Column: Copper price slump brings Chinese buyers out in force

While the rest of the world worries about recession, China is steadily increasing its imports of physical copper.

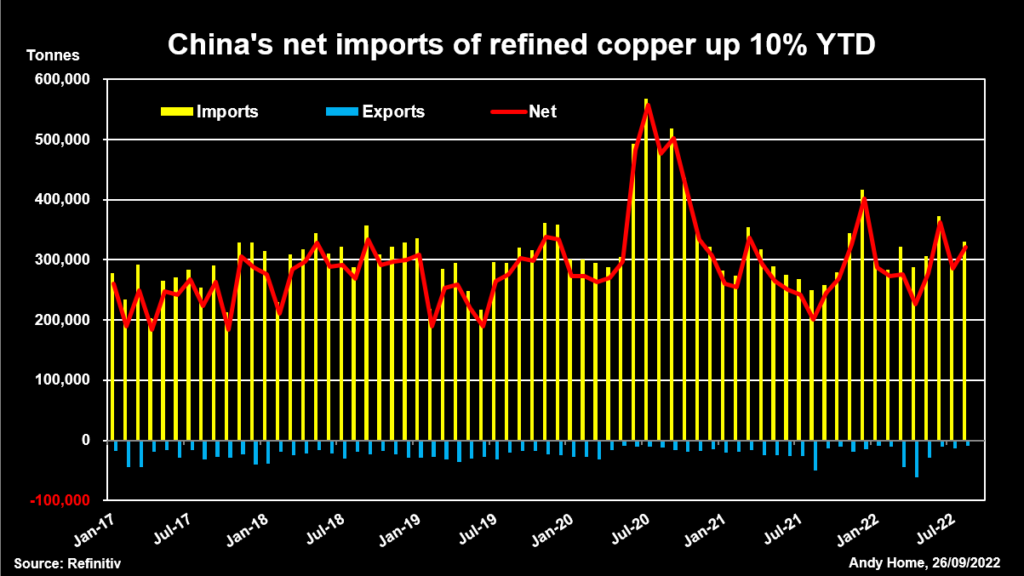

The country’s net call on refined copper from the rest of the world was up by 9.8% in the first eight months of the year. Year-to-date volumes are the strongest since 2020, when China imported a record amount of metal.

China is simultaneously lifting imports of both copper scrap and mined concentrates, suggesting the hunger for refined units is not down to a shortage of raw materials.

Strong import flows defy both the broader gloom around China’s debt-laden property sector and the more specific problems at trading house Maike, which is one of China’s dominant copper import channels.

It’s clear a major restocking exercise is underway, but is there something else at work as well?

Buying spree

China’s net imports of refined copper were 2.31 million tonnes in the first eight months of this year, a 200,000-tonne increase on the same period of 2021.

However, that understates the scale of the buying spree that is currently taking place. Imports were running below year-earlier levels as recently as May. The pace accelerated sharply in June and has been running at an annualised 3.87 million tonnes over the last three reported months.

Annual imports have only exceeded that level in 2020, a year when the LME copper price plunged to below $5,000 per tonne as covid-19 chilled manufacturing activity first in China and then everywhere else.

Chinese buyers today are similarly capitalising on copper’s precipitous slide from over $10,000 per tonne in March to a current $7,425.

This is in many ways a natural turn of the stocking cycle.

Copper doubled in price between 2020 and 2021, causing such financial pain for smaller buyers that Beijing released around 110,000 tonnes of metal from the state stockpile.

If the government was forced to destock by extreme prices, it’s a fair bet that the entire domestic supply chain was doing the same.

Scrap and concentrates imports up

The restocking momentum is also travelling down copper raw materials import channels.

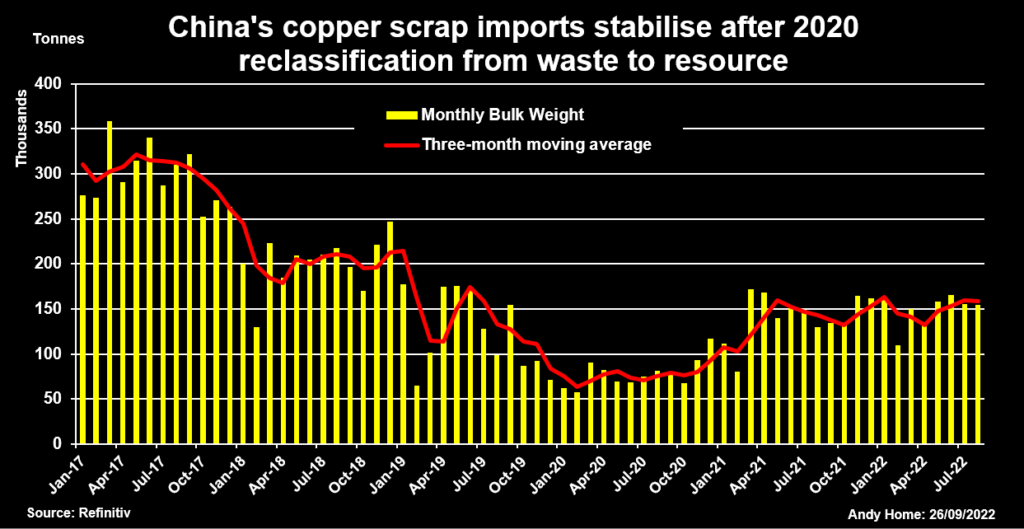

Year-to-date imports of copper scrap are up 8.2% on last year, building on the surge that followed its 2020 removal from the list of banned waste imports.

Import volumes of 1.19 million tonnes through August look small by comparison with previous years but what’s now entering China is much higher-purity material as required by the regulatory reclassification from “waste” to “resource”.

The United States has returned to top-supplier position, shipping 214,000 tonnes of copper recyclables to China so far this year, up 48% on 2021 rates.

It’s worth remembering that some of this material will flow straight to fabricators for direct melt into their products. Higher scrap flows should logically mean less requirement for pure refined metal.

Not right now though.

Similarly, robust import flows of mined concentrates – up 9.1% year-on-year through August – have allowed Chinese smelters to lift production by 2.6% so far this year.

That hasn’t diminished the call on metal from the rest of the world either.

Green demand driver

China’s copper import hunger appears unsated.

Higher imports over June-August have made zero impact on Shanghai Futures Exchange stocks, which remain extremely low at 36,897 tonnes. The Shanghai futures curve is accordingly in backwardation through June 2023.

The Yangshan copper premium, a closely-watched signal of import demand, is currently assessed by Shanghai Metal Market at $98.0 per tonne over LME cash, up from a March trough of $6.50 per tonne.

All of which begs the question as to whether the current import surge is more than just a restocking impulse.

A partial answer seems to be that while China’s old economy is foundering, its new economy is picking up the slack in terms of copper usage.

Headline manufacturing indices indicate that China’s factory activity has been contracting due to rolling lockdowns and weakness in the residential property sector.

Construction has been one of the mainstays of Chinese economic growth in recent years and it’s an important copper demand driver, particularly in the latter stages of project development when wiring and white goods are installed.

It’s impossible for copper to escape the weakness emanating from the property sector but the new economy, in the form of electric vehicles and grid spending, is providing a powerful offset.

Sales of new energy vehicles doubled year-on-year in August and are generating a broader recovery in automotive output in China.

Grid spending, which languished over the second half of the last decade, is re-accelerating, rising 11% year-on-year in the first eight months of 2022, according to Citi. (“China grid spending has another strong month”, Sept. 23, 2022)

Analysts at Goldman Sachs estimate such new green demand is fully making up for reduced offtake from old economy drivers such as property. (“Copper: Tightening into a slowdown”, Aug. 22, 2022)

Beijing is targeting 25% electric vehicle penetration by 2025 and has pledged to double grid spending over the coming 5-year period.

The sign-posting of more government investment in decarbonisation is a major reason for China’s copper buyers to feel confident about restocking physical units at current price levels.

Copper’s usage in energy transition, a future promise for the rest of the world, is taking tangible shape in China.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by David Evans)

More News

BHP seeks to restart Cerro Colorado mine with $1.5B investment

The copper mine has been closed since late 2023 after it was denied its water permit.

July 02, 2026 | 10:43 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments