Column: Funds keep faith with copper even as squeeze fades

The vicious squeeze on the CME copper contract appears to have largely passed but fund managers are sticking with their bullish convictions on both US and London markets.

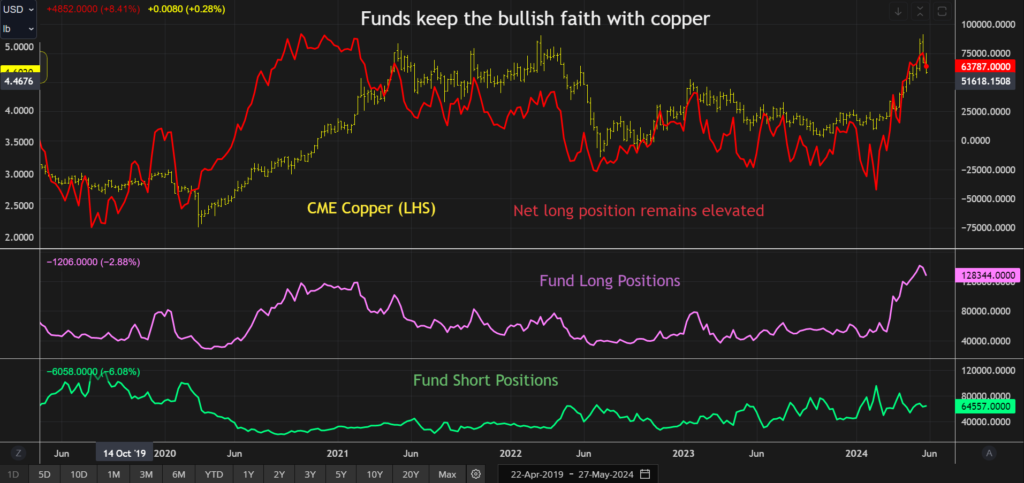

There has been some light profit-taking as the price has retreated from last month’s record highs but fund long positioning remains elevated both on the CME and London Metal Exchange (LME).

The money surge into copper is part and parcel of a broader rotation of funds into the base metals sector but copper’s super-charged rally to a CME peak of 5.20 cents per lb and an LME high of $11,404.50 per ton has made it the star attraction.

However, Doctor Copper’s new investor friends may find their bullish resolve tested in the days ahead.

With the short-covering momentum on the CME contract now abating, fund longs are left waiting for fundamentals to catch up with their price expectations.

Long and strong

Fund managers trimmed their long positions on the CME copper contract by 7.4% over the week to May 28, according to the latest Commitments of Traders Report (COTR).

However, bets on higher prices amounted to a hefty 128,344 contracts, which is still the largest bull commitment since January 2018.

The net collective long position is lower at 63,787 contracts. There has been no short capitulation. Indeed outright money manager short positions edged up by 2.0% to 64,557 contracts.

However, it’s clear that the bulk of the recent investment flow remains sitting on the long side of the market.

The situation is similar in London, where the record investment long position shrank only marginally in the week to May 20. At 105,262 contracts, it is still by some margin higher than anything seen since the LME launched its own COTR in 2018.

Squeeze dissipates

The upwards price momentum has faded as the CME squeeze has steadily dissipated, LME three-month metal currently consolidating just above the $10,000 level.

There remain pockets of tightness across nearby CME time-spreads but the immediate panic appears to be over and the cash premium over the London contract has shrunk from over $1,000 per ton in the middle of May to around $250.

Short positions have either been covered or rolled with a view to delivering physical copper.

The explosion in the arbitrage with the LME is expected to draw metal to CME warehouses in the United States.

Some 100,000 tons of copper are reported to be on their way, although nothing has yet arrived.

CME registered stocks fell another 2,256 short tons last week to a six-month low of 16,607 tons.

Chinese glut

Outside of the United States, though, copper stocks have been building.

LME headline inventory has edged up from an early-May low of 103,100 tons to a current 116,000 tons. The ratio of metal awaiting physical load-out has shrunk from 20% at the start of May to just 5%, or 6,025 tons.

The stocks build in China has been more pronounced.

Shanghai Futures Exchange warehouses hold 321,695 tons of copper, the most since April 2020.

This year has seen the usual seasonal surge around the Chinese New Year holidays but not the usual post-holiday decline. Stocks have simply continued climbing, up another 20,731 tons over the course of last week.

Local data provider Shanghai Metal Market estimates bonded warehouse stocks have also risen from under 10,000 tons at the start of the year to 76,000 tons.

Clearly, no-one is short of copper in China right now.

Waiting game

Copper’s recent rally to all-time highs has been accompanied by a profusion of headlines about the lack of supply growth relative to strong energy-transition demand.

The bull narrative has spread far beyond the closeted world of industrial metal traders to the retail investment crowd.

Fear of missing out has played its part in the buying frenzy and it’s understandable given the ever higher price forecasts being bandied around.

Hedge fund manager Pierre Andurand has grabbed the super-bull crown, telling the Financial Times he expects copper to nearly quadruple in price to $40,000 over the coming years.

It’s worth stressing the extended time-frame around that prediction because right now copper dynamics don’t look quite so bullish.

The extent of the stocks build in China is a major discrepancy in copper’s bull narrative.

The country is the world’s largest buyer of the metal but shows every sign of entering a de-stocking cycle in response to the recent price surge and still-stuttering demand.

Bullish fund managers may face a tense wait for supply-chain reality to catch up with copper’s elevated price.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by David Evans)

More News

Northern Star replaces CEO, activist investor Elliott wants more

July 01, 2026 | 08:29 pm

Ukraine urges swift publication of Irish investigation into alumina exports

July 01, 2026 | 01:22 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments