Gold price can’t rise on weak payrolls

The US economy added only 194,000 jobs in September, falling short of expectations, but the Fed can still taper soon — and gold knows it.

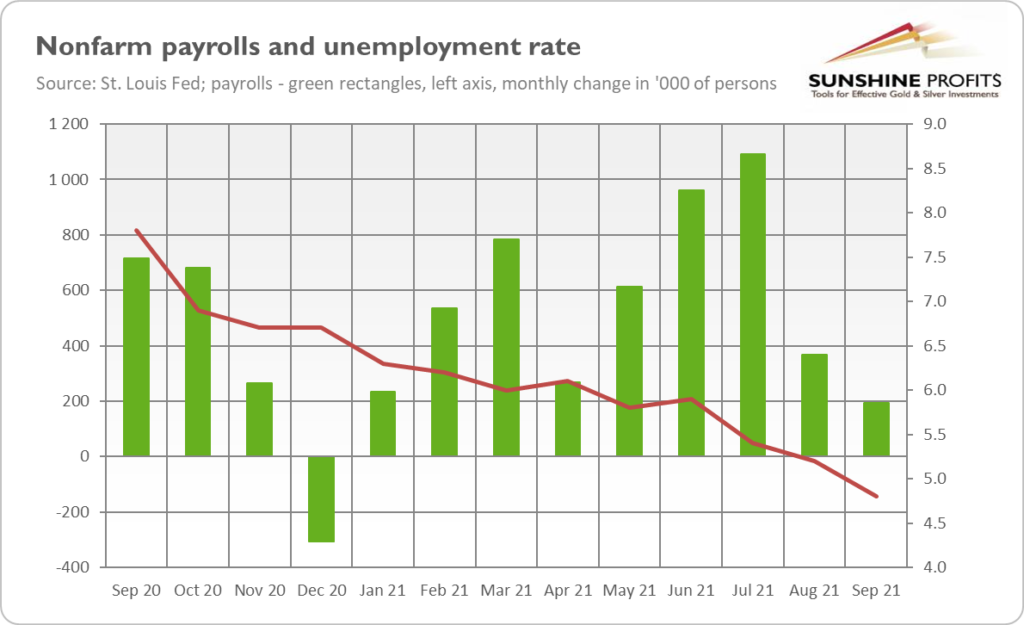

Another disappointment from the economy! The September nonfarm payrolls came surprisingly weak. As the chart below shows, the US labor market added only 194,000 jobs last month, much below the expectations (analysts forecasted about half a million added jobs). The disappointing numbers followed the additions of 1,091,000 in July and 366,000 in August (after an upward revision). The most recent job gains were the weakest since December 2020.

However, the overall report was generally more positive than the headline. First of all, the unemployment rate declined from 5.2% to 4.8%, as the chart above shows. It’s a positive surprise, as economists expected a drop to only 5.1%. In absolute terms, the number of unemployed people fell by 710,000 – to 7.7 million. It’s a considerably lower level compared to the recessionary peak, but still significantly higher than before the pandemic (5.7 million and unemployment rate of 3.5%).

Second, taking revisions into account, the employment in July and August combined is 169,000 higher than previously reported. It means that the monthly job growth has averaged 561,000 so far this year and about 550,000 over the last three months.

Third, the main reason for the very weak nonfarm payrolls was a decline in local and state government education – by 161,000. Most back-to-school-hiring typically occurs in September, but the recruitment last month was lower than usual, which some analysts attribute to early retirement of some teachers, mask-wearing mandates and vaccination requirements. Another issue is that the report is based on data that was collected when the Delta variant of the coronavirus was reaching its peak, and now the situation looks better.

Implications for gold

What does the recent employment report imply for the Fed’s monetary policy and the gold market? Well, Fed Chair Jerome Powell told reporters during his press conference in September that he would like to see a “reasonably good” or “decent” employment report before deciding that the Fed’s threshold for reducing its asset purchasing program has been met.

So, you know, for me, it wouldn’t take a knockout, great, super strong employment report. It would take a reasonably good employment report for me to feel like that test is met. And others on the Committee, many on the Committee feel that the test is already met. Others want to see more progress. And, you know, we’ll work it out as we go. But I would say that, in my own thinking, the test is all but met. So I don’t personally need to see a very strong employment report, but I’d like it see a decent employment report.

Now, the question is whether 194,000 job gains are decent enough to taper the quantitative easing. Interpreting words of an oracle is never an easy task. The September payrolls are neither strong nor a catastrophe. However, given the level of expectations and the fact that job gains were weaker than in August (commonly considered a great disappointment) I wouldn’t describe the latest payrolls as “decent”.

However, we have to remember that the overall report was much better than the payrolls analyzed in isolation. Given the significant decline in the unemployment rate, the September employment report can be defended as “decent”. So, the Fed can still taper in November, or announce it at least, especially that some members of the FOMC were ready to tighten US monetary policy already in September.

It seems that my line of thinking is in line with the market’s interpretation of the Fed’s likely course of action. The price of gold jumped briefly on Friday above $1,780, but it could not break the resistance or hold this position and returned quickly to its recent comfort zone of $1,750-1,760. The rather shy reaction of the yellow metal can be seen on the chart below.

Gold’s inability to shine in response to the second weak nonfarm payrolls in a row or to the inflation worries is quite disappointing. Well, Mr. Market decided that the September employment report wouldn’t restrain the Fed from tapering. The focus on the upcoming tightening cycle creates downward pressure on gold prices, which counterweighs worries about the labor market or inflation.

However, it might be the case that the price of the yellow metal will bottom somewhere around the actual start of tapering, and, without all that pressure around the tapering announcement, it could be free to move upward again.

(By Arkadiusz Sieron)

More News

BHP seeks to restart Cerro Colorado mine with $1.5B investment

The copper mine has been closed since late 2023 after it was denied its water permit.

July 02, 2026 | 10:43 am

{kind=link}

{kind=link}

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments