Iron ore price expected to ease over next 5 years on slower demand growth and more supply

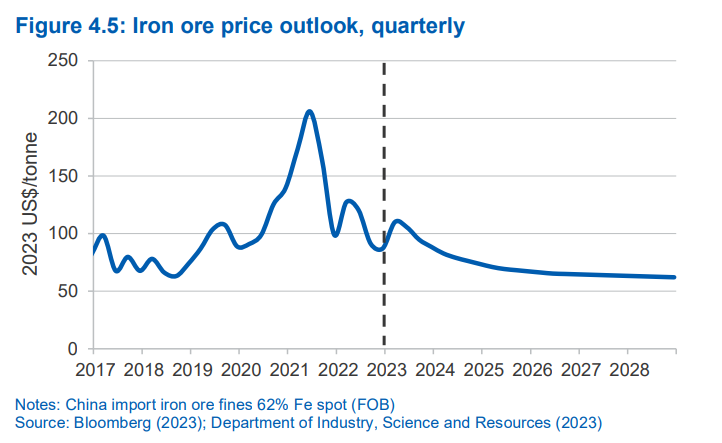

Despite iron ore rebounding strongly in early 2023, after falling more than 50% in the second half of 2022, prices are expected to ease over the next 5 years on slower demand growth and more supply.

The higher prices seen in recent months reflect a partial recovery in Chinese steel production, as the country reopens following the end of the zero-covid policy.

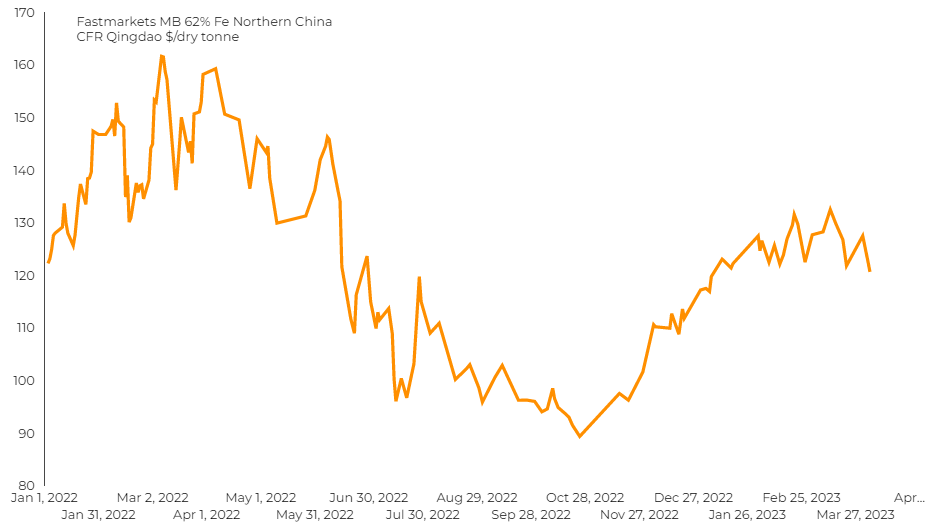

Benchmark 62% Fe fines imported into Northern China fell 1.47% on Tuesday, to $120.65 per tonne, pressured by higher shipments and fears about government intervention.

Fitch Solutions Country Risk and Industry Research recently revised its iron ore price forecast for 2023 from $110 a tonne to $125 a tonne.

“Mainland China’s recovery from its two structural headwinds (zero-Covid policy and real estate sector reform) will support iron ore prices in the short term,” the market analyst said in its latest report.

“On the supply side, we expect a steady production level across major producers. Many have posted stronger productions quarter-on-quarter, while production guidance is expected to grow marginally,” Fitch said.

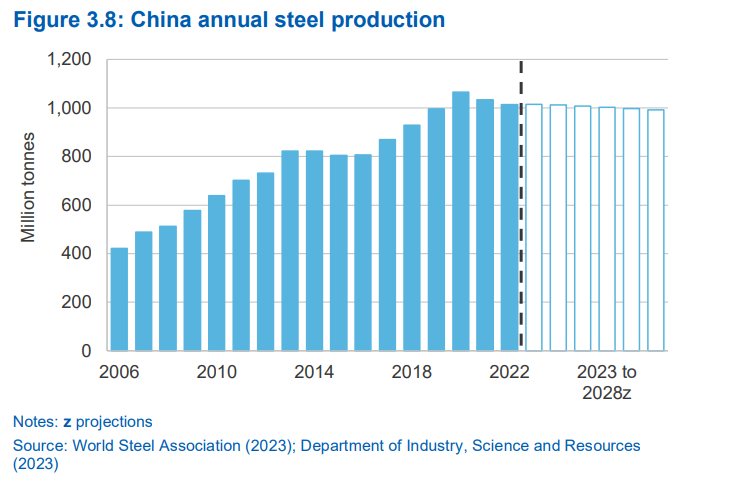

However, with China projected to see a mild decline in total steel production in the next 5 years, a softer rate of growth (0.9% annually) is expected in global iron ore demand, according to a recent report from the Australian Government.

China accounted for 57% of global iron ore demand in 2022. Demand is expected to decrease as the country aims to reach peak steel output by 2030 in an effort to reduce carbon emissions.

“China’s efforts to reduce aggregate steel output are expected to support a longer-term shift in its economy away from investment-led (and toward consumption-led) growth,” Fitch said.

With the country announcing its first decline in population in over six decades in 2022, a more modest rate of growth for the Chinese economy is also expected to support the trend.

Global supply is expected to grow by 3.1% annually until 2028, with new supply coming online in Australia, Brazil and Africa.

Australia is projected to see a continued ramp-up of greenfield projects from Rio Tinto, BHP and Fortescue, and emerging producers such as Mineral Resources Limited and Atlas Iron.

Brazil is expected to grow iron ore exports by around 6% annually until 2028.

In Africa, Guinea’s government recently restarted the development of the massive Simandou mine, expected to produce 150 million tonnes per annum.

In the long term, Fitch expects prices to decline to $50 a tonne by 2032.

More News

Canacol gas curbs force Colombia’s Cerro Matoso ferronickel mine to cut output

Cerro Matoso said it was cutting operations by 25%.

July 01, 2026 | 10:01 am

GreenMet plans $150M rare earth processing hub in West Virginia

July 01, 2026 | 09:36 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments