Column: Iron ore shrugs off China covid woes, focuses on stimulus

The iron ore market is choosing to focus on China’s efforts to stimulate its property sector, rather than on rising concerns over the potential economic fallout from surging covid-19 cases and public anger at efforts to contain outbreaks.

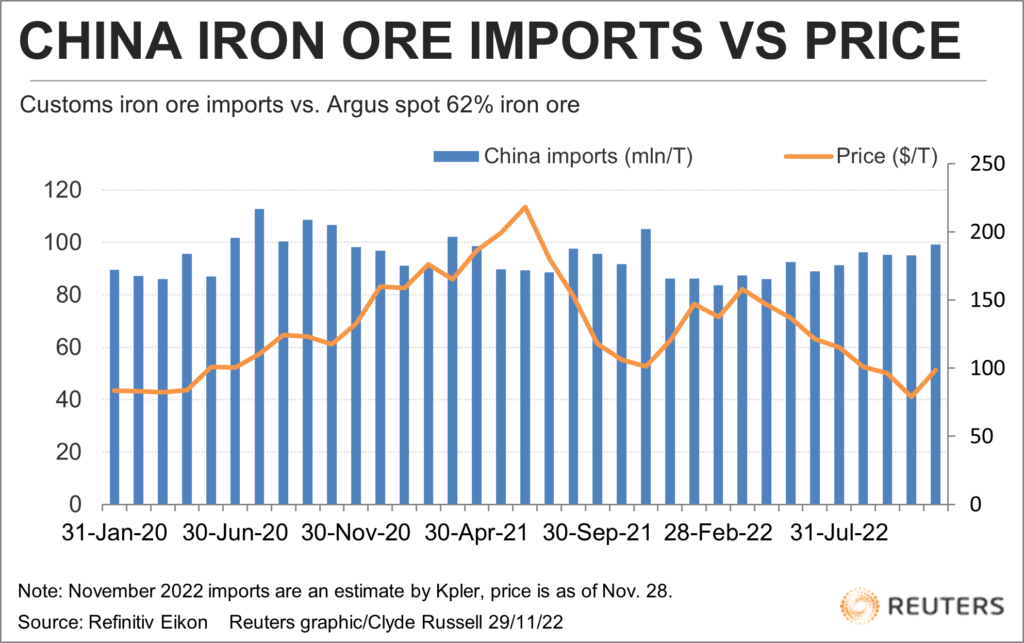

The spot price of benchmark 62% iron ore for delivery to north China, as assessed by commodity price reporting agency Argus, dipped slightly on Monday to end at $98.60 a tonne from the previous close of $99.25.

The small drop was matched by December iron ore futures traded in Singapore, which dropped to $98.14 a tonne from the close of $99.15 on Nov. 25.

However, iron ore contracts traded on the Dalian Commodity Exchange ended at 753.50 yuan ($104.65) a tonne on Monday, a gain of 2% from the close on Nov. 25.

The small drop for the international prices of spot iron ore and the modest gain for the main Chinese domestic price perhaps indicate the different perceptions held by traders in those markets.

International traders may be slightly more concerned by Beijing’s ongoing adherence to strict zero-covid measures than China’s domestic investors.

But the overall message from the price action is that, for now at least, the rising COVID-19 cases and the rare street protests against the authorities’ adherence to its zero-covid strategy are insufficient reason to alter an otherwise positive outlook for iron ore.

Demonstrations against Beijing’s covid-19 policies took place at the weekend in several cities, with analysts saying they were the biggest since the Tiananmen Square protests in 1989, which were violently crushed by the authorities.

The impact of any ongoing protests may become more important if they continue and escalate, or if they lead to either even stricter measures against covid-19, or an easing of restrictions in a bid to appease public opinion.

Outside of the covid-19 uncertainties, the picture looks brighter for iron ore, as China, the biggest buyer of the steel raw material, appears determined to revive its ailing property sector.

China’s biggest commercial banks pledged at least $162 billion in new credit to property developers last week, the latest in a series of steps taken to restore confidence in the housing sector.

The question for the market is whether the efforts to stimulate the housing construction and infrastructure sectors will be enough to boost steel demand, or whether a slowing global economy will cut demand from areas such as manufacturing.

Bullish signals

There are some other positive signals for iron ore, with China’s port inventories below levels prevailing at the same time last year, even though they have been rising in recent weeks.

Stockpiles were 138 million tonnes in the seven days to Nov. 25, up from 135.45 million the prior week, but below the 150.9 million in the same week last year.

Iron ore inventories typically rise in the northern winter as steel mills build up stocks ahead of the peak steel demand period in the spring.

Iron ore inventories peaked at 160.95 million tonnes in February this year, suggesting there is scope for them to continue building in the coming months.

Certainly, China’s iron ore imports appear headed for a relatively strong outcome in November, with Refinitiv estimating seaborne arrivals at 106.8 million tonnes, while commodity analysts Kpler are expecting a lower, but still strong, 99.13 million tonnes.

The official customs data for October had iron ore imports at 94.98 million tonnes, so it’s likely that November’s outcome will be stronger.

The vessel-tracking data and customs numbers don’t align perfectly because of difference as to when cargoes are assessed as having been landed and cleared, but the tracking data does provide useful information about the likely direction of imports.

Spot iron ore prices have spent much of the year veering between hope that China’s stimulus efforts will be successful, and the reality that they haven’t as yet.

This dynamic is ongoing. But, while stimulus efforts are accelerating in size and scope, the market also remains at risk from the covid-19 situation.

(The opinions expressed here are those of the author, Clyde Russell, a columnist for Reuters.)

(Editing by Simon Cameron-Moore)

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments