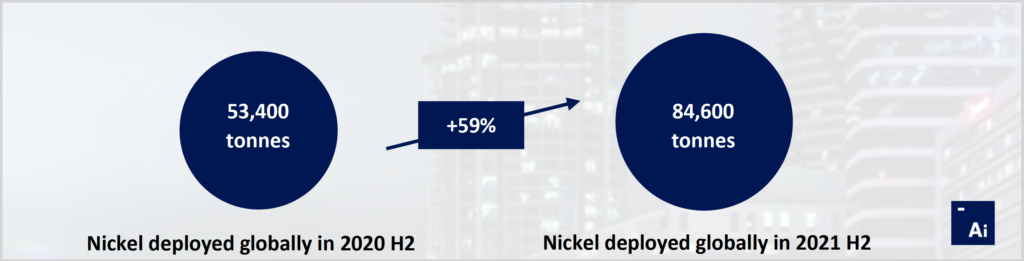

Moreover, in 2021 H2, 84,600 tonnes of nickel were deployed onto roads globally in the batteries of all newly sold passenger EVs combined, 59% more than in 2020 H2.

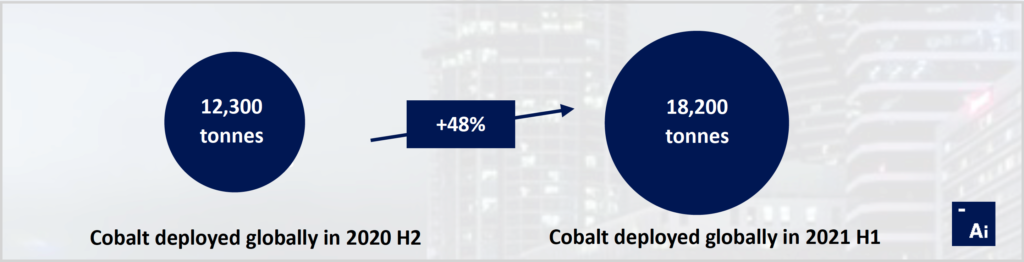

This also meant surging cobalt demand. In 2021 H2, 18,200 tonnes of cobalt, 23,600 tonnes of manganese, and 159,200 tonnes of graphite were deployed onto roads globally in the batteries of all newly sold passenger EVs combined, up 48%, 62% and 101% over the same period the year prior, respectively.

In 2021 H2, Tesla deployed over 1,500 tonnes of cobalt onto roads globally, 17% more than it deployed in EV batteries in 2020 H2 and roughly twice as much as the next two in line. Mercedes deployed 790 tonnes of cobalt onto roads globally in 2021 H2, an increase of 28% over 2020 H2, Hyundai deployed 740 tonnes, an increase of 20% over 2020 H2.

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments