The anatomy of a mine site visit

On Wednesday January 27th, 2016, Palisade Global went on a 2-day investigative assignment to take a look under the hood of Canarc Resource Corp’s “El Compas Project” in Zacatecas, Mexico… We thought it would be enlightening to share the notes with our reader…

With the information we have/had access to on a “2-day site visit”, it is impossible for us to make a definitive determination, using quantitative analysis or otherwise, as to the integrity of the project’s resource delineation or the PEA. Our observations and opinions are our own; so take them as you wish. Please read the disclaimer at the bottom of this write-up.

We will try and put everything in laymen’s terms for the most part, when we first saw Canarc’s PEA numbers we were a little surprised… First off, it seemed too good to be true. And in our experience evaluating investment opportunities at this stage of development – this is usually the truth. But this time we were pleasantly surprised.

When we look at a project like this, there are a few important technical categories to evaluate:

The Team – Who are these guys? Can they run a mine? How much will they lean on local expertise and labour? What type of experience does the local management possess? How much would the company need to spend on training the local labour force?

The Geology – Do they have a firm grasp on the geology of the deposit? How extensive is the dataset? Is the data well organized? Are they honest and forthcoming about any gaps in their knowledge/understanding of the geology? Have they incorporated geological interpretation into domaining of resource blocks?

Resource – How much variability is there across the drill intercepts? Did they cut the exceptionally high grades (top-cut factors) if necessary? Is mineralization visually distinguishable and discrete (this is important for grade/dilution control when mining and modeling)? Sample sizes – did they target specific geological features or just blindly sample at meter wide intervals? QA/QC – were regular blanks/standards/duplicates sent interstitially to check for lab integrity? Does the drill spacing make sense compared with the variability from hole-to-hole? Would the geological modeling change significantly if spacing was tighter?

Mining Method – What is the geometry of the deposit? Does the proposed mining method seem realistic for the general orientation of the deposit and its width continuity? What are the tonnage expectations? Will the proposed mining method and developed mine infrastructure suit that or is it unrealistic? How susceptible would the resource be to dilution? Is this dilution adequately represented in the cash flow model? How much variance could they expect/ how much could they tolerate? How easily can they control grade and dilution? And most importantly… How ambitious is the mine plan – does is it feature a lot of moving parts? Or is it relatively straightforward?…

Without getting into too much of the details – We will move onto talking about our trip.

Following a direct flight from Toronto to Mexico City, we hopped on a quick 1 hour and 20 minute flight to Zacatecas where from our airplane window we could see a serene countryside of rolling hills covered in scrub and cacti, accentuated by headframes and couple of spewing smoke stacks, in short… our kind of place! The airport was excellent with international flights to LA and Chicago preparing to depart. The inner miner entrepreneur in us was screaming out “good, we can get spare parts easily in this place.”

Through the winding and confusing streets of Zacatecas, we drove past a couple of Walmarts, McDonalds’, Starbucks and some of the most amazing architecture we’ve ever seen. We were told all of this beauty came from centuries of silver-gold-lead-zinc mining. On the highway there were signs for Fresnillo and Durango – we quickly realized the scale and prolific epithermal nature of the area code.

We had the pleasure of sharing the backseat (literally, not figuratively) with very pleasant and funny Metallurgist named Garry Biles (President & COO), he was a Newfie (who doesn’t like Newies’s!?). Gary had a wealth of experience in Mexico among other Latin American countries, with 25+ years of Mining and Mill management experience; he was the guy in the operational steering wheel.

We picked his brain on all aspects of the mining and milling/processing, local staffing potential, and the geopolitical landscape. With a level head, and a calm upbeat personality, we noticed this guy was the real deal, ready to handle the stress and rigors of mine management. He even joked how he was itching to deal with the day-to-day breakdowns and the frustrating language barriers that are part and parcel of mine management in foreign jurisdictions. His passion for all of it was clear – and that was all we needed to know!

We soon arrived at headquarters, a rented house in the middle of town, where we met the rest of the team. The office was clean and organized, outfitted with PCs, light tables, map cabinets, a projector and all things good and holy that make for a proper geology office. At the table was the recently hired Country Manager and local face of the company, Alfonso Canseco, or as he insisted we call him, “Poncho”. He had 30+ years of Mine Management experience in Zacatecas, working faithfully for a couple of the biggest mines in the region. His English was poor, but he looked like a pretty confident, laid back and serious hombre. This was a key hire for Canarc according to Gary – he has a huge network of technical and skilled labour connections that have worked for him in the area for a long time. Having run a couple of mines ourselves, having these connections is essential because of the synergistic operational efficiency that it brings to a project from Day 1. Although we did not speak the same language, we had a very good feeling about Señor Poncho.

Enter Jose Luis Garcia, the resident Geologist with a silver tooth and burning passion for exploration and spicy food. Boasting over 10 years of experience at El Compas and in surrounding areas, he confidently walked us through all aspects of the project’s regional and local geology. We looked at sections, drilling, mineralization controls (macro and micro) and additional zones with mineralized potential. Our focus here was to judge the prospects for expanding the project’s current 150K ounce resource. With solid structural, geochemical and surface sampling, Jose Luis showed us another four zones on the property with fingerprints matching El Compas’ that warrant further investigation.

Based on our observations, we will say there is a very strong chance they can double the resource on other pods in the area. Some signs point to a potential Ag-Pb zone at depth, but we would say evidence for that was a little shaky. It is tough to establish what there is until more drilling is conducted – for all we know, there could be 1M oz. somewhere on or around the property. Surrounding claims held by other local prospectors and companies also exhibit strong potential with encouraging surface sample numbers, etc.

With an operating mine, Canarc would be poised to engage in accretive negotiations where “no doubt” they could add ounces and likely find another El Compas nearby. We were very impressed with Jose Luis’ abilities as a geologist/geotechnician. He loves the project, is excited to talk about it, and frankly that is all an investor could want. Passion baby passion!

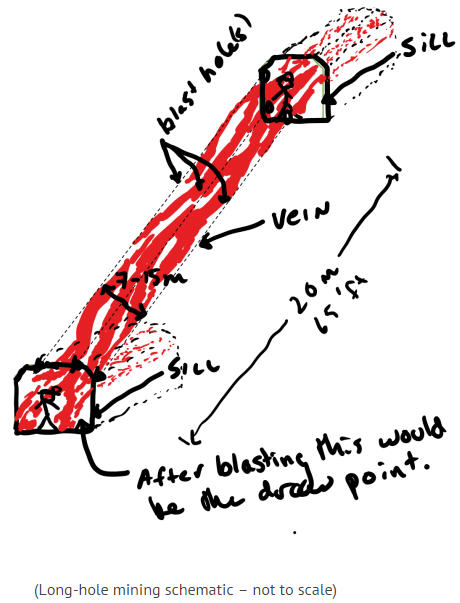

Not sparing any detail, Jose Luis and Gary walked us through the resource and the PEA for the project, highlighting the annual stoping schedule as compared to the overall resource model. Positively, the orebody appears quite continuous, ranging from 7-15 meters thick dipping on average 60-70°. We are talking some serious crustiform epithermal veining here with sharp contacts and very little host rock mineralization outside of the veins.

Because they are planning to long-hole mine these wide veins with 20 meter sills (~65’), these will be some very large holes. At first blush, the steep discrete nature of the veining should make dilution and overbreak quite controllable, running at 500 tonnes/day (tpd). We had questions about drilling such long blast hole rings through 15 meters, thick Qtz±Crb veins, We would imagine those could have a tendency to wander, Gary assured me that the local miners do that all the time. We could now picture the never ending upside down pezz dispenser that will be their panel draw points, hence the absurdly low tonnage costs (high volume blasting low volume mucking and milling at 4-5 gpt).

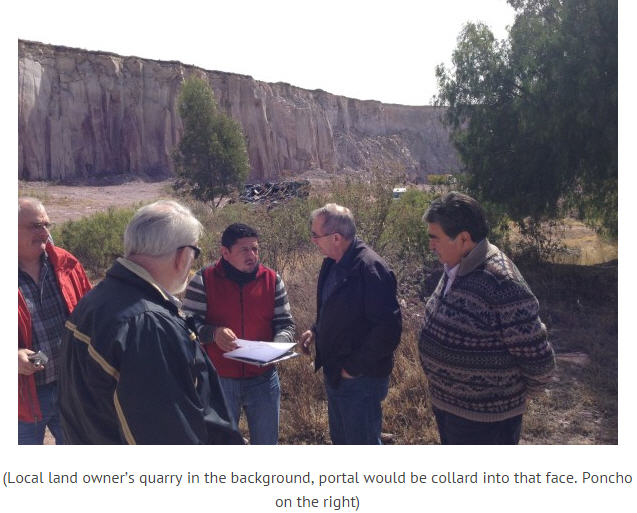

We proceeded to the El Compas site, which took about 15 minutes from downtown. We thought it was pretty strange for the project to be so close to town, just a kilometer or two from housing developments. For those questioning why Canarc is not open-pitting this project – voila, this is your answer. Standing on top of the hill, Jose Luis and Gary identified the orientation of the mineralization to put everything in perspective for us. A local rhyolite quarry had done a good job stripping a 10 to 15 meters sheer face on which the portal for the decline would be collared. The quarry was still being worked while we were there, about 300 meters or so from the proposed portal site.

Scattered throughout the hillside, Jose Luis pointed out numerous veins and shafts from historic activities and mapping, or as he says “beins and chaffs”. We inspected a few holes laid out in the sun – good thing we brought the trusty hand lens along. The core was nice and competent, mineralized vein zones were obvious; with little to no wall rock numbers outside of the veining, grade control should be a breeze!

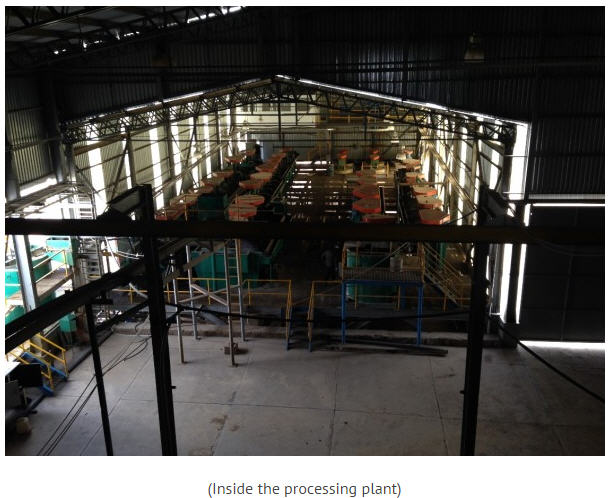

Catalin Chiloflischi, Canarc’s CEO, was busy all day speaking with the government and finalizing an agreement for the Plant. In the field, Gary received a call saying it was officially finalized – they had signed a binding agreement for the Plant. Gary was pretty proud of his colleague! He mentioned how much work Catalin had put forth to get this done over the past year. With a sigh of relief and a huge Newfie smirk, Gary and the rest of us skipped off to the mill site to meet Catalin and have a walk around. Having the mill in hand is really a key component of this project – without it, the project would be pretty lackluster. It’s pretty difficult to validate a 500 tpd mill construction with a 150Koz deposit. Hence why most if not all of us have ever heard about Canarc resources or El Compas until now.

When we got to the Mill site, we were very pleasantly surprised. The site was secured with a fence and a guard post, and featured an office building, lab building and an incredible amount of infrastructure. Massive buildings were outfitted with what appeared to be relatively newish gear: cone crushers, conveyors, ball mills, flotation cells, thickener tanks, about US$60,000 worth of HDPE piping and a pretty new looking Cat loader with a flat tire. All of it was just there – the odd part, or perhaps not so odd, was that the entire operation was gutted of wiring. There was not a strand of copper in the whole place. In most cases, motors were all intact and appeared fine, just the wiring was missing.

The tailings infrastructure was also newly constructed. It sat nearly completely empty – massive but empty! Overall, we would guess someone must have spent a small fortune on this entire plant + tailings infrastructure/ everything. We soon learned that this facility had been intended to serve as a government owned toll mining operation; however, as it turned out, it was built for war, but never saw battle. The government turned it off because they did not have the feed.

The contract that Catalin negotiated with the government provides Canarc full access to the fully permitted turnkey site, at no cost, for the first 6 months; thereafter, the company will have to pay the government a fee of US$7,000 per month and allowing 50-100 tpd capacity for toll milling. Canarc will have to spend approximately a US$1 million to bring the mill back into working order. Catalin appears to have covered all of its bases – local contractors have delivered multiple quotes pertaining to hauling, mining, mill restoration, and wiring, all in writing.

That night we had a great time with an excellent meal, a few shots of tequila to wash it all down, while discussing financing options and variations on capex requirements. One option that was discussed was proceeding with a potential US$5.5M capex without a cyanidation circuit (i.e. simply using flotation and producing a concentrate). Another scenario that we mulled over was spending an extra US$1.5 million to complete a circuit that would produce a saleable dore. The verdict on that has not yet been reached – it will depend on additional metallurgical testing and optimization research.

The next day, we were present alongside government ministers and the Governor of Zacatecas for the unveiling of Santa Cruz Silver Mining’s new operation in the area. Our table at the event was directly adjacent to the table for the Ministers – there were speeches, local television crews, and mariachi jams! During his speech, the governor acknowledged the agreement they entered with Catalin, offering thanks to the company and encouraging success for Canarc in the near future. It was nice to observe the strong working relationship between the Canarc and the regional government.

In summary, Catalin has done great job along with Gary, Poncho, and the whole team to make something promising out of this little El Compas asset. Our takeaway was recognising a genuine team with a genuine asset in a beautiful safe and welcoming Mexican mining jurisdiction. Assuming fully financed with a NPV of US$32 million after tax and a current market cap US$12 million US, we could see CCM trading at 1.1X net asset value like some of the comps out there; meaning Canarc has the potential to nicely award its investors.

Palisade Global Investments Limited holds shares of Canarc Resources. The information contained in such write-ups is not intended as individual investment advice and is not designed to meet your personal financial situation. Information contained in this report is obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The opinions expressed in this report are those of Palisade Global Investments and are subject to change without notice. The information in this report may become outdated and there is no obligation to update any such information.

More News

Northern Star replaces CEO, activist investor Elliott wants more

July 01, 2026 | 08:29 pm

Ukraine urges swift publication of Irish investigation into alumina exports

July 01, 2026 | 01:22 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments