Nickel prices will continue to fall: BMI

A new report by BMI research says that refined nickel prices will continue to lose steam in the coming months due to increased supply from Indonesia, subdued demand from China and fading overly-optimistic demand expectations from electric vehicle production.

“We have kept our nickel price forecast at $10,000/tonne for 2018 and expect prices to head lower over our forecast period from 2017-2021 as the global nickel market surplus widens,” the firm says.

According to BMI, once investors realize that any significant impact of EV’s on nickel demand is still years away, prices will continue to go down from the current $11,295/tonne following an unexpected rally in the second half of 2017, which took them above $13,000/tonne.

“Further downside pressure on prices will emerge in the short term as the global nickel market shifts into a surplus. On the one hand, we expect stainless steel demand – which accounts for approximately 70% of all nickel consumption – to wane as the Chinese Government shifts policy away from heavy industry,” the business intelligence company predicts.

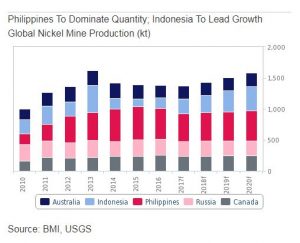

When it comes to supply, BMI foresees excess as Indonesia floods the market following the end of its ore export ban. To support its analysts’ point, the firm refers to Bloomberg’s data, which show that Indonesian nickel ore production growth averaged 62% y-o-y over the first nine months of 2017.

The market researcher states that it also expects global refined nickel production to increase from 1.89 million tonnes in 2017 to 1.92 million tonnes in 2018. “This uptick in production will be driven by a recovery in Chinese, Russian and Australian production following a contraction for all these major producers over 2017.”

Indonesia, BMI says, will have the fastest refined nickel output growth rates from 2017-2021, increasing its total production from 43 kt in 2017 to 50 kt in 2021, amounting to average annual growth of 9.4%.

The other outperforming major producer will be Australia, which maintains a stable regulatory environment and solid project pipeline, while output in the number one global producer, the Philippines, is supposed to remain muted in the coming months as a result of environmental shutdowns of mines over 2017.

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Frutabol Colinho do Porto

Nickel prices surge after Philippines shuts down mines

Speculators rush to close bearish bets for metal used in making stainless steel