Top iron ore producer forecasts 50% fall in price

Iron ore was the best performing commodity in 2020, thanks to China’s early emergence from the pandemic and Beijing’s heavy spending on economic stimulus, particularly infrastructure.

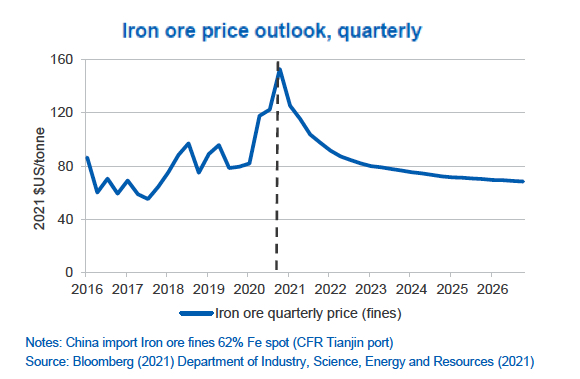

Iron ore prices have eased since hitting levels last seen in 2011 at the beginning of this month, but at $167 a tonne are still 90% higher than this time last year.

China consumes 57% of the world’s iron ore and controls more than two-thirds of the seaborne trade. Australia’s share of world trade is 53% and although relations between the two countries have soured, when it comes to iron ore they are joined at the hip.

Australia’s department of industry’s quarterly report outlines a bonanza for the country with annual iron ore export values expected to peak at A$136 billion ($103bn) in 2020–21 and stay above A$100 billion for the next five years.

The strong earnings are thanks to new mines and expansion projects coming online, which will push Australia’s iron ore exports from 900 million tonnes currently to 1.1 billion tonnes by 2025–26.

The outlook for prices, however, is far less rosy. Australia’s office of the chief economist sees a range of factors putting downward pressure on prices over the coming months.

Some price falls are expected, as Vale’s Brazilian operations steadily return to output levels prior to the January 2019 Brumadinho dam collapse. Overall, Brazilian output is expected to recover to normal levels by the end of 2021. More rapid progress on this front could lower prices more swiftly.

Chinese steel mills, which are facing severe pressure on margins, may also seek to postpone some output in order to manage price pressures over the coming months. Chinese Government stimulus measures could also be phased down in the second half of 2021, reducing the imperative for rapid purchases of iron ore to meet production schedules and allowing some build-up of iron ore at ports.

While price spikes are likely as a result of disruptions due to extreme weather in the two main supply regions of Western Australia and Brazil, the longer term outlook for the iron ore price is squarely in double digits.

Prices are expected to halve by the end of next year and then gradually decline to reach $72 a tonne in real terms by the end of 2026.

More News

South32 CEO open to M&A following Alcoa asset sale

The diversified miner agreed to sell the bulk of its aluminium portfolio.

July 01, 2026 | 02:59 am

Seeing the whole picture: Closing notes from Kazakhstan

June 30, 2026 | 04:26 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Yaw Anane

The price is damn too high for emerging markets