Critical minerals diplomacy surges, but few deals have teeth

Governments have signed more than 70 critical minerals agreements and policy frameworks since 2021 in a race to secure supply chains and reduce dependence on China, but the growing list of announcements masks a more important reality; most of these deals still lack the commitments needed to reshape global mineral markets.

In this context, the significance of this growing number of agreements for miners, investors and downstream manufacturers matters only insofar as these instruments can generate the conditions needed to advance project development, mobilize financing and support the emergence of alternative processing capacity outside China.

Paper promises

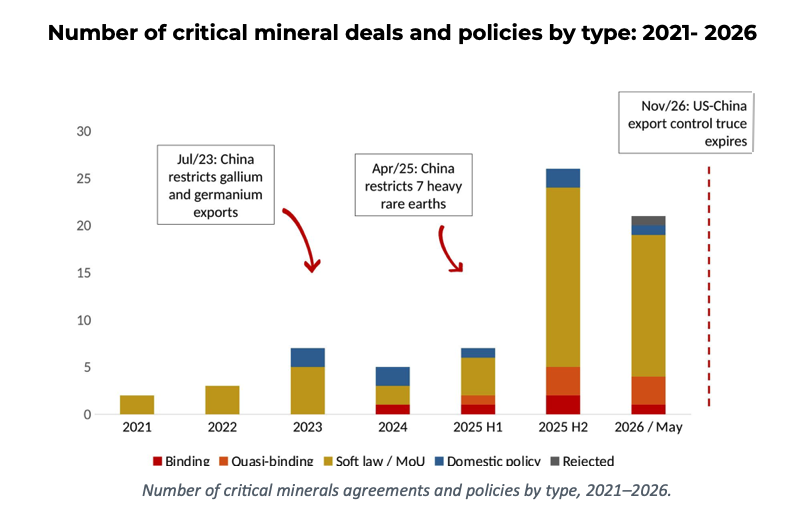

The scale of the diplomatic push is difficult to ignore. More than 50 bilateral and multilateral agreements have been announced in the past 18 months alone, involving major consuming nations including the United States, European Union, Japan and Australia. Yet a review of critical minerals agreements signed through May 2026 shows that more than 60% remain non-binding memorandums, partnerships or cooperation frameworks.

That distinction deserves far more attention than it receives. Although the expanding agreement map is often presented as evidence of progress toward supply-chain diversification, in reality, it says more about geopolitical alignment than mineral endowment. In that sense, the more relevant question now is the substance of the obligations created by those signatures, not the parties involved.

The answer matters because these agreements are supposed to underpin a multitrillion-dollar effort to reduce dependence on China, which continues to dominate mineral processing. China controls an estimated 60% to 90% of global rare-earth refining capacity and maintains leading positions across several strategic mineral supply chains.

Despite a flurry of diplomatic activity, most governments have stopped short of making commitments tied to specific investments, production targets, procurement requirements or financing mechanisms.

As a result, a gap is emerging between diplomatic momentum and the commercial certainty required to develop new mines, refineries, separation plants and battery supply chains. Admittedly, non-binding agreements can create political visibility and improve coordination, but they do not necessarily secure offtake, guarantee public financing, accelerate permitting or protect projects from future policy reversals.

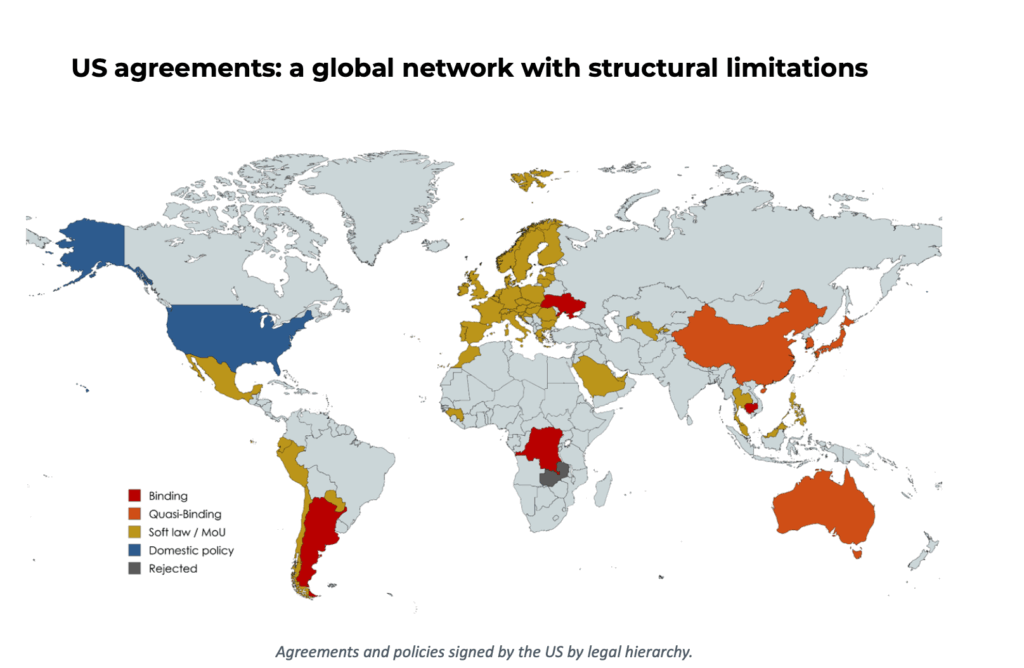

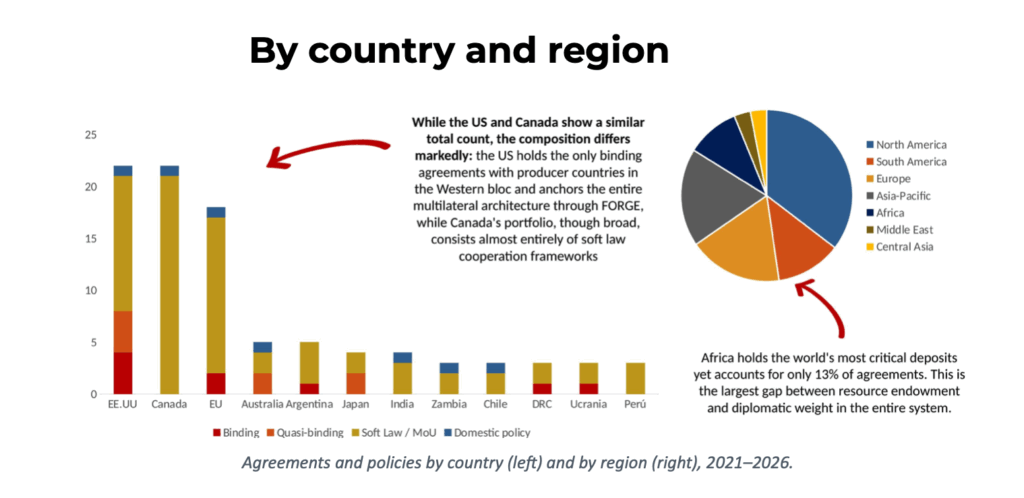

The US illustrates the challenge. Washington has signed more than 20 agreements in the past 18 months and has positioned itself as one of the most active participants in critical minerals diplomacy. Yet only a handful of those agreements are legally binding. Consequently, the result is a widening disconnect between the ambition to reduce China’s midstream dominance and the enforceable policy tools needed to achieve that objective.

The architecture now taking shape extends well beyond Washington. Initiatives such as FORGE, the US-EU-Japan critical minerals cooperation framework and the Critical Minerals Production Alliance are creating overlapping networks designed to strengthen supply chains among allied nations. Their architects argue, with some justification, that relationships established today can accelerate investment and project development tomorrow.

But from an industry perspective, not all agreements carry equal weight. The arrangements most likely to influence investment decisions are those that move beyond diplomatic coordination and incorporate operational or financial commitments. In practice, frameworks that include price floors, stockpiling mechanisms, co-financing arrangements, permitting cooperation or procurement support are far more consequential than broad declarations of intent.

Resource leverage

That is not to say non-binding agreements lack value. Indeed, they can influence capital flows, encourage technical cooperation and provide political backing for mining projects. Resource development unfolds over decades, and governments often prefer flexible arrangements that can evolve alongside markets and geopolitical priorities.

Still, flexibility has limits. Companies evaluating multibillion-dollar projects require more than political goodwill. In this context, support becomes meaningful only when it can be translated into bankable demand, infrastructure, financing and regulatory certainty.

One of the most revealing gaps in the emerging network appears in Africa. The continent hosts more than 60% of global cobalt reserves as well as significant deposits of copper, graphite and rare earth elements, yet it accounts for a relatively small share of the agreements signed so far. At the same time, recent developments suggest producer nations are becoming increasingly selective about the terms they are willing to accept.

A binding agreement between the US and the Democratic Republic of Congo highlighted Washington’s efforts to deepen ties with resource-rich jurisdictions and challenge Chinese influence in the cobalt supply chain. Zambia’s reported rejection of proposed US conditions, meanwhile, underscored a broader trend; host governments are asserting greater control over how their resources are developed.

That shift may prove just as important as the competition among consuming nations. The critical minerals race is not simply about securing supply. Rather, it is also reshaping the bargaining power of producer countries. Governments that control strategic deposits are increasingly positioned to demand local value creation, infrastructure investment, processing capacity and policy flexibility in exchange for preferential access.

Not surprisingly, binding agreements remain concentrated among a relatively small group of strategic producers and partners, including Australia, Japan, Argentina, Ukraine and the DRC. In Europe, the Critical Raw Materials Act remains one of the few frameworks that contains legally enforceable diversification requirements.

Reality check

The urgency behind this diplomatic surge stems largely from rising trade tensions between Washington and Beijing. As those tensions continue to shape strategic planning on both sides, the scheduled expiry of the current US-China export-control truce later this year has become a focal point for policymakers and industry participants alike. Even if negotiations yield another extension, governments appear committed to maintaining the broader critical minerals architecture that has emerged over the past several years.

For miners and investors, the lesson is increasingly difficult to ignore. The race to build alternative supply chains is real, but the legal and financial foundations remain far less developed than the headlines suggest. So far, governments have demonstrated a willingness to sign agreements. What they have not yet demonstrated, at least on a scale, is a willingness to attach those agreements to the binding commitments that projects require.

Until more frameworks move beyond political declarations and toward commitments capable of supporting financing, offtake, processing and project execution, the industry’s effort to challenge China’s midstream dominance will remain more aspiration than achievement.

* Antonia Godoy Arias is a policy and regulatory affairs analyst at Plusmining consulting firm.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments