Five themes to watch for European miners after humbling year

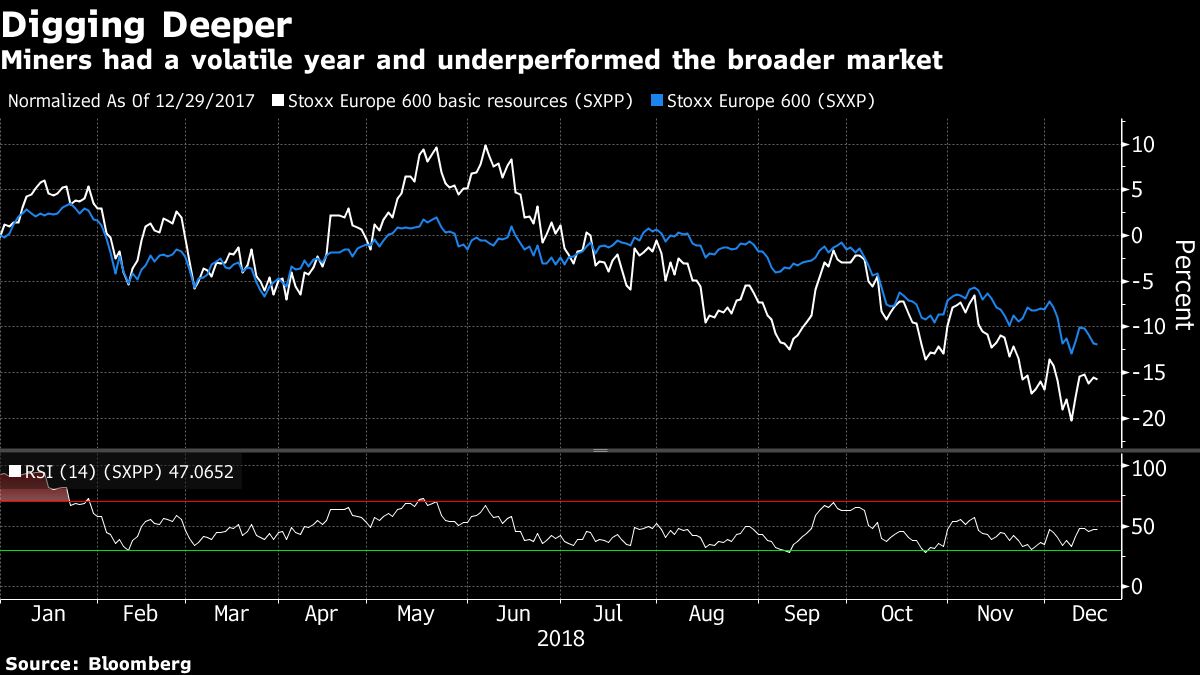

It all started so well in 2018 for investors in European metal and mining stocks, as copper led a base-metals rally to multi-year highs in a time before trade turmoil gripped markets. But, as the year closes, the sector index is languishing about 25 percent below its June peak.

Fractious rhetoric between Washington and Beijing over tariffs, plus growing worries about the state of China’s economy undid the good work of the first half. And there are plenty of signs that these worries will remain top of mind for traders in 2019.

While a slump of 16 percent this year means the Stoxx 600 Basic Resources Index isn’t among Europe’s worst-performing sectors, the SXPP is now trading at the cheapest valuations since 2012 and the highest dividend yield since 2016.

As investors ponder whether those numbers signal that it’s time to buy — or sell — the sector, here are five key themes to consider for 2019:

Trade and the economy

While some of the heat has gone out of the trade conflict in December, it remains a major topic for 2019, given its bearing on demand for metals. On a positive note, ArcelorMittal’s global presence seems to have worked in its favor as the company didn’t report any damage to its business so far. Specialized steelmakers such as Voestalpine AG and Kloeckner AG are less fortunate, already warning of the consequences.

Stainless steel is another beaten-down subsector. Aperam SA, Outokumpu Oyj and Acerinox SA have all slumped at least 30 percent since October as they struggle to contend with cheaper imports and oversupply.

The Chinese government has said repeatedly that it will support the economy, but investor-pleasing measures have yet to materialize.

“Lately, commodity markets have shown persistent concerns over China macro conditions into 2019,” according to Citigroup Inc. strategists wrote in a note on Dec. 17. “Mixed China macro data, including a sharp slowdown in household consumption, call for more policy fine-tuning into 2019. On the positive side, investment across infrastructure, manufacturing and property improved with levels of infrastructure investment surging in November following weak readings over the past few months.”

Chinese policy

It’s been a year of slowing economic growth and weaker purchasing managers index readings for the world’s biggest metals consumer. The Chinese government has said repeatedly that it will support the economy, but investor-pleasing measures have yet to materialize.

Credit Suisse analysts have seen cause for a degree of optimism. “While fiscal caution should limit the scope of stimulus, we cannot rule out the Chinese government reacting to trade tensions and growth pressures by ‘going back to what it knows’ via infrastructural/construction investment, which would provide a boost for commodity demand,” the analysts wrote in a note on Dec. 17.

Beijing’s environmental policies also have implications for steel prices and iron-ore consumption. Investors will look for further updates on local production curbs that may have been offset by imports. The picture could prove positive for ArcelorMittal, which will update investors on Feb. 7.

Tougher pollution rules are also driving a shift to high-grade iron ore among Chinese steelmakers. Top quality producers BHP Group Plc and Rio Tinto Plc are obvious beneficiaries, as is high-grade iron ore pure-play Ferrexpo Plc.

M&A and cash returns

Miners showed progress in deleveraging by selling large assets to focus on core areas. BHP and Rio Tinto have cleaned up their balance sheets and rewarded investors generously with buybacks and special dividends. BHP alone returned about $21 billion over the past two years.

This is unlikely to happen again in 2019, so attention will turn to regular payments in a sector that trades at a dividend yield of about 5.7 percent, and to capital spending on new projects and M&A.

Palladium should continue to benefit from strong fundamentals in 2019

Talking of deals, progress in a few transactions will engage investors. The combination of Randgold Resources Ltd. and Barrick Gold Corp. is due to be completed by the end of 2018. There are questions about the future of Acacia Mining Plc, about 64 percent owned by Barrick. With gold producers struggling to contain cost inflation, further consolidation can’t be ruled out. A battle to control SolGold Plc is looming, with both BHP and Newcrest Mining Ltd. building stakes in the promising copper and gold producer.

Precious metals

Gold reclaimed its haven status late in 2018, delivering a boost to bullion producers in the final quarter of the year. Randgold, Acacia Mining and Polymetal International Plc could prolong recent gains into 2019 should doubts about the global economy and volatility in equities persist continue to dog investors.

Palladium topped gold this year, as demand from the auto industry soared in a switch from diesel engines to gasoline-powered cars, which tend to use more palladium in autocatalysts. The metal “should continue to benefit from strong fundamentals in 2019,” according to Bloomberg Intelligence analysts, potentially favoring palladium-exposed Lonmin Plc and MMC Norilsk Nickel PJSC.

Special cases

Glencore Plc will again demand investor attention. The world’s largest commodity trader is under investigation by the U.S. Department of Justice for alleged bribery practices in the Democratic Republic of Congo, Venezuela and Nigeria. The miner has lost about 20 percent of its value since the investigation was made public on July 3. Glencore is the cheapest among large-cap mining and metals companies, trading at a 7.8 forward price-to-earning ratio. Based on recent copper-mine transactions, Glencore’s red-metal assets would be worth more than its total market value, according to Sanford C. Bernstein & Co. analysts.

Aluminum has been a disrupted market in 2018. Sanctions continue to overshadow United Company RUSAL Plc, the largest producer, while Norsk Hydro ASA’s Alunorte plant in Brazil, the world’s biggest aluminum factory, remains at reduced capacity, pending a water-pollution investigation. A return to full output at Alunorte will be key for Norsk Hydro’s earnings and would ease tensions in aluminum supply.

Stretched balance sheets will be another potential red flag. With prices falling and margin pressure mounting, difficulties may deepen for leveraged companies. Copper smelter Nyrstar NV lost more than 90 percent of its value in 2018 on cash-flow concerns and doubts about its debt repayment capacity. The final chapter of this story could come in September 2019 when a large chunk of its bond burden matures.

(By Michael Msika)

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments