A glass half full or a glass half empty for lithium producers

Lithium producers’ share prices have been under pressure all year and some investors are no doubt wondering whether that is the end of the lithium boom. Metal bulletin research’s forecast is for the lithium market to shift into a supply surplus this year and as such we have expected prices to fall, so it is understandable that producers’ share prices are also suffering. But, with this just the dawn of the EV and ESS era, the main battery raw materials boom lies ahead.

The main battery raw materials boom lies ahead.

What we are seeing is the first significant supply response following the demand shock in 2015, when China endorsed the electric vehicle (EV) revolution. The demand shock led to a run up in prices to an average of $21,760 per tonne in 2017, from around $9,500 per tonne in the second half of 2015 (basis MB’s assessment of spot prices ex-works China). As well as boosting lithium producers’ share prices, it also incentivised producers and processors to build and expand capacity. While in recent years new capacity has suffered start-up issues and production of the right grades of material have been a problem for some, the combination of significant potential profit margins and the passage of time, mean many have now acquired the knowhow to produce the grades required. And, with a significant ramp up in mine supply, more spodumene and DSO is now expected to be processed into battery grade lithium.

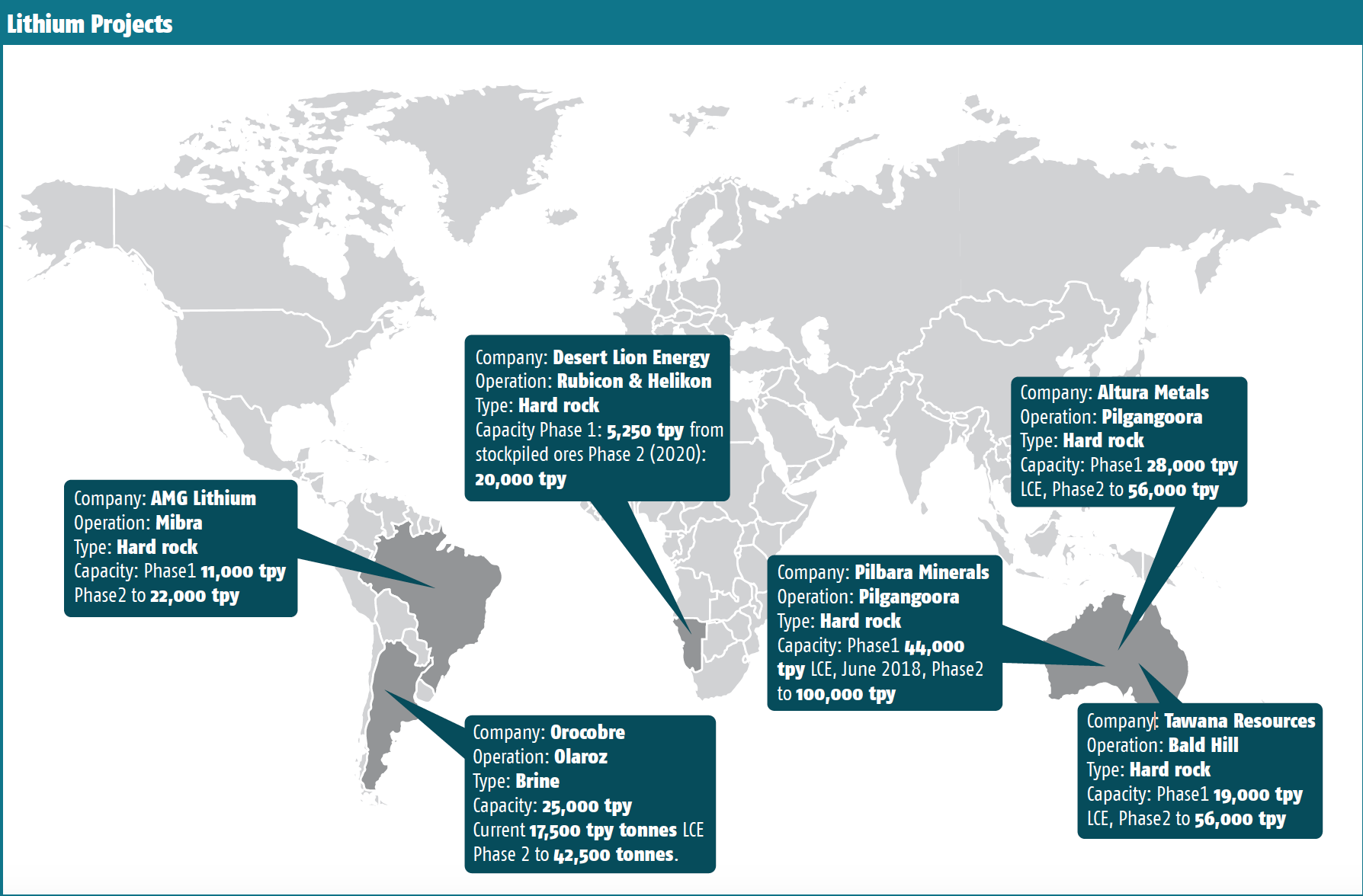

The ramp up of a handful new producers in 2018/2019 (see map below) is expected to shift the market into a supply surplus – not surprisingly prices are reacting accordingly.

While oversupply may be an issue for a year or two, the demand side of the equation is only going one way and that is sharply upwards.

Down the road, especially after 2023, demand is expected to see exponential growth on at least three counts. Firstly, falling battery prices are expected to make EVs cheaper to own and run than petrol/diesel vehicles. This is expected to make EVs the vehicle of choice. Secondly, governments are expected to increasingly push the EV agenda and thirdly, cheaper batteries will mean energy storage systems (ESS) become more feasible. As more energy is generated from renewable sources the need for grid load balancing and energy storage will grow rapidly. Compound average growth rates (CAGR) for lithium demand in the order of 15-19% are widely expected between now and 2025, with CAGR for EVs forecast to be around 25%.

Therefore, the big picture, medium-to-long term, outlook suggests that lithium and indeed all battery raw materials, have a very exciting time ahead of them and any pullback in lithium prices and producers’ share prices are likely to be temporary.

Glass half empty

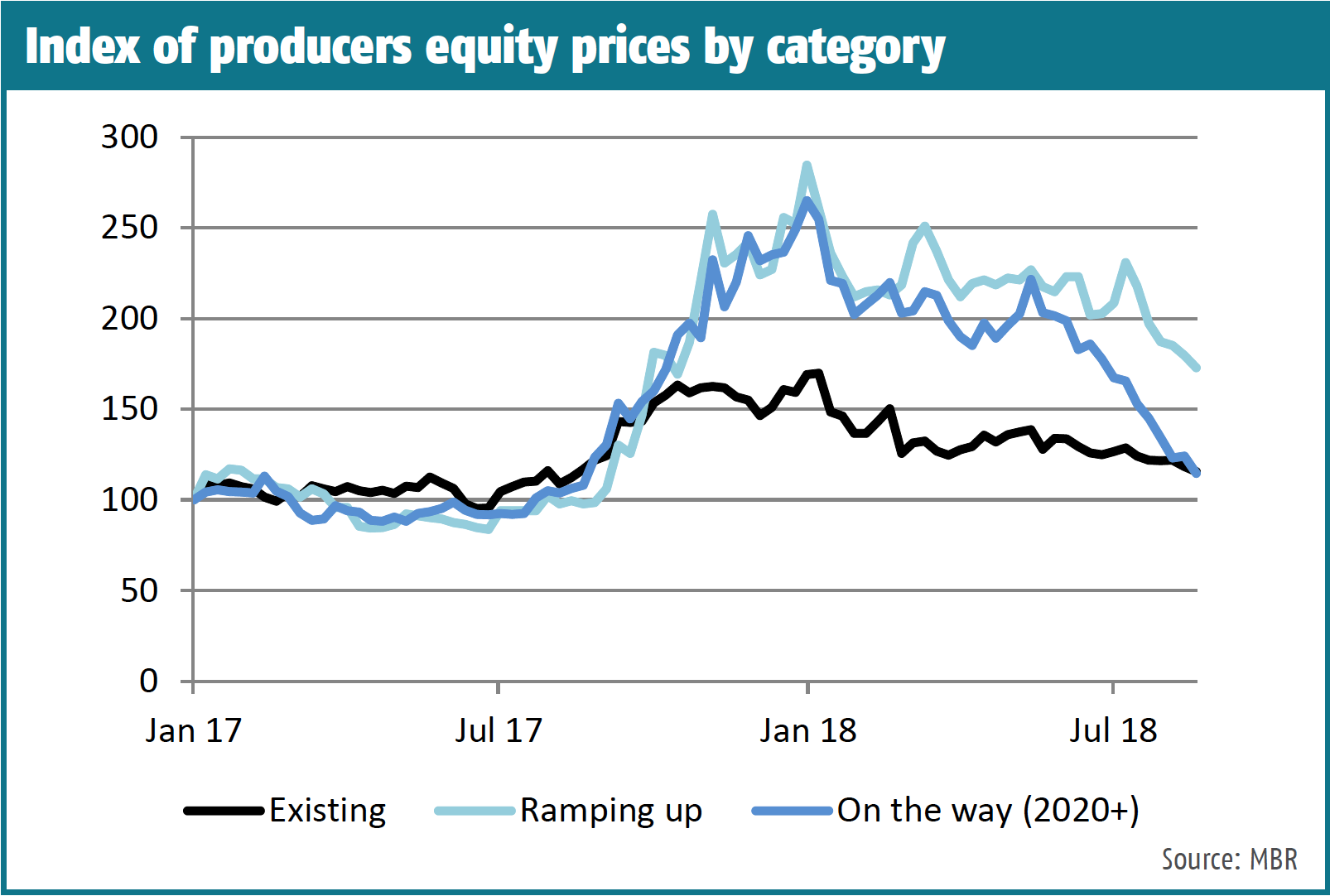

Like any commodity cycle price booms will be followed by price busts as supply responses hit the market. 2018 has heralded the first correction within the long term boom. As lithium prices started to turn lower in December 2017, the share prices of produces and juniors have not surprisingly been negatively affected, some more than others.

This is shown by the chart that shows the indices of various categories of producers: existing producers, those ramping up and those that are expected to start production in the early 2020’s. The indexes were calibrated at 100 at the start of 2017, so show the equities’ reaction to both the rising lithium prices seen in 2017 and to this year’s fall in price.

The more speculative end of the equity spectrum, that included the two sets of juniors (those close to being in production and those expected to be in production in the early 2020s), did well in 2017 when lithium prices were rising. This is because rising lithium prices meant the outlook was bright and potential profit margins for these companies were improving as prices climbed. Those producers now ramping up production have the advantage of being able to set long term contracts using a relatively high base price, while some of the existing producers will still have contracts based off prices from recent years.

Ironically, the share prices of existing producers, who would actually immediately benefit from higher price rises, saw their shares rise but not to the same extent as the juniors. At first sight this might seem odd, but this is partially because the existing producers in the index sell most of their output on long-term contracts – these long-term contract prices have actually lagged behind the spot prices, so they would not have been in a position to benefit from the rising spot market. For example, prices for large contracts cif Asia averaged around $14,000 per tonne in 2017, according to MB assessments, while us dollar equivalent spot prices, ex-works China, averaged around $21,760 per tonne, so the contract prices have not increased to the same degree as spot prices.

With spot prices falling, fortunes have changed. While the outlook has deteriorated, at least those producers that are ramping up production have been and are benefiting from relatively high prices where margins are still good. While those still a few years away from being in production run the risk of coming on stream when prices are lower, hence their shares have been hit the hardest.

With spot prices falling, fortunes have changed.

On a percentage basis since the start of 2017, the index of existing producers had climbed 70% and in late August 2018, the index was still 15% higher than at the start of 2017 – the correction from the top has been around 32%.

The index of those producers ramping up in 2018-2019, rallied 184% and was recently still 73% higher than at the start of the period, so it has corrected by 39%. The index of those producers not expected to be in production until the early 2020’s saw gains of 165% and the index now stands 14% above its start point, meaning it has corrected by 57%.

It should be noted that the corrections from the highs have accelerated since June this year. At the end of May the corrections stood at 22%, 24% and 23% respectively. The fact that other metals’ prices have fallen sharply since June with base metals down an average of 24%, tied into growing concerns about the fallout from US President Donald Trump’s trade war, suggests a significant amount of the correction in lithium equity prices may not be solely due to the lithium market. It does seem as though the lithium producers’ share prices have also been caught up in a broad based risk-reduction sell-off by investors.

This leads us on to the glass half full…

In recent months and weeks the lithium industry, along with the downstream companies such as processors, cathode and battery makers, as well as OEMs, have been active in securing their supply chains. This is a solid sign that industry insiders have complete confidence in the outlook for EVs and ESS. Reports of offtake agreements, joint ventures, equity partnerships, streaming deals and asset swaps, all show considerable upfront investment in an effort to secure supply. It is doubtful downstream companies would be so keen to lock in these deals if they expected ongoing surpluses.

Active in securing their supply chains.

With lithium producers’ and juniors’ share prices under pressure, the spate of consolidation within the industry and along the supply curve is likely to accelerate.

More News

Japan buyers agree on higher aluminum fees Due to war disruption

July 03, 2026 | 09:04 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments