Iron ore price bounces back while Fitch sees rally slowing ahead

Iron ore prices rose on Wednesday, after five straight sessions of losses, tracking steel futures as China’s output curbs fuelled supply worries.

According to Fastmarkets MB, benchmark 62% Fe fines imported into Northern China were changing hands for $165.48 a tonne, up 1.8% from Tuesday’s closing.

The most-traded iron ore for January 2022 delivery on China’s Dalian Commodity Exchange ended daytime trading up 3.7% at 871.50 yuan ($134.33) a tonne, after hitting its lowest since March 26 in the previous session.

Shanghai steel futures rose for a second day to their highest level in nearly two weeks on supply worries.

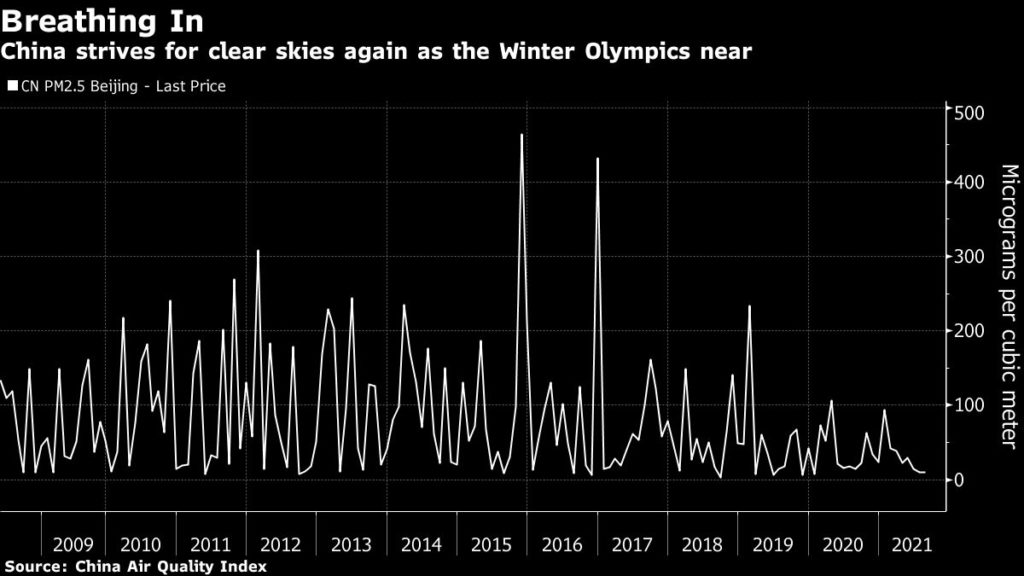

Mills in China have been asked to reduce output starting July to limit full-year production to no more than the 2020 volume to cut emission levels.

The ongoing curbs have dampened iron ore demand, bringing spot prices to the lowest levels in more than four months, SteelHome consultancy data showed.

The restrictions may be extended until March 2022, and possibly even intensified ahead of the Beijing Winter Olympics in February. A draft plan on controlling air quality in the steel hub Tangshan city during the games has been circulating online.

“Pressure remains on iron ore futures in China amid fear that restrictions on steel output will last longer than expected,” said ANZ senior commodity strategist Daniel Hynes.

Rally weakening

“The iron-ore price rally is finally starting to show signs of weakening, which will continue into coming months,” said market analyst Fitch Solutions.

Fitch says the price of iron ore is likely to drop from the expected $170 a tonne by year-end to $130 in 2022, $100 by 2023 and ultimately $75 by 2025.

According to the agency, improving production growth from Vale, Rio Tinto and BHP has started to loosen tight supplies on the seaborne market.

Fitch forecasts that global mine output will grow by an average of 2.4% from 2021 to 2025, compared with the 2% contraction observed over the previous five years.

(With files from Reuters and Bloomberg)

More News

Canacol gas curbs force Colombia’s Cerro Matoso ferronickel mine to cut output

Cerro Matoso said it was cutting operations by 25%.

July 01, 2026 | 10:01 am

GreenMet plans $150M rare earth processing hub in West Virginia

July 01, 2026 | 09:36 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments