Barrick needs Randgold to make the grade

(Bloomberg Opinion) — Gold miners have been struggling for decades against geological destiny.

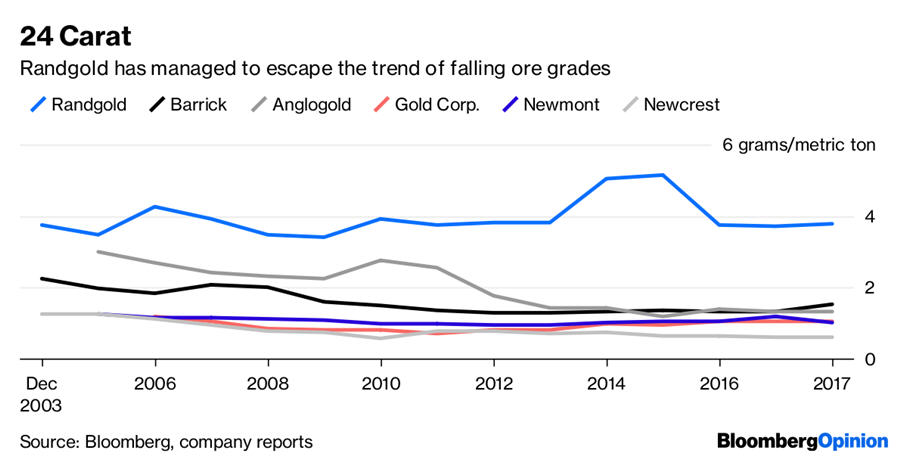

The grade of metal in the world’s gold reserves has been declining for years, from average levels above 10 grams a metric ton in the late 1960s to almost one tenth of that now. That’s a worrying metric, because few gold mines can operate profitably below 1 gram a ton – equivalent to extracting two teaspoons of gold from a Statue of Liberty’s-worth of ore.

With gold prices now hovering below $1,200 a troy ounce, that deterioration of the world’s ore quality is becoming particularly acute. From levels of 1.42 grams a ton a decade ago, the average reserve grade of the top five gold miners – Barrick Gold Corp., Newmont Mining Corp., Anglogold Ashanti Holdings Plc, Goldcorp Inc., and Newcrest Mining Ltd. – has fallen to 1.12 grams in 2017, having touched a low of 1.04 five years earlier.

In recent years, Barrick’s Executive Chairman John Thornton, who’s also a Ford Motor Co. director, has taken a carmaker’s approach to this problem: promising to slash operating costs and use data analytics to supercharge the productivity of its pits. That can only get you so far, though, because the grade of most deposits goes down as miners dig up the best bits.

With each ton of rock that’s extracted, it gets harder and harder to make money.

That’s the reason a combination with Africa-focused producer Randgold Resources Ltd. became essential. Randgold’s board has agreed to an all-share takeover in which Barrick will end up with about two-thirds of the equity in the new business, the companies said Monday. Randgold’s Chief Executive Officer Mark Bristow will become CEO under Thornton, who’ll keep his existing title.

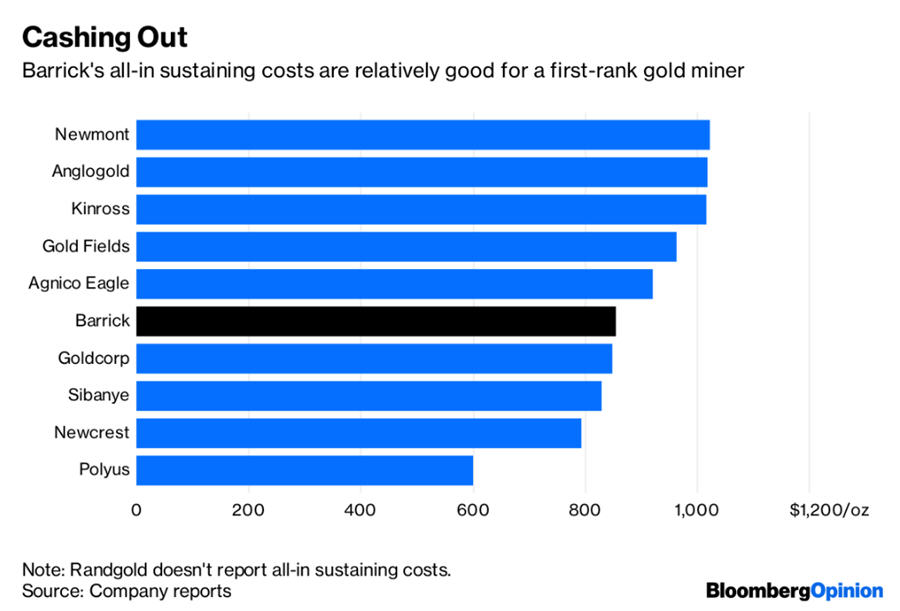

The deal is remarkable given the way Bristow has positioned himself as a gadfly in recent years. The rest of the industry has tried to standardize its financial reporting on the basis of all-in sustaining costs – a metric that’s meant to bring together production costs with head-office expenses and maintenance capital expenditure to account for the depletion of mineral reserves.

Barrick does rather well on this account, with costs of $856 an ounce in the June quarter, among the lowest of major miners. Bristow, however, has been a trenchant critic, arguing that the number has served to obfuscate true costs, rein in exploration spending and ultimately fuel the grade decline that’s damaging the entire industry.

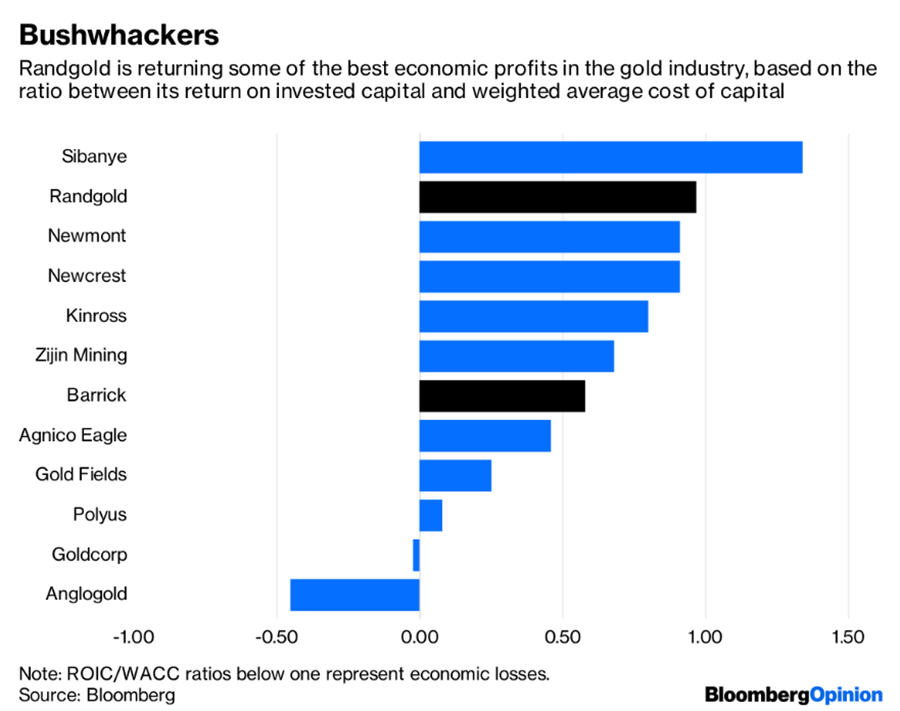

In terms of economic profit, he appears to have a point. If a miner is truly making money for its investors, its return on invested capital should be running ahead of its weighted average cost of capital. It’s extraordinarily rare, though, for companies to actually achieve this: Indeed, Randgold is one of the few miners to have regularly accomplished that feat in recent years, alongside Polyus PJSC. That being the case, it will be interesting to see how Bristow will sell his shareholders on a merger with the biggest beast in an industry he’s spent years criticizing.

One obvious justification is that Randgold’s reserves, too, are running out. At last year’s annual production rate of 1.32 million ounces, its five active pits and under-development Massawa site will be depleted in about 10 years. Mineral exploration is a crapshoot, so if Randgold’s shareholders want the best prospect of finding the next high-grade deposit, they’re better off linking themselves to Barrick’s exploration budget and revenues that are about twice the size.

There’s another issue, too. With prices for many commodities (though not gold) on the rise again, resource nationalism is rearing its head. Randgold’s biggest pits are in Mali and the Democratic Republic of Congo, which are both revising their mining codes to win more royalties from mineral wealth. Barrick’s spread of deposits – in particular its still-outstanding suite of assets in the U.S. at the Goldstrike, Cortez and Turquoise Ridge pits, as well as mines in South America and Oceania – is a good way of diversifying that particular risk, even as its own African pits have been caught up in a protracted and bitter dispute with the government.

The strongest argument, though, may be that Bristow is bringing down the system from the inside. Harnessing the best of Barrick’s pits to Randgold’s more aggressive style might be the best way to get the industry as a whole out of its rut.

“We will need to take a very critical view of our asset base and how we run our business,” Bristow said in a statement accompanying Monday’s initial announcement. The merged company would pursue “a strategy similar to the one that proved very successful at Randgold.”

From that language, the attraction of a deal to Randgold should be pretty clear. Judging by the respective shares in the new company, you’d think it was Barrick that was going to be in control. The way Bristow is talking, though, he intends to be in the driving seat.

(By David Fickling)

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments