Global cobalt glut won’t be stemmed by Glencore Congo output stoppage

LONDON – Disruptions to cobalt supplies in the Democratic Republic of Congo are not expected to eradicate a glut of the material used to make batteries for electric vehicles, thwarting hopes that prices can be boosted from their lowest since March last year.

Glencore last week said its subsidiary Katanga Mining had halted cobalt exports from the Kamoto Project in DRC while it builds a facility to remove uranium.

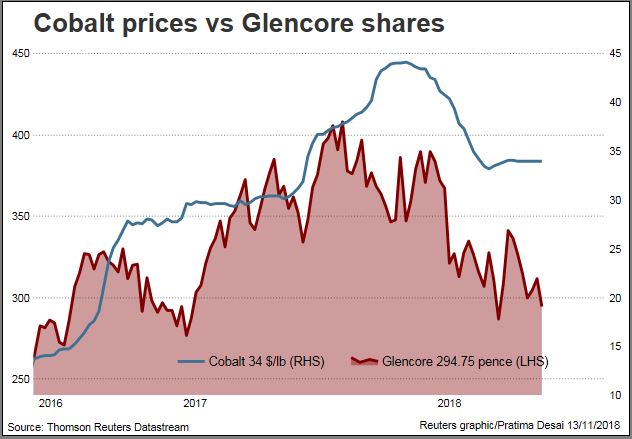

Prices of cobalt metal, at around $55,000 a tonne, have barely moved since the announcement on Nov. 6.

The metal crashed below $50,000 a tonne earlier this month from above $95,000 in March due to expectations of surpluses this year and next.

Guidance for cobalt production from Katanga was 11,000 tonnes this year and 34,000 tonnes in 2019.

To remove uranium, Katanga plans to build an Ion Exchange system at a cost of around $25 million, which should be completed by the end of the second quarter of next year, provided it obtains the necessary permits.

“It only makes the market look less bearish for the next 8 months or so,” said Vivienne Lloyd, an analyst at Macquarie.

Mined cobalt will be stored at the site and processed in the Ion Exchange system after construction. The processing and sale of the cobalt is expected to be completed before the end of the fourth quarter of 2019.

“The market will still be oversupplied next year as they are planning to make up sales in the second half and there are many others selling cobalt hydroxide,” Lloyd said.

While the industry typically talks about cobalt metal, the surplus is in cobalt hydroxide, used to make sulphates for the cathode part of the lithium-ion batteries used to power electric cars, a fast-growing sector of the auto industry.

Hydroxide comes from Congo, which has the world’s largest reserves of cobalt, expected to produce nearly 90,000 tonnes this year in a market estimated at around 135,000 tonnes.

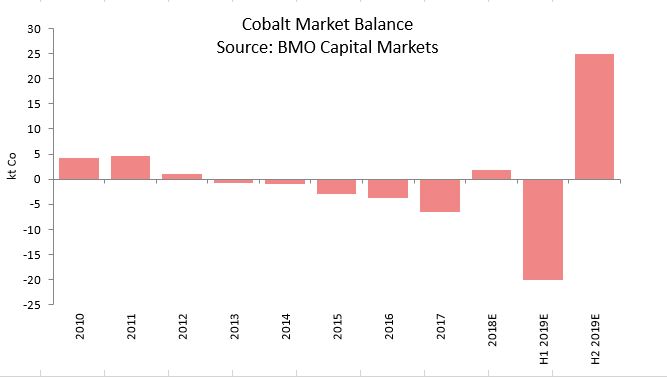

“We had been forecasting the largest cobalt surplus on record for 2019, albeit in a market with 13 percent consumption growth,” BMO Capital Markets analyst Colin Hamilton said.

“Taking out the planned 30,000 tonnes of mine supply from Kamoto, however, leaves first half 2019 in the largest deficit on record. But should Kamoto play catch-up in the second half, we would have an aggressive swing to surplus.”

Hamilton expects to see a deficit of 20,000 tonnes in the first half of next year and a surplus of nearly 25,000 tonnes in the second half.

The outlook for market balances could change if there are long delays to getting the necessary permits and importing the equipment needed to build the plant in Congo.

However, analysts say a ramp-up of production at sites such as Metalkol in Congo, owned by Eurasian Resources Group, should ease any supply constraints for hydroxide.

“There is no shortage of cobalt hydroxide right now,” said CRU analyst George Heppel. “The main effect is going to be an increase in payables for hydroxides.”

Payables, a reference to the percentage of the cobalt metal price used to price hydroxide, hit levels above 90 percent last year and have since slipped to around 65 percent.

(By Pratima Desai; Editing by Veronica Brown and Jan Harvey)

More News

Boliden in talks to buy Votorantim’s controlling stake in Nexa

Nexa is one of the world's leading zinc producers.

July 02, 2026 | 02:50 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments