Gold rally foiled again as payrolls torpedo weekly gain

Just when it looked like gold’s rally had gotten back on track, the US payrolls report came along.

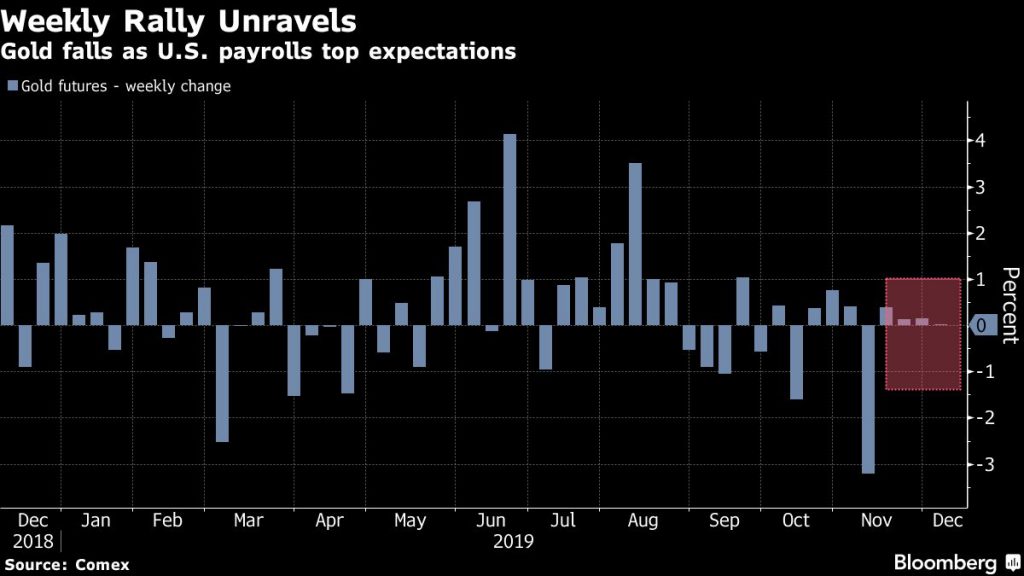

The number of jobs added to the economy jumped 266,000 last month, the most since January, according to a government report Friday that topped all estimates in a Bloomberg survey calling for 180,000 jobs.

Gold has struggled to sustain recent rallies as resilient US economic data and bets on progress toward a U.S.-China trade deal limit demand for the metal as a haven. That weakens the case for more cuts on U.S. borrowing costs, further damping the appeal of the non-interest-bearing precious metal. Prices are down more than 6% from a six-year high reached in September.

The jobs report “is a blow-away number: It means there will be no more interest-rate cut, which is bearish for gold,” says Phil Streible, senior market strategist at RJO Futures.

Bullion futures for February delivery fell 1.2% to settle at $1,465.10 an ounce at 1:30 p.m. on the Comex in New York. Prices slipped 0.5% for the week.

The jobless rate dipped to 3.5%, matching the lowest since 1969. Average hourly earnings climbed 3.1% from a year earlier, exceeding projections, and the prior month was revised higher.

Earlier Friday, equities rose after China said it’s in the process of waiving retaliatory tariffs on imports of U.S. pork and soy by domestic companies. That’s a procedural step that may also signal a broader trade agreement with the U.S. is drawing closer.

“China is waiving some tariffs, which means we’re close to an agreement,” also weighing on gold, Streible said.

(By Yvonne Yue Li)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments