Big funds bet billions on mining supercycle

Major fund managers are heralding a sustained rally in mining and metals as money floods into the sector at the fastest pace in years, driven by robust AI infrastructure, rising defence spending and a shift away from expensive tech stocks.

Assets under management in mining exchange-traded funds more than doubled to $87.4 billion by March 31, from $37 billion a year earlier, data compiled by research firm ETFGI for Reuters shows.

Oil & gas and agriculture have also attracted significant inflows, marking one of the sharpest rotations toward hard assets in history.

Investors put $8.24 billion into mining in the first quarter, a $10.8 billion turnaround in sentiment compared with the first three months of 2025 when sweeping US tariffs announced by President Donald Trump triggered outflows of $2.52 billion.

BlackRock portfolio manager Evy Hambro told Reuters capital is starting to rotate into hard assets from high-valuation tech stocks, calling it “the early stages of a commodity supercycle”.

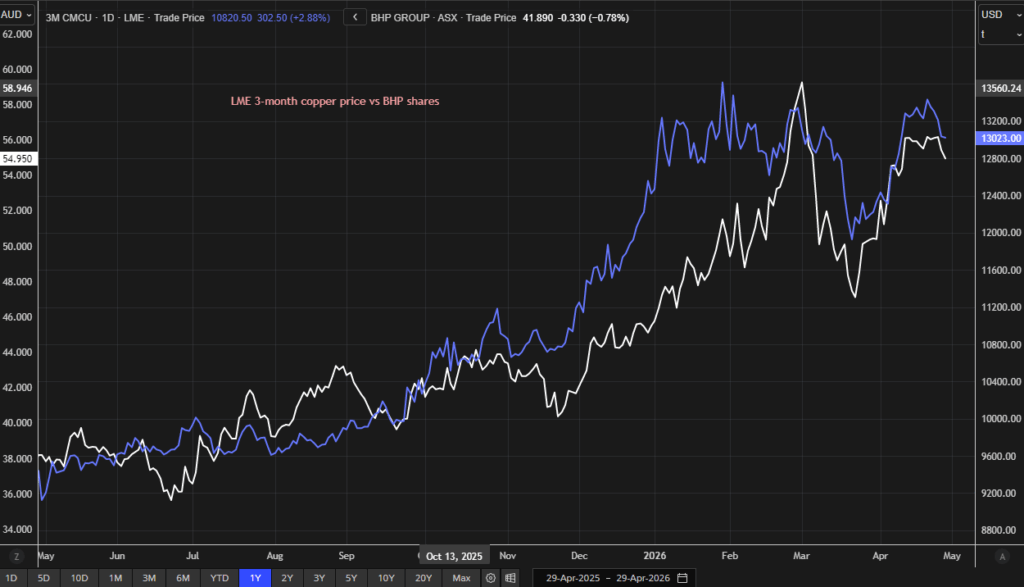

Morningstar’s US Technology Index fell 9% in the first quarter. Shares of BHP (ASX: BHP) and Rio Tinto (LON: RIO), the world’s two largest mining companies, both hit record highs this year.

“The material intensity of GDP is rising,” Hambro said, pointing to surging capital investment in grid infrastructure, data centres, electric vehicles and charging stations.

Unlike China’s urbanization-driven boom in the 2000s, Hambro said demand is “much more robust and resilient” in this cycle because there is global diversification across AI, electrification and defence.

However, the shift heightens risks of sharp price swings as metals markets are small relative to global equities and bonds and thus more vulnerable to bottlenecks in mining, refining and transport, analysts and investors said.

Fidelity’s Taosha Wang also said that a mining and energy-focused supercycle has already arrived as the Iran war pushes governments to prioritize supply security.

Industrial metals vs gold

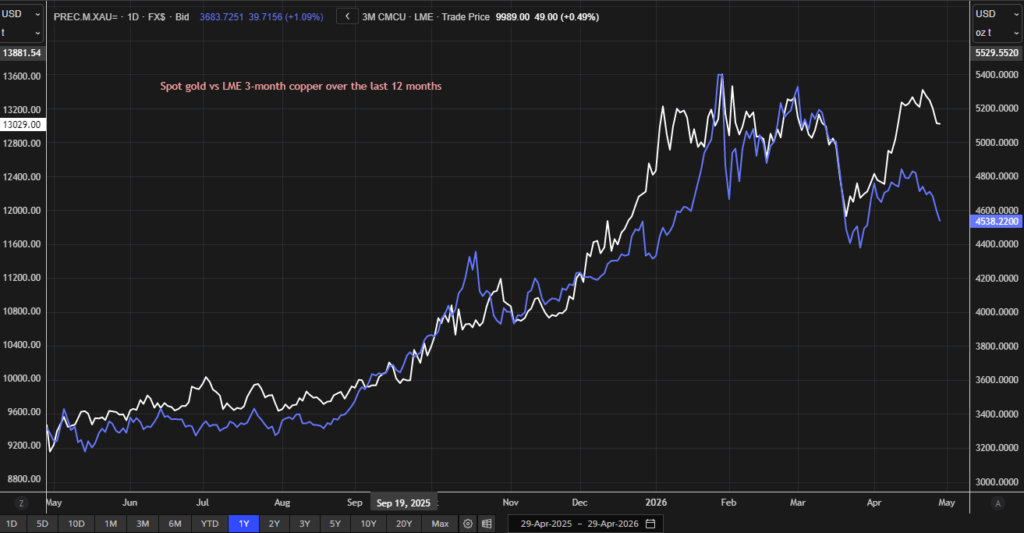

Flows have shown a tilt toward industrial metals. Copper funds attracted $198 million in March, while a searing rally in gold gave way to profit taking. The VanEck Gold Miners (GDX) ETF alone lost $710 million last month, but remains up almost $1 billion year-to-date.

The pullback in gold during an active geopolitical crisis is notable, investors say. Rather than seeking shelter in traditional safe havens, markets appear to be betting that the Iran conflict will catalyze a real-economy response, with energy security and infrastructure investment requiring copper, steel and rare earths.

Flows into oil and gas funds – of an almost net $6 billion in the first quarter according to ETFGI data – reinforce the thesis that investors are positioning for infrastructure spending, fund managers said.

Some portfolio managers see appeal in diversified miners like BHP and Rio Tinto positioned at the intersection of multiple demand drivers.

“Copper is very much in demand, aluminum very much in demand, even more so now, as the Iran crisis unfolds,” said Anix Vyas, portfolio manager at Harding Loevner, noting that Rio Tinto with holdings of both metals can benefit from a surge in demand from data centres and industrial applications.

Vyas framed the shift as investors fleeing software companies vulnerable to AI disruption for companies with more durable competitive advantages, like miners with control over critical minerals.

Small markets – big swings

The relatively small size of metals futures markets means heavy inflows can magnify volatility even as a broader uptrend remains intact.

Trading volumes for metals futures including copper and aluminum on the London Metal Exchange amounted to $21 trillion last year, while the CME put trading in gold futures at more than $25 trillion, paling against the $85 trillion racked up in Nasdaq-100 futures and more than $135 trillion in S&P 500 futures.

The sharp year-on-year swing in ETF mining flows demonstrates how quickly sentiment can shift and how vulnerable these markets are to reversal.

The sector is also only a small slice of the global stock market, with the top five mining companies representing just 0.4% of the MSCI ACWI Index versus 16.8% for the top five tech companies. Metals and mining products account for just 0.57% of total equity ETF market share.

Major mining companies’ shares still trade at 7 to 8 times EV/EBITDA, well below the 14 times multiples seen during the 2008-2010 boom, suggesting significant upside if the supercycle plays out.

“Copper is at the intersection of everything and critically undersupplied. There is no doubt in my mind that copper prices could double or triple over the next decade and owning copper producers will deliver multiples of the spot price growth,” said Charlie Aitken, group investment director at Australia’s Regal Partners, which is overweight mining and metals and held A$21 billion ($15.05 billion) under management at the end of March.

However, while investments in the sector offer an inflation hedge, they could also accelerate price gains, compounding inflation pressures from the Iran war’s impact on energy markets and posing risks to global growth, investors said.

($1 = 1.3957 Australian dollars)

(By Clara Denina, Melanie Burton, Pratima Desai and Polina Devitt; Editing by Veronica Brown and Kirsten Donovan)

More News

Bomb attack damages Ecuador mining agency probing illegal gold

It’s the second blast in recent weeks affecting Arcom offices.

June 29, 2026 | 12:28 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments