Is China locking up Indonesian nickel?

As it has done with cobalt, graphite and rare earths, China appears to be locking up the nickel market.

Nickel’s top producer, Indonesia, in early September decided to accelerate a scheduled ban on ore export shipments, from 2022 to January 1, 2020. The ban which instead took immediate effect on Oct. 28, is to encourage the building of domestic smelters instead of exporting raw nickel, and other metals, for processing abroad. (the country did the same thing in 2014 but lifted the ban three years later).

No coincidence

Is it any coincidence that Indonesia decided in September to ban nickel ore exports, just a few weeks after a meeting between Indonesian president Joko Widodo and Chinese industrial executives, including Xiang Guanda, who in partnership with his wife, runs Tsingshan Holding Group?

We think not. Tsingshan is the world’s biggest stainless steel-maker, and has substantial investments in Indonesian nickel.

The Chinese metals giant is known for causing a major disruption to the nickel market in the mid-2000s, when it and other Chinese companies massively adopted nickel pig iron (NPI), crushing the nickel price. The firm went on to build low-cost NPI plants in Indonesia.

Tsingshan now plans to construct an Indonesian plant to produce nickel-cobalt salts from nickel laterite ores. Using previously uneconomic technology Tsingshan says it will transform class 2 laterite deposits into class 1 metal for the battery market.

Class 2 nickel is primarily used to make stainless steel, which accounts for two-thirds of global nickel demand. Sulfide deposits provide ore for Class 1 nickel users which includes battery manufacturers. These battery-cos purchase nickel sulfate, derived from high-grade nickel sulfide deposits. It’s important to note that less than half of the world’s nickel is suitable for the biggest growth market – EV batteries.

At the July meeting in the presidential palace, Xiang reportedly offered several policy suggestions” on improving Indonesia’s business environment and briefed the group on plans to expand Tsingshan’s total investment in the country to $15 billion, including a plant making nickel chemicals for electric-car batteries, according to a press release from the company. Two months later, Indonesia announced it would bring forward a ban on nickel ore exports by two years.

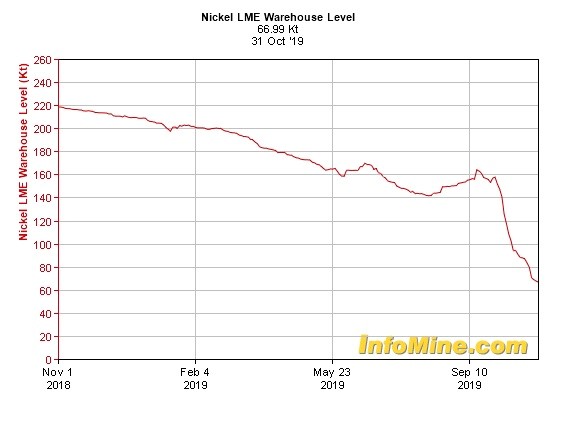

Tsingshan has also raised eyebrows among metal traders in London for drawing down abnormally large quantities of metal from LME warehouses – causing nickel stockpiles to fall to an 11-year low.

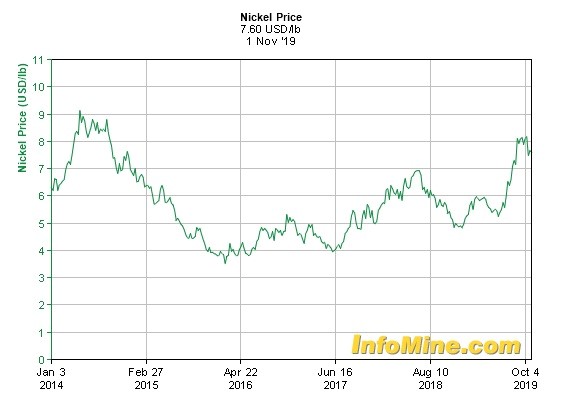

The draw-downs occurred in two phases. In July nickel prices shot past $6.00 per pound as a result of nickel inventories in LME warehouses dropping to 150,000 tonnes.

In early September, Indonesia announced the nickel export ban would be moved forward two years, causing nickel to jump 8.8% to its highest price in five years.

Between the last week of September and October 24, another nickel buying binge took place. Warehouse inventories plummeted from 152,000 tonnes to 87,132t – their lowest since 2012. The 25,000 tonnes that left storage was the largest amount withdrawn in the 40 years of the nickel contract.

A media report says Tsingshan Holding Group was one of the main forces behind the record draw-down, along with JP Morgan. The LME is reportedly reviewing recent trading in the nickel market to “ensure that the client’s activity is not conducive to an abusive squeeze or other pattern of market abuse/disorderly market conduct,” according to an email sent to LME members.

At Ahead of the Herd we find the timing extremely suspicious. Tsingshan says it took so much metal out of warehouses to secure supplies, ahead of the looming ban on Indonesia raw metal exports. That seems plausible. And perfectly legit, if it didn’t know about the ban until it was announced early September.

But how about the significant draw-down in July? Could it be that Tsingshan’s Xiang Guanda was told during his meeting with the President and those Chinese officials, about the export ban being imposed earlier than 2022 (or perhaps that was part of a deal made during the meeting), and took the opportunity to move nickel out of storage before prices went up following the official ban announcement?

Being the paranoid type, I find it very unlikely there is a coincidence between Tsingshan buying up record nickel inventories, and the nickel export ban being imposed, just weeks apart.

It appears to me that China, through its “Trojan Horse” Tsingshan Holdings, is trying to corner the nickel market – or at the very least, Indonesia’s share of it.

The proof

It didn’t take long to find evidence to support my hypothesis; it’s right in the news release issued on July 15 by Tsingshan Holding Group. The bottom of the page shows six Chinese men posing for a photo. Apart from Xiang Guanda, who are the others? The group includes You Xiaoping (any relation to Deng Xiaoping, the former Chinese President?), chairman of Zheijiang Huayou Cobalt Co.; the president of Guangdong Brunp Recycling Technology Co., Ltd.; and Huang Weifeng, chair of Shanghai Decent Investment (Group) Co., Ltd., a subsidiary of Tsingshan.

Cobalt eh? We know from a previous article that China basically owns cobalt processing – the country is heavily invested in the DRC, by far the world’s biggest cobalt producer, mining about two-thirds of the critical metal – as it works towards its goal of mass EV adoption, and ensures its factories have access to clean-technology raw materials like cobalt, lithium and graphite.

In a $9 billion joint venture with the DRC government, China got the rights to the vast copper and cobalt resources of the North Kivu in exchange for providing $6 billion worth of infrastructure including roads, dams, hospitals, schools and railway links. China controls about 85% of global cobalt supply, including an offtake agreement with Glencore, the largest producer of the mineral, to sell cobalt hydroxide to Chinese chemicals firm GEM. China Molybdenum is the largest shareholder in the major DRC copper-cobalt mine Tenke Fungurume, which supplies cobalt to the Kokkola refinery in Finland. China imports 98% of its cobalt from the DRC and produces around half of the world’s refined cobalt.

Interesting. We learn from the news release that the Huafon Group and Tsingshan Holding Group signed an agreement on Aug. 27 establishing a joint venture in Indonesia. The $3 billion JV is expected to produce 12 million tonnes of coke fuel per annum; coke is made from metallurgical coal in iron and steel-making.

A nugget appears a bit further down in a comment from You Xiaoping:

“You [Xiaoping] added that the cooperation marks another milestone for Huafon in expanding abroad, after the company established industrial bases and sales branches in many countries involved in the Belt and Road Initiative, such as Turkey, Vietnam, India and Pakistan.”

Now we’re getting somewhere. These two Chinese conglomerates are cooperating in a large industrial industrial enterprise to produce coke made for iron and steel production, presumably for sale to some of the nearly 150 countries (according to China) that have signed up for its Belt and Road Initiative (BRI).

Our analysis has shown that the BRI poses more risks for developing countries than rewards. This JV presumably will use Indonesian coal to meet Chinese objectives in pulling central Asian, and other markets within its own trading orbit.

It’s also interesting to note from Tsingshan’s news release, how the promised $15 billion will be allocated to Indonesia. Eight billion has already been sunk into the Morowali industrial park on the island of Sulawesi. Tsingshan’s stainless steel mill on the island started in 2017 with a capacity of 2 million tonnes per annum and has since been upgraded to 3Mtpa of stainless steel hot-rolled coils.

Chinese investment in the 2,000-hectare industrial park is expected to reach $15 billion. We know that part of the remaining investment by Tsingshan is a plant making nickel chemicals for electric-car batteries.

In February Reuters reported on the $4 billion Chinese-led project to produce battery-grade nickel chemicals, that Indonesia hopes will attract electric-vehicle makers into the country, which is the second-largest car-maker in Southeast Asia.

The group of islands nation wants to become a global hub for producing and exporting electric vehicles to Asia and possibly Australia.

Toyota already plans to invest $2 billion over four years in developing EVs, starting with hybrids. Hyundai says it will produce EVs as part of an $880 million investment in the country.

In January construction started on the battery plant in Morowali, led by a consortium of Chinese developers including Tsingshan, battery company GEM Co Ltd., and units of CATL – the largest EV battery company in the world. Nickel feedstock for the plant would come from Indonesia’s nickel laterite ores (Tsingshan says the feed would be abandoned low-grade nickel ores).

Cobalt may also be part of the facility, according to electrive.com, as EV automakers aim to diversify supply from cobalt controversially sourced from the DRC. PR Newswire names a number of companies exploring for cobalt within Indonesia’s nickel laterite deposits. Ninety-nine percent of cobalt is unearthed as a by-product of copper and nickel mining.

Conclusion

Nickel is used in two of the dominant battery chemistries for EVs, the nickel-manganese-cobalt (NMC) battery used in the Chevy Bolt (also the Nissan Leaf and BMW i3) and the nickel-cobalt-aluminum (NCA) battery manufactured by Panasonic/Tesla.

Battery manufacturers have been developing nickel-rich NCM 811 batteries (80% nickel, 10% cobalt and 10% manganese) because they have longer lifespans and allows electric vehicles to go further on a single charge.

Most Chinese battery manufacturers use lower-cost lithium-iron-phosphate batteries ie. no nickel, but they are looking to migrate to nickel-containing batteries with several including Shanshan, Nichia, L&F & Reshine producing them. China’s biggest battery manufacturer, Contemporary Amperex Technology (CATL) told investors it has begun mass production of the NCM 811.

Jinchuan, China’s top nickel producer, plans to build a project in Guangxi that will produce raw materials for the EV battery market.

It makes sense to use more nickel in EV batteries, because doing so increases the battery’s energy density, thereby extending the vehicle’s range.

It also explains why China needs nickel sources to fuel its booming electric-vehicle industry. (China is by far the largest EV manufacturer, followed by the US) In 2018 China only produced 110,000 tonnes of nickel compared to 560,000t in Indonesia and 340,000 in the Philippines. If it’s switching from phosphate-based lithium-ion batteries to nickel-based, it needs a large, secure supply of the base metal.

The country already has a lock on cobalt, graphite and rare earths production, so why not get a monopoly on the nickel market, too? China appears to be using Indonesia’s ban on raw nickel exports to do just that. Not only did China buy up most of the world’s nickel stockpiles from under the nose of the LME, it also managed to give itself a two-year head-start on the rest of the world in working with Indonesia to develop a huge facility for developing battery-grade nickel. Chinese-led, of course. Because China doesn’t really care about helping Indonesia to become an EV battery hub. Its real goal is to establish a nickel-processing beach-head in the largest nickel producer in the world, using Chinese technology to process class 2 nickel laterite deposits into class 1 battery-grade metal. Then sell its nickel chemicals to battery companies either in China or Belt and Road countries, as it continues on the path to complete global metals domination.

(By Richard (Rick) Mills)

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified. AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice. AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

AOTH/Richard Mills is not a registered broker/financial advisor and does not hold any licenses. These are solely personal thoughts and opinions about finance and/or investments – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor. You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments but does suggest consulting your own registered broker/financial advisor with regards to any such transactions.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments