Op-Ed: Argentina’s mining promise meets reality

Argentina’s vast mineral wealth has long outpaced its mining output, and a new investment regime now faces the critical test of turning potential into production.

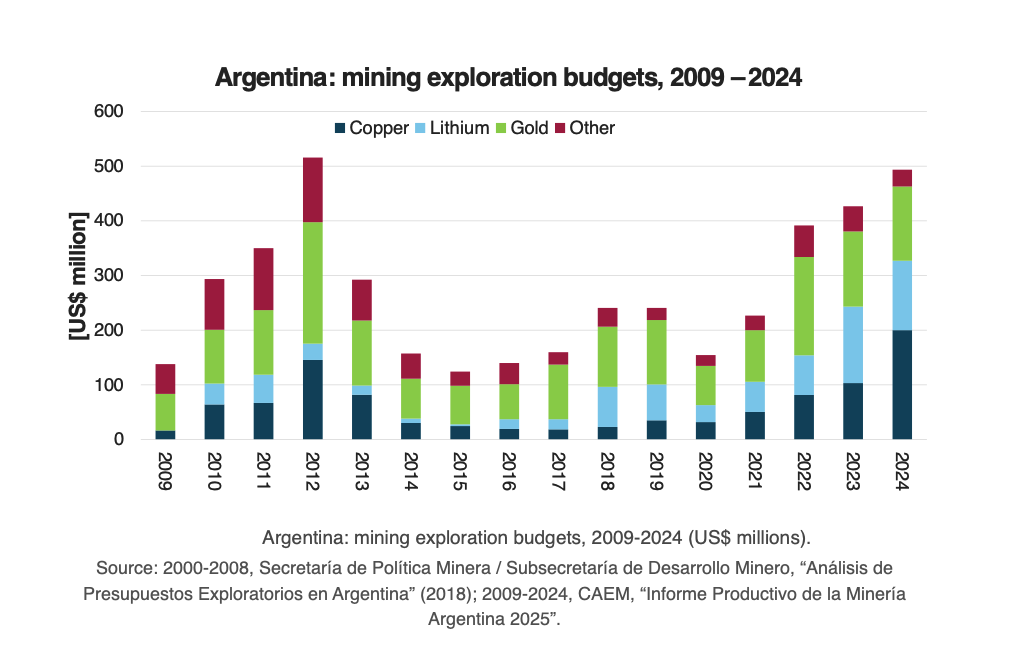

For decades, the country has attracted sustained exploration spending across copper, lithium and gold, yet that capital has failed to translate into meaningful production growth. The disconnect is starkest in copper: Argentina hosts world-class deposits but produces less than 20,000 tonnes annually, a negligible figure beside neighbouring Chile’s roughly 5.5 million tonnes. The explanation is not geological—it is structural. Regulatory instability, foreign exchange controls, import barriers and uncertainty around profit repatriation have consistently deterred long-term investment decisions.

The Milei government’s Large Investment Incentive Regime, or RIGI, is an attempt to change that equation by reducing the systemic risks that have historically delayed mining projects. “The core of RIGI is not an isolated incentive, but rather the coordinated reduction of risk faced by long-term mining projects,” said Patricio Faúndez, economics lead at GEM Mining Consulting. By offering greater fiscal stability and a more predictable currency framework, the policy aims to shrink what economists call the “option value of waiting”—the incentive for companies to postpone large, irreversible investments in uncertain environments.

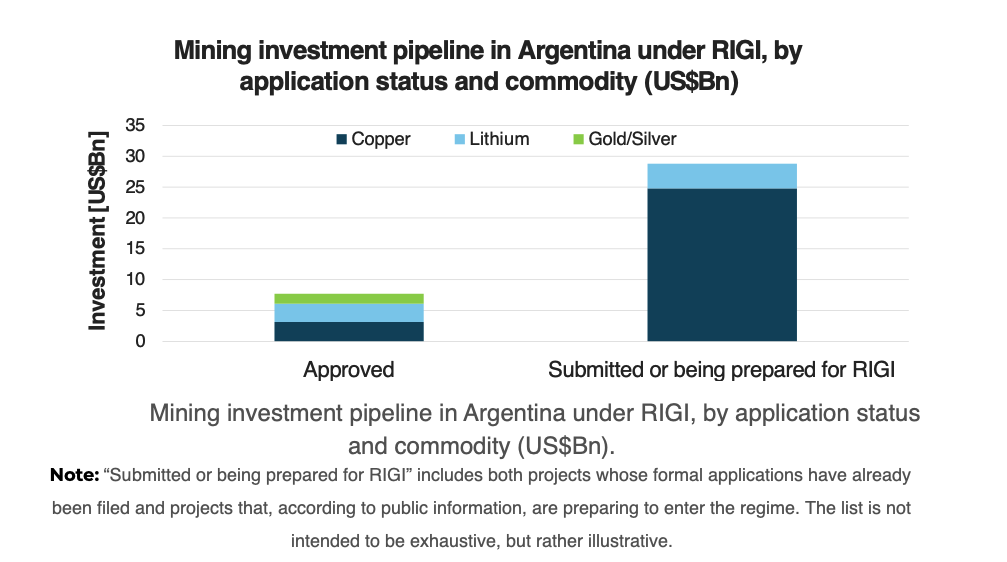

Early signs suggest the regime is gaining traction, though cautiously. Initial approvals have focused on lithium projects and brownfield expansions—developments that require less capital and shorter timelines. Roughly US$8 billion in projects have already been approved, with lithium accounting for a significant share. More telling, however, is the next wave: nearly US$30 billion in projects either submitted or being prepared for RIGI, dominated by large-scale copper assets such as Vicuña, MARA and El Pachón.

This emerging pipeline highlights both the promise and the risk of the policy. Copper projects are capital-intensive, technically complex and often take more than a decade to build. Their advancement will depend less on headline incentives and more on whether Argentina can sustain macroeconomic stability and regulatory consistency over time. In other words, RIGI’s success will not be measured by announcements, but by final investment decisions.

If even part of the current pipeline materializes, the implications would be profound. Argentina could shift from a marginal copper producer to a significant global supplier, reshaping its export profile and strengthening South America’s role in critical minerals markets at a time of rising global demand.

But that outcome is far from guaranteed. Argentina’s mining history is littered with deferred projects and missed opportunities, often derailed by the very uncertainties RIGI now seeks to address. The regime has clearly altered investor sentiment at the margin; whether it can anchor long-term confidence is the real question.

RIGI is not a silver bullet—it is a stress test.

* Patricio Faúndez is Economics Analyst Leader at GEM Consulting

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments