Lithium price plunge is pitting Cathie Wood against sector veterans

Lithium’s recent price collapse and the prospect that supply from new mines could accelerate the slump are stoking fierce debate in the electric-car battery industry.

It’s an argument that’s pitting ARK Investment Management Chief Executive Officer Cathie Wood against some of the sector’s most prominent voices.

Lithium carbonate in China, a key benchmark, has tumbled almost 30% since touching a record in November, a sharp reversal from the material surging more than 14-fold since mid-2020 as automakers rushed to lock in raw materials needed for the rapid expansion of their electric lineups.

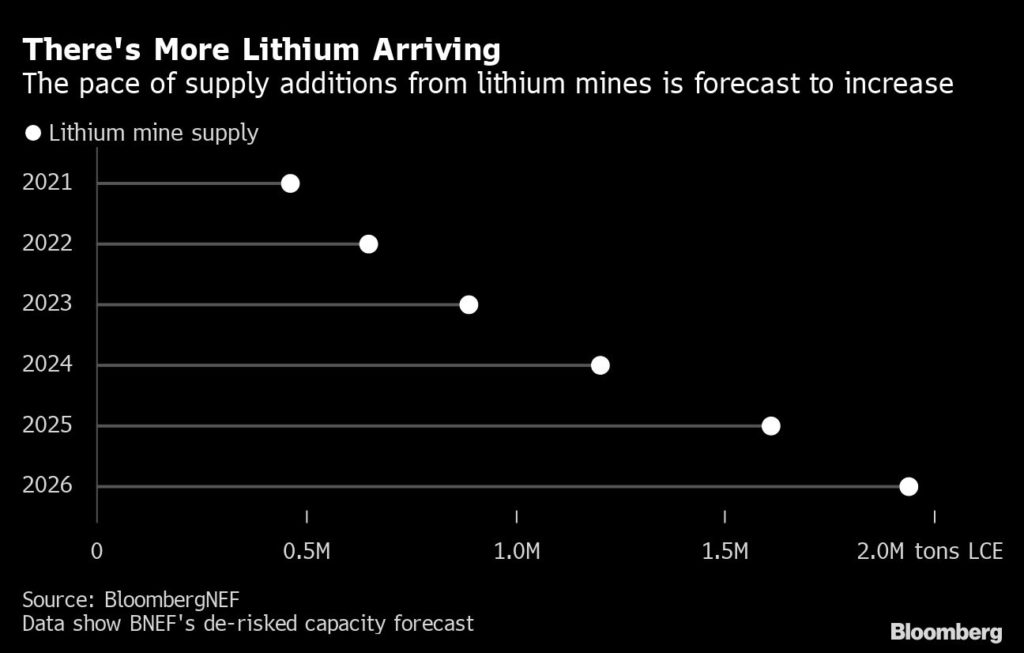

Signs of slower sales in China, the top EV market, along with concern about subsidy cuts and destocking activity across the battery supply chain have all weighed on lithium’s outlook. The potential impact of more supply is also now acutely in focus, with a stream of expansions or new projects that promise to get up and running this year.

Wood said last week that the extraordinary run-up in prices of the metal had been a “clarion call” for more production, and that the response from the industry means “odds are high that lithium will be in excess supply.” China Nonferrous Metals Industry Association, a leading industry group, has warned that rising supply could weigh on lithium prices this year, while BYD Co. said it expects the metal to stabilize in 2023.

Others including Joe Lowry, founder of advisory firm Global Lithium, insist demand is being underestimated and that these prognosticators fail to take into account the complexities of securing funding and permitting for new mines.

Suppliers are more bullish, too. “Early indications are both that cathode inventory and battery inventory in China are decreasing, which is a good sign for lithium sales,” Kent Masters, CEO of Albemarle Corp., one of the top global producers, told investors last week. The firm expects “continued favorable pricing for lithium” this year, according to a statement.

Another issue that my colleague Mark Burton and I highlighted earlier is whether less-established companies and nations will be able to deliver supply as promised.

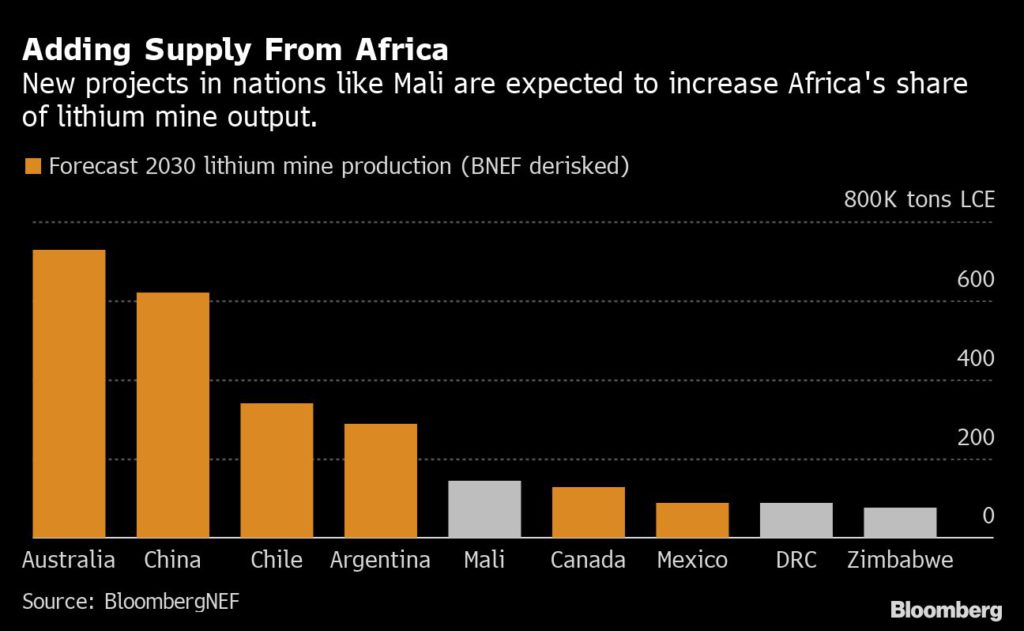

That’s particularly important for some of China’s key players, who are pinning hopes on the success of a cluster of new projects across Africa. The continent has emerged as a hotspot for Chinese lithium investment, and is becoming a counterpoint to US efforts to build out its own supply networks with free-trade partners and other allies like Canada and Australia.

Chinese refiners are preparing for miners in Australia to move into higher-value downstream chemical production, which could limit the volume of raw material available for export, according to Peng Xu, analyst at BloombergNEF.

Ganfeng Lithium Group Co. has invested in Goulamina mine in Mali, while Chengxin Lithium Group Co. has interests in Zimbabwe. Zhejiang Huayou Cobalt Co. and a unit of top battery maker Contemporary Amperex Technology Co. are among investors in a project in the Democratic Republic of Congo.

Several African nations will join the ranks of top producers of lithium raw materials through the end of the decade, according to data compiled by BloombergNEF. Many of those countries are already major suppliers of metals like copper and cobalt to Chinese companies that ship the materials for processing at their own domestic refineries.

“The least risky and best places for Chinese companies are probably places they have had success in the past,” said Jason Holden, a senior metals and mining analyst at S&P Global Commodity Insights.

(By Annie Lee)

More News

Congo plans first stock market as AI mineral boom draws interest

July 02, 2026 | 06:49 am

Agnico Eagle suspends Quebec pit mining, flags production hit

July 02, 2026 | 06:29 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

W

Cathie Wood is right, and all of the ‘usual’ Wall St Lithium ‘pundits’ are dead-wrong, with just more, of their ‘usual’, completely clueless, Blah Blah Blah Blah Blah Blah Blah Blah, about the price of Lithium collapsing this year, ..which, I might just add, has all been ..paid-for, by China’s CATL, in ..their ..own ..desperate attempts to undermine, and to drive down, the price of Lithium Supply, by spreading absolute reams of FUD, about Lithium demand, in China, during, the past few months, to ‘very conveniently’ coincide, with, the same period when most of China’s Lithium processors have been shut down and undertaking needed maintenance, and expansion work, upon ..enlarging, their Lithium processing plants..!! ???. Gee, I wonder why, they would be bothering to ..’enlarge’ their Chinese Lithium processing plants, if CATL, is right, and the global demand for Lithium is collapsing..?? ??? ????????