Column: Gulf aluminum disruption ripples up to alumina market

(The opinions expressed here are those of Andy Home, a columnist for Reuters.)

The Iran war has focused the aluminum market on what is not coming out of the Strait of Hormuz. But there is an equally significant problem: what is not going in.

Gulf aluminum smelters are highly dependent on imports of alumina, the intermediate product between bauxite and metal, to maintain operations.

The region has six smelters but only two alumina refineries. One of them, Emirates Global Aluminium’s (EGA) Al Taweelah plant, has been damaged by Iranian missiles. The smelter at the site is out of action for the same reason and other smelters are running at reduced capacity.

The first-round impact of this disruption is further price pressure on an already soggy alumina market as shipments are redirected away from the Gulf.

The second-round effect could be further cuts in Gulf metal production as smelters run low on raw-material stocks.

The only winner here is China, which is soaking up the displaced alumina.

Under pressure

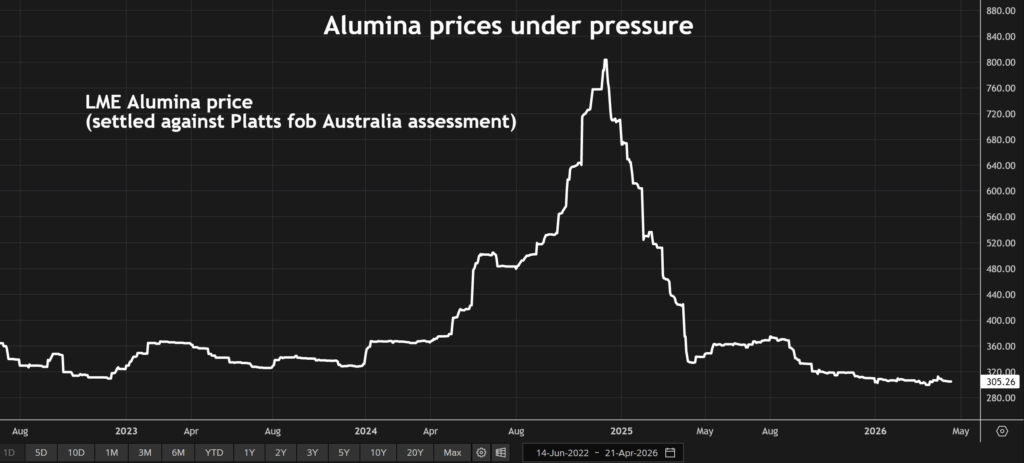

The alumina market was under pressure even before the outbreak of the Iran war.

The London Metal Exchange (LME) price , which settles against S&P Global Platts’ assessment of the Australian fob price, has been hovering around the $300 per metric ton level since the start of the year.

That is a far cry from the frenzied rally of 2024, when prices surged to above $800 on a series of supply hits.

The market has since shifted to oversupply, thanks to continued expansion of production capacity in China and Indonesia.

Macquarie Bank assessed the global surplus at 2.54 million tons last year and in December was forecasting another surplus of 1.26 million tons in 2026.

The bank has just upped its 2026 oversupply estimate to 2.2 million tons as Gulf-bound shipments are redirected into the seaborne market.

How long the Strait remains closed to shipping will determine everything.

Input risks

The longer it takes the Strait to reopen, the greater the risk of further smelter cuts to those already announced by Qatar producer Qatalum, and Aluminium Bahrain.

The only fully integrated Gulf producer is Saudi Arabia’s Ma’aden, which operates its own bauxite mine feeding the Ras Al Khair alumina refinery.

Ma’aden produces more alumina than its smelter consumes and has been arranging emergency supplies to others, according to consultancy Wood Mackenzie.

Alumina is not the only headache for Gulf operators.

Coal tar pitch, which is used to manufacture the carbon anodes used in the smelting process, could be an even bigger logistical problem, according to AZ Global Consulting.

While other carbon inputs such as calcined coke and petroleum coke can be “diverted, stockpiled, re-bagged, trucked, or re-routed with relative flexibility … liquid pitch requires heated storage, heated silos, and heated trucks to keep it molten from loading point to discharge point,” it said.

Such facilities are not widely available and not easily improvised. “Pitch may prove to be the hardest logistics problem in the carbon chain if disruption continues,” AZ Global said.

China wins

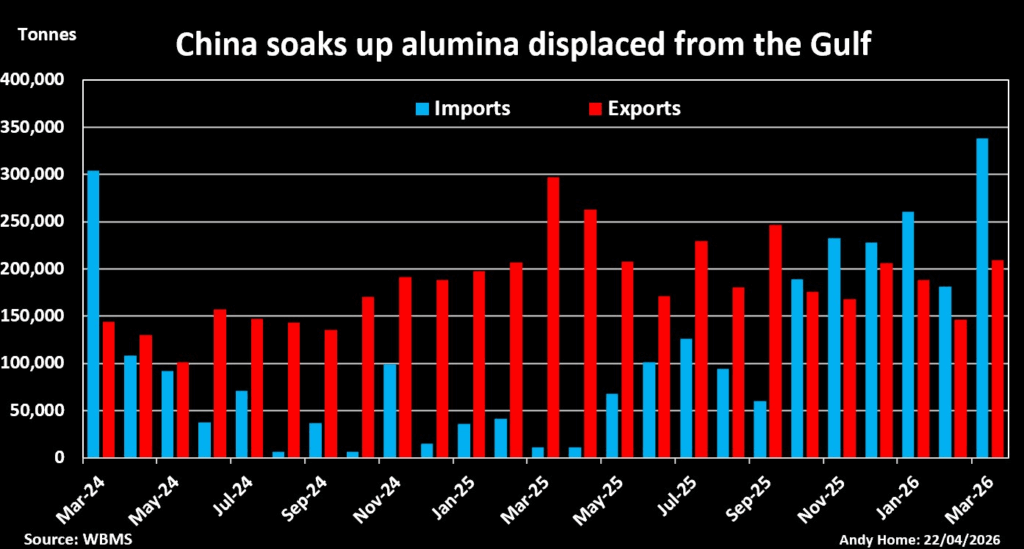

China is the prime beneficiary of the disruption in the alumina segment of the processing chain.

It imported 338,315 tons of alumina in March, the largest monthly tally since January 2024, according to the World Bureau of Metal Statistics, which collects data from official customs figures.

AZ Global expects imports to remain robust in the months ahead on the back of an open import arbitrage between domestic and international prices.

With the Gulf crisis also sending aluminum prices to four-year highs, China’s smelters are enjoying strong margins.

Western production fell by an annualized 312,000 tons in March due to curtailments in the Gulf, while Chinese production rose by 88,000 tons, according to the International Aluminium Institute.

China’s share of global production inched up to a record 60.2% last month, and that ratio is likely to carry on creeping higher as the Iran war takes a growing toll on Gulf smelters.

(Editing by Marguerita Choy)

More News

Bomb attack damages Ecuador mining agency probing illegal gold

It’s the second blast in recent weeks affecting Arcom offices.

June 29, 2026 | 12:28 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments