Electric vehicle outlook is even brighter if the world bikes and takes the bus

Last week, my team at BloombergNEF published our big annual Electric Vehicle Outlook. The report looks at how all the different segments of road transport could evolve over the coming decades and maps out the impact on oil markets, electricity demand, batteries, metals and materials, charging infrastructure and emissions.

There’s a lot of different angles within a big report like this. Here’s what I’d highlight among the many interesting storylines:

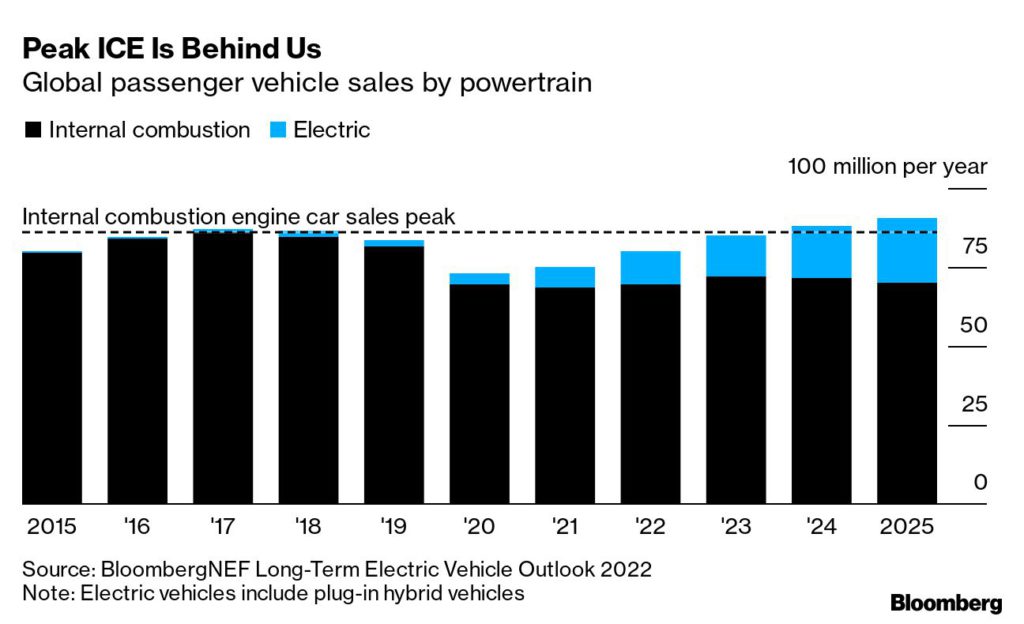

Combustion vehicle sales have peaked and are now in terminal decline.

Automotive sales are still recovering from the combination of Covid-19, semiconductor shortages and a host of other factors. The overall market should pick up in the next few years, but EV sales are rising fast enough now to keep combustion vehicles from returning to their previous peak.

By 2025, BNEF estimates sales of internal combustion passenger vehicles will be 19% below their 2017 peak. While the transition still isn’t happening fast enough for road transport to reach net zero by 2050, this is still a remarkable development after over 100 years of growth for the internal combustion engine. My colleague Nat Bullard wrote more about this here.

Electrification has now spread to all segments of road transport.

There are fascinating e-mobility case studies in both wealthy and emerging economies. China, for example, has 685,000 electric buses on the road and 195 million electric two-wheelers. In South Korea, 17% of light commercial vehicles sales were electric last year. In India, almost 40% of the three-wheeler fleet is already electric.

Each country has a very different mix of mobility needs, and very different starting points in their vehicle fleet. But if something moves and it travels on a road, somebody is now working on trying to electrify it. There will likely be more surprising successful case studies in the years ahead.

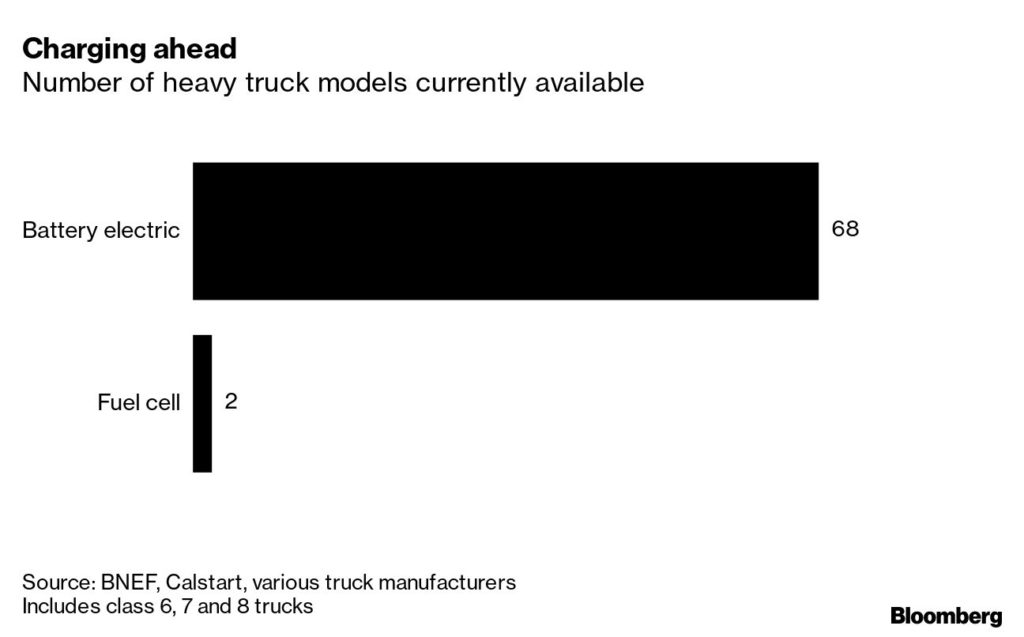

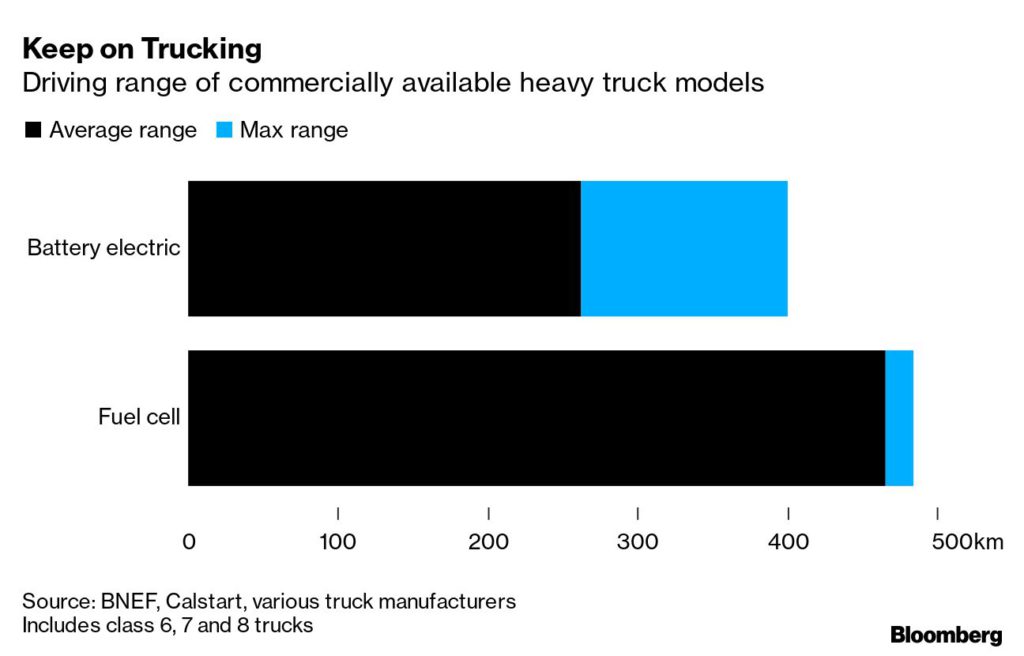

The battle between hydrogen fuel cells and batteries in heavy trucks is heating up. Or is it?

Ten years ago, there were lively debates over whether batteries or fuel cells would power the next generation of passenger cars. That’s largely been settled now, with about 20 million passenger EVs on the road and fewer than 50,000 fuel cell ones. Even Toyota, an ardent supporter of hydrogen, has been coming up well short of its relatively modest target to sell 30,000 fuel cell vehicles annually by now, moving just 5,930 of them in 2021.

The discussion has now shifted to heavy trucks, where fuel cells could still play a role. But the data there suggests a similar outcome may be in the cards. A global tally in this year’s outlook report found 68 electric heavy trucks available today and just two fuel cell models.

It’s still early days, and decarbonizing long-haul trucking will be particularly difficult. But there are plenty of miles driven by heavy trucks in shorter duty cycles, or on routes where volume, not weight, is the limiting factor. There’s also ongoing work to further “truckify” lithium-ion batteries, fine-tuning their chemistry to reflect truck usage cycles instead of just using the same cells put into passenger cars. Many fleet operators are eager to make the switch soon, so having real models on the market now is a major advantage.

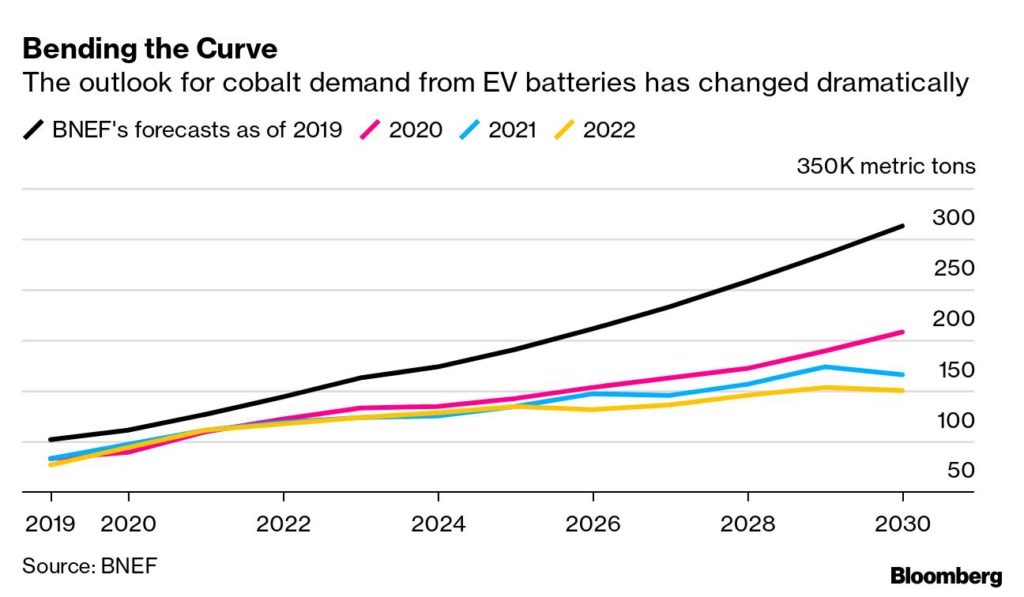

Expected cobalt demand from EVs is dropping.

The story of cobalt in EV batteries is fascinating. Most of the high-density lithium-ion batteries going in EVs are in the nickel manganese cobalt family, or NMC, with different numbers denoting different ratios of these three ingredients in the cathode (for example, NMC 622 or NMC 811). Demand for cobalt looked ready to rocket a few years ago — this appeared to be the preferred chemistry as EVs scaled up.

Cobalt demand is still set to rise, but by much less than previously expected. High cobalt prices and supply chain concerns accelerated the switch to different chemistries, including lithium iron phosphate, or LFP, which uses no cobalt or nickel. BNEF now expects LFP batteries to account for 42% of all EV battery demand next year.

This highlights an essential feature of how markets work: high prices not only drive investment in new supply, but also induce demand-side substitution. Large amounts of new investment are needed in all areas of the battery supply chain, but there are good reasons to be skeptical about warnings of endless shortages. Battery raw materials will likely go through the same cyclical fluctuations as commodity markets in the long term. The cure for high prices is still high prices.

Net zero requires more than just a drivetrain switch.

Just swapping out the drivetrain isn’t the most efficient way to reach carbon neutrality by 2050. This year’s outlook report includes a reduced demand scenario looking at how governments can combat car dependency.

Even a modest 10% reduction in miles traveled via car globally by 2050 yields major benefits and makes the journey to net zero much easier. This can be accomplished with modal shifts, primarily to active transport (cycling and walking) and public transport.

In this scenario, the global car fleet drops by 145 million cars in 2050, reducing cumulative CO2 emissions by 2.25 gigatons and cutting annual battery demand by 433 gigawatt hours, reducing strain on supply chains. An all-the-above approach is needed to get on track for net zero.

(By Colin McKerracher)

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments