Kaminak Gold announces positive feasibility

Kaminak says it plans to move forward with mine permitting for its Coffee Gold project in the Yukon after receiving a positive feasibility study.

The gold junior announced after-tax NPV 5% of CAN$455 million and IRR of 37 %; average life of mine annual gold production of 184,000 ounces and all-in sustaining costs of us$550/oz au.

The Coffee project is located 130 km south of Dawson City in Yukon Territory, Canada.

“The Coffee Project further benefits from being a simple, open pit, heap leach mining opportunity, situated near infrastructure that delivers low all in sustaining costs and pays back capital in under two years,” said Eira Thomas, Kaminak President and CEO.

Full news release is below:

Kaminak Gold Corporation Announces Positive Feasibility Study Results On Yukon Coffee Gold Project

View News Release in PDF Format

After-Tax NPV5% of C$455 million and IRR of 37 %; Average Life of Mine Annual Gold Production of 184,000 Ounces and All-In Sustaining Costs of US$550/oz Au

January 6, 2016

Vancouver, B.C. – Kaminak Gold Corporation (“Kaminak” or the “Company”) (KAM: TSX-V) is pleased to announce the results of a Feasibility Study prepared in accordance with National Instrument 43-101 (NI 43-101) for the Company’s 100% owned Coffee Gold Project (the “Coffee Project”) located 130 km south of Dawson City in Yukon Territory, Canada. The Feasibility Study indicates that the Coffee Project represents a robust, rapid pay-back, high margin, ten year open pit mining and heap leach project that works in the current gold price environment. As such, Kaminak intends to move forward into mine permitting to support mine construction, which is planned for mid-2018. The Company is well financed ($28 million as of September 30, 2015) to undertake an aggressive work-plan in 2016 to meet these objectives.

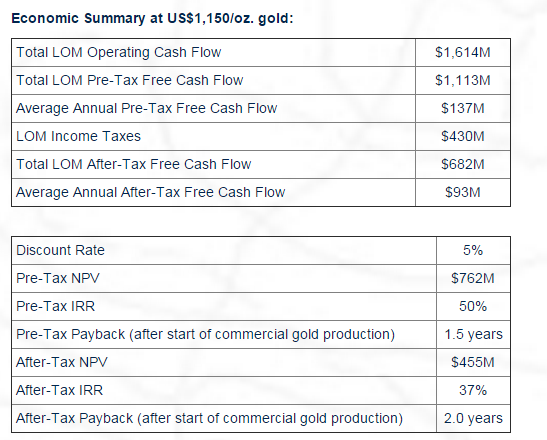

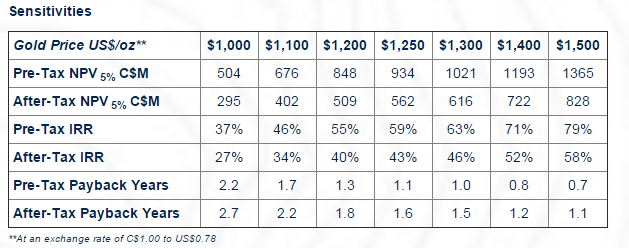

At a gold price of US$1,150/oz and an exchange rate of C$1.00 to US$0.78, the Coffee Project base case estimate (the “Base Case”) generates an after-tax net present value (NPV) at a 5% discount rate of C$455 million and an internal rate of return (IRR) of 37%. The proposed mine will operate over an initial ten year mine-life with average annual gold production in excess of 200,000 ounces for the first five years (excluding the initial 3 month ramp-up period), and average annual life-of-mine gold production of 184,000 ounces. Initial capital expenditure to fund construction and commissioning is estimated at C$317 million, with a life-of-mine capital cost of C$478 million (including C$60 million in closure costs). The all-in sustaining cash costs (as defined per World Gold Council guidelines, less corporate G&A) is estimated to be US$550 per ounce of gold produced. The project is expected to have a significant impact on Yukon’s GDP, generating over $2 billion of gross revenue and contributing 480 permanent, high paying jobs.

Eira Thomas, Kaminak President and CEO commented: “This feasibility study firmly establishes the Coffee Project as one of the world’s best undeveloped gold projects by value and margin that works in the current gold-price environment. The Coffee Project further benefits from being a simple, open pit, heap leach mining opportunity, situated near infrastructure that delivers low all in sustaining costs and pays back capital in under two years”. She further noted, “Kaminak feels privileged to be working in the pro-mining jurisdiction of Yukon where we enjoy strong relations with all levels of government, including our local First Nations, with whom we have worked alongside, collaboratively since 2010.”

Accompanying this news release is a video corporate presentation given by Eira Thomas, Kaminak President & CEO, discussing the Feasibility Study and available for viewing by clicking the following link: https://www.webcaster4.com/Webcast/Page/1369/12606, or by visiting the Kaminak website, www.kaminak.com.

Furthermore, Kaminak is hosting a live Q&A conference call on Thursday, January 7th at 11:00 a.m. Eastern time (8:00 a.m. Pacific time) with the Kaminak Executive and Feasibility Study team. Participants may join the call by dialing toll-free North America (866) 393-4306 or International (734) 385-2616 and providing the company name (Kaminak Gold Corporation) to the operator. A recorded playback of the call will be available two hours after the call’s completion until January 21st, 2016 by dialing (855) 859-2056 and entering the conference ID#: 17824557, and on the Kaminak website.

Coffee Project Feasibility Study Overview

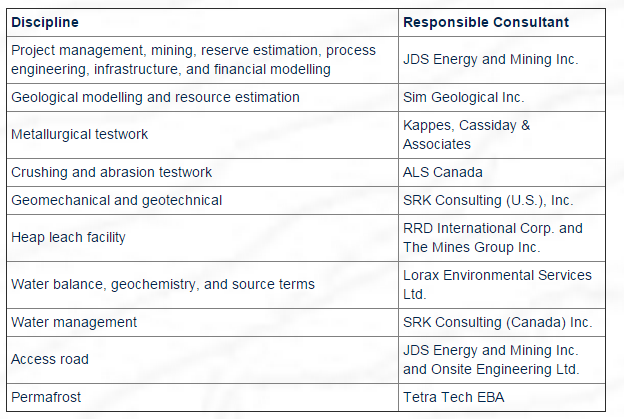

The Feasibility Study was initiated in July 2014 after the release of the Preliminary Economic Assessment in June 2014 and commenced with infill drilling, geotechnical investigations and other fieldwork to support the study. The Feasibility Study was prepared and led by JDS Energy and Mining Inc. (JDS), an established Yukon mine builder, in collaboration with a broad range of industry leading consultants (see Contributors below),

Highlights (all currencies are reported in Canadian dollars unless otherwise specified):

- A pre-tax NPV5% and IRR of $762 million and 50% respectively;

- An after-tax NPV5% and IRR of $455 million and 37% respectively;

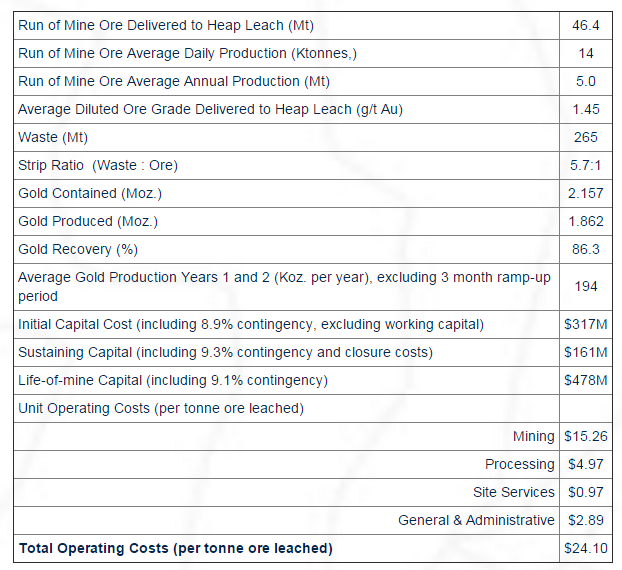

A mine life of ten years with peak annual gold production of 228,000 ounces in project Year 4 and average, steady state, annual gold production of 193,000 ounces (Years 1-9);- 2,157,000 ounces of gold mined at head grade of 1.45 g/t Au (Probable Mineral Reserve of 46.4 Mt at 1.45 g/t Au, containing 2.157 Moz Au.);

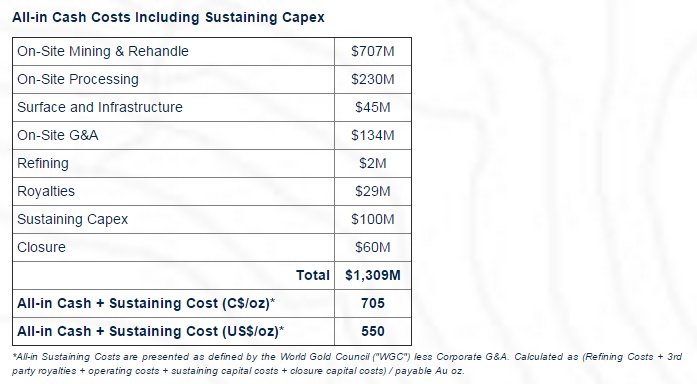

1,862,000 ounces of gold produced after average metallurgical gold recoveries of 86.3%;- Total cash cost estimated at US$482 /oz Au (including royalties, refining and transport) and an all-in sustaining cost (as defined by the World Gold Council less Corporate G&A) estimated at US$550/oz Au, generating an operating margin of US$600/oz or 52%;

- Initial and sustaining capital costs, including contingency, for a 100% owner-operated mine are estimated at $317 million and $161 million (including $60 million in closure costs) respectively; and

- A payback of 1.5 years pre-tax and 2.0 years after-tax after the commencement of first commercial gold production;

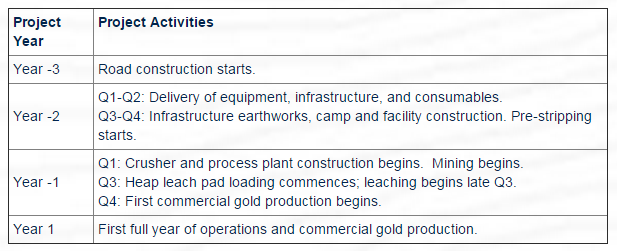

The Feasibility Study proposes four open pits mined by conventional shovel and truck methods at a nominal ore mining rate of 5 million tonnes per annum for approximately ten years (with Year 1 being the first full year of commercial gold production). A total of 312 Mt of material will be mined to produce 46.4 Mt of ore (strip ratio of 5.7 : 1). Run-of-mine ore will be crushed to a 2-inch feed size and placed on a heap leach pad. Gold will be extracted from the leachate by an Adsorption-Desorption-Recovery (ADR) carbon plant.

The site will be accessed principally from Dawson City, Yukon, by a 214 km single-lane, gravel road with pullouts. The cost associated with upgrading existing road and to construct approximately 37 km of new road along the proposed 214 km route is estimated at approximately $25 million. Electrical power will be generated on site by diesel-powered generators. Project construction time from site mobilization to first commercial production of gold is estimated to be 18 months, excluding access road construction which will take approximately 9 months.

Comparison to the June 2014 Preliminary Economic Assessment (PEA)

The PEA presented a broadly similar operation to the Feasibility Study. The key differences from the PEA presented in the Feasibility Study include:

- Total ounces unchanged, with a shorter mine life, higher head grade, lower reserve tonnage, and higher strip ratio;

- Increased average total mining rate from approximately 64,000 tonnes per day (tpd) to approximately 92,000 tpd;

- A ridge-top heap leach pad with a shorter initial construction period and lower capital cost per tonne of ore leached than the valley-fill impounding heap leach facility proposed in the PEA;

- An access road from Dawson City utilizing a high proportion of existing gravel roads; and

- Improved economics due to a shorter construction period, shorter mine life and higher average gold grade.

Coffee Gold Feasibility Study Assumptions and Economic Results

The tables below summarize the various assumptions, operational parameters and economic results of the Feasibility Study. All money values are nominal 2015 Canadian dollars unless otherwise stated.

The following assumptions were applied only in the derivation of the after-tax valuation of the project:

- Pre-development and sunk costs relating to the project (including but not restricted to exploration and geotechnical investigations, resource evaluation, fieldwork, metallurgical testwork, environmental and baseline studies costs, technical studies);

- Canadian Exploration Expense (CEE) and Canadian Development Expense (CDE) tax pools with appropriate opening balances;

- Applicable private and Yukon Crown royalties;

- Federal and Yukon Territory tax rates; and

- Specific capital cost class Capital Cost Allowance (CCA) rates over the life of the project.

The following inputs were assumed for the project:

- Gold Price of US$1,150 / oz.

- Exchange Rate (US$ : C$) of 0.78

- Diesel Price (delivered to site) of $0.85/ L for stationary equipment and $0.89 / L for mobile equipment.

Feasibility Study Operating Parameters

The Base Case set out above represents the value of the project from the known resources. The Base Case assumes an owner-operated open pit mine, access to site via a gravel road (approximately 295 days per annum) and diesel power generation. Mining will take place 365 days per annum, and the heap leach pad is planned to be operated 275 days per annum with no crushing and stacking of ore occurring during January through March.

Opportunities to Enhance Value

Value-enhancing opportunities, such as contract mining, the acquisition of high quality, second hand mining and ancillary equipment, crushing and process plant, and accommodation quarters, will be further investigated as the project moves into detailed engineering and procurement. As operations ramp up and a greater understanding of the ore and heap leach facility performance evolve, extending the duration of the crushing / stacking period, the period and temperature of solution heating, and increasing the size of the ore feeding the heap leach pad will be evaluated. Current oil prices indicate that diesel-only power generation is the most cost effective power option. As diesel prices increase, partial replacement of diesel with LNG will become more cost effective.

There is potential for resource expansion along strike and to depth, with two existing inferred gold resources (Kona North and Sumatra), and seven separate drill discoveries in the early stages of evaluation located proximal to the proposed mine site which contain more than 25 km of priority gold in soil anomalies remaining to be systematically drill-tested.

Coffee Project Feasibility Study Major Components

Metallurgy

Ore samples for metallurgical testing were taken from bulk surface samples and drill core composites. A total of 40 column tests were completed at both ambient lab and simulated cold-climate temperatures, composited from 4500 samples, representing 29,608 kg from 123 drill holes and 8 trenches (at ½”, 1”, 2” and 6”crush sizes). In addition to column leach tests, metallurgical testing included bottle roll leaching, flotation, column percolation and drain down, multi-element head assay analyses, column-leach head and tail assay screen analyses, ball mill work indices, crushing impact, and abrasion indices. Fire assays for gold and silver were also conducted. Major conclusions from the test program include:

- Coffee Project ores generally leach very rapidly with low reagent consumption

- Ore agglomeration is not required;

- Cyanide soluble assays from over 14,000 samples confirmed that cyanide soluble recovery is a reliable method to determine gold recovery;

- Differences in recovery observed between ambient lab temperature leach tests and simulate cold climate leach tests were negligible;

- Optimal gold recovery is achieved at an ore size of 80% passing a 50 mm screen size (P80 of 50 mm; 2”); and

- An average plant gold recovery of 86.3% was determined from metallurgical testwork results and after the application of discount factors (~3%) to simulate plant operating conditions.

Geology and Mineralization

The Coffee Project area is underlain by a package of metamorphosed Paleozoic rocks of the Yukon-Tanana Terrane comprising metasedimentary schist and orthogneiss which form a west-northwest plunging antiform with gently dipping limbs. The Palaeozoic sequence is intruded by Mid Cretaceous granite and younger intermediate dikes.

These units are host to gold mineralization that is hydrothermal in origin and structurally controlled, forming steeply dipping strike extensive mineralized lodes in broadly E-W, N-S and NE -SW trending structural corridors. Mineralization is associated with both polyphase brecciation and intense sulphidation of mica-rich host rocks resulting in the formation of gold-bearing arsenian pyrite. Extensive oxidation occurred due to ingress of meteoric water downwards and along the structural deformation zones. This process resulted in the oxidation of the arsenian pyrite along rims and cracks causing the release of micron-scale free gold.

Mineral Resource Estimate

The Feasibility Study is based on an Indicated Mineral Resource estimate undertaken by Robert Sim, P.Geo., an independent Qualified Person of SIM Geological Inc. (Kaminak News Release, September 23rd, 2015). The mineral resource estimate incorporated 1,682 diamond core and reverse circulation drill holes completed from 2010 to 2015 for a total of 280,000 metres. This estimate defines a total Indicated mineral resource of 63.7 million tonnes averaging 1.45 g/t Au for 2,968,000 ounces of contained gold, and a total Inferred mineral resource of 52.4 million tonnes at an average grade of 1.31 g/t Au for 2,212,000 ounces of contained gold. These mineral resources are inclusive of mineral reserves. Cut-off thresholds used in the resource estimate reflect the projected metallurgical characteristics at various degrees of oxidation; 0.3 g/t Au for Oxide and Upper Transition, 0.4g/t Au for Middle Transition and at 1 g/t Au for Lower Transition and Sulphide types.

A series of resource block models, covering the limits of the four deposit areas, were produced with gold grades estimated by ordinary kriging into model blocks measuring 10m along strike, 2.5m across strike and 5m in the vertical dimension. A capping strategy was employed to control the effects of potentially anomalous, high-grade, sample data during block grade interpolation. The ratio of cyanide soluble gold verses total gold content was utilized to assign the various Oxide ore types in the block models. Mineral resources are classified according to their proximity to sample locations and are reported according to the CIM Definition Standards for Mineral Resources and Mineral Reserves.

Mineral Reserve Estimate

The Mineral Reserve for the Property was estimated by Dino Pilotto, P.Eng., an independent Qualified Person of JDS.

Cut-off grades, ranging from 0.27 to 1.40 g/t, were determined for each deposit and ore type and based on appropriate mine design criteria and the adopted mining method. The Mineral Reserves were estimated at a gold price of US$1,200 / oz., and an exchange rate of C$1.00 to US$0.87, with the application of dilution and recovery factors appropriate to an open pit mining method. The factors applied to generate the pit shells were the best estimate of gold price and exchange rate at the time the pit shells were generated. These factors were not those utilized to generate the final project economics, but reserve estimates using the lower gold price and exchange rate indicate that there were not any material differences. Pit optimizations and analyses were conducted to determine the optimal mining shells.

As input to the initial pit limit optimization and subsequent mine scheduling, and in order to reflect the selectivity of the mining method chosen when compared to the block model parameters, an external mining dilution was calculated and applied for each of the various deposits. This external mining dilution was based on a calculation of the number of waste blocks adjacent to an ore block in the mineral inventory block model. Only blocks which were contained within the resource classification of Indicated and above the given gold cut-off grade were considered as ore blocks.

Probable Mineral Reserves are estimated at 46.4 Mt at 1.45 g/t Au, containing 2.157 Moz Au.

Mining

An open pit, shovel and truck mining method was applied to the Coffee Project deposits. Mining is scheduled at the start of Year -1 in order to ensure the delivery of a minimum of 3.5 Mt of ore to the heap leach pad prior to the first winter shut-down, and to provide sufficient quantities of waste material to facilitate construction activities. Mining of the deposit is planned to produce a total of 46.4 Mt of ore and 265 Mt of waste (5.7:1 strip ratio) over a ten-year project production life, including the initial year of pre-production. Mining is planned to continue throughout the year. During the crusher and heap leach shutdown in the first three months of each year uncrushed ore will be stockpiled. The mine plan focuses on achieving consistent annual total material production rates of between 34 and 40 Mt, while ensuring a steady-state ore production rate of 5 Mt per annum.

The Supremo pit contributes approximately 71% (32.9 Mt) of the total ore and commences mining in Year 2 of the project. It is planned to remain in production to the end of mine life. The Latte (25%, 11.5 Mt), Double Double (2%, 1.1 Mt) and Kona (2%, 0.9 Mt) pits will contribute early production and will be completed by Year 3. This schedule endeavours to prioritize the early production of higher value material where practical.

Open pit mining operations will use a fleet comprising industry-standard 16 m3 shovels, 12 m3 front-end loaders, 4 m3 excavators, and 144 t haul trucks. This fleet will be supplemented by appropriately sized drills, graders, and dozers. A 5 m bench height was selected for mining in ore and waste with overall 20 m effective bench heights based on a quadruple-bench configuration. The handling of the fine ore from the crusher to the heap leach pad is included in the open pit scheduling and operating cost estimation.

Waste rock will be placed in three engineered waste rock facilities proximal to the pits from which the waste is sourced. Some waste rock will be backfilled into mined out pits at Latte, Supremo and Double Double in order to create causeways and facilitate ore haulage routes to the crusher. Waste rock from the Kona pit, due to its geochemical characteristics, will be placed in a temporary waste rock facility adjacent to the pit during mining and then backfilled into the mined-out Kona pit.

Processing

The process includes a two-stage crushing plant feeding a heap leach operation. Gold is extracted by an adsorption-desorption-recovery (ADR) carbon plant. The process is based on a heap leach processing rate of 5.0 million dry tonnes per year at an average feed grade of 1.45 g/t and an anticipated overall recovery of 86.3%. The crushing rate will be approximately 18,200 tpd over the 9-month operating period. The process plant, located in close proximity and at a lower elevation to the heap leach facility, minimizes pumping by allowing gravity feed of pregnant solution.

Crushed ore will be trucked to the heap leach facility and spread by dozer. Crushing and heap leach stacking will be suspended between January and March in order to maintain the thermal integrity of the heap. The heap leach facility will operate all year with the solution heated as necessary to maintain thermal integrity. The facility will be stacked progressively, in well-defined stages, from the east to the west.

Ore leaching will commence in the third quarter of Year -1. At the end of the fourth quarter approximately 3.5 Mt of ore will be available for leaching. Gold recovery will continue through the first quarter of Year 1 and ore crushing and stacking recommence in Q2 of Year 1. Progressive closure of the heap leach pad will commence in Year 4 as depleted areas of the facility become available for decommissioning, covering, and reclamation. The seasonal placement of synthetic geomembrane covers will aid in maintaining the thermal profile and controlling precipitation run-off.

Process water for leaching will be sourced from site contact water exclusively, except at the start of operations when a small amount of water may be sourced from surrounding creeks. Event and rainwater storage ponds will be constructed between the heap leach pad and the process plant.

Infrastructure and Project Execution

The following key infrastructure will support the mine and process facilities:

- A 214 km access road from the Klondike Highway turn-off 15km east of Dawson City, utilizing and upgrading existing roads where possible and requiring only approximately 37 km of new road construction to connect portions of existing isolated road. The Stewart and Yukon rivers will be crossed by barge in summer and ice roads in winter. During the fall freezing and spring breakup periods, each approximately 6 and 4 weeks respectively, the site will not be accessible by road. On-site storage for consumables accommodates a period of up to ten weeks without site access;

- A 1,200 m gravel airstrip;

- Truck work shop, warehouse, administration and camp accommodation;

- Bulk explosives storage and magazines;

- Power plant (installed capacity of 9 MW), initially diesel-fired but capable of partial LNG substitution;

- Diesel bulk storage tanks (for power generation, mining equipment and ANFO) with a ten week capacity;

- Potable water, fire water and sewage treatment systems; and

- Potable water to be trucked from the Yukon River;

Project operational time-line

Total manpower complements during construction and operations are estimated to peak at 480 and 435, respectively. During construction a peak, on-site labour force of 250 is anticipated. The peak, on-site operational labour complement is anticipated to be 225. Personnel will generally operate on a 2 week on – 2 week off shift rotation on a fly-in – fly-out basis.

Contributors

The Feasibility Study was undertaken and led by JDS Energy and Mining Inc., under the direction of project lead, Angus Christie, PhD., (JDS) with oversight and contributions from James Scott, MSc., P.Geo (Advanced Projects Manager, Kaminak) and Fred Lightner, P.E. (Director of Mining, Kaminak).

The following organizations contributed to the Feasibility Study:

Total manpower complements during construction and operations are estimated to peak at 480 and 435, respectively. During construction a peak, on-site labour force of 250 is anticipated. The peak, on-site operational labour complement is anticipated to be 225. Personnel will generally operate on a 2 week on – 2 week off shift rotation on a fly-in – fly-out basis.

Next Steps

With the results of the Feasibility Study now in hand, Kaminak will begin advancing the Project through the permitting process in Yukon. The Project will be subject to an environmental and socio-economic assessment under the Yukon Environmental and Socio-economic Assessment Act (YESAA), administered by the Yukon Environmental and Socio-Economic Assessment Board (YESAB). Kaminak has assembled a team of experts to assist the Company in the development of a Project Proposal which the Company plans to submit to YESAB in Q3 2016. Once through YESAB’s adequacy review, the Company will submit applications for a Quartz Mining Licence and Water Licence, the two major licences required for the construction and operation of a mine.

Kaminak’s disclosure of a technical or scientific nature in this press release has been reviewed and approved by James Scott, MSc., P.Geo, Advanced Projects Manager for Kaminak Gold Corporation, who serves as a Qualified Person under the definition of NI 43-101.

On behalf of the Board of Directors of Kaminak

“Eira Thomas”

President and CEO

Kaminak Gold Corporation

Photo of Tony Reda, Vice President of Corporate Development, at the Coffee Gold Project

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments