Platinum market forecast to remain in balance in 2018

London, 8th March 2018: The World Platinum Investment Council (WPIC) today announces the publication of its latest Platinum Quarterly – the first independent, freely-available, quarterly analysis of the global platinum market. This report incorporates analysis of platinum supply and demand for the fourth quarter of 2017, the full year 2017 and a forecast for 2018.

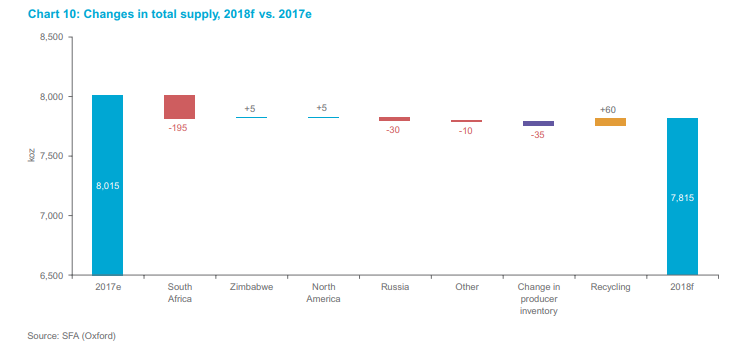

Today’s report shows that platinum supply and demand will be closely matched in 2018, returning the market to equilibrium (+25koz). Global platinum supply is forecast to be 7,815 koz in 2018, a decline of 2% from 2017, despite an anticipated increase in recycling of 60 koz to 1,965 koz. Total mining supply for 2018 is expected to decline by 4% to 5,850 koz, mostly owing to reduced output from South Africa following some mine closures in 2017 and lower production in Russia.

Global demand is projected to grow marginally in 2018 to 7,790 koz, as a recovery in industrial demand and an increase in jewellery demand outweigh a decline in automotive demand and slightly lower investment demand.

Paul Wilson, chief executive officer of WPIC commented:

“While 2017 was a challenging year for platinum, early indications show signs of a market that is moving in the right direction in 2018. Supply is tightening and demand remains resilient. These promising fundamentals, paired with elevated global uncertainty and a better economic growth outlook, mean macro conditions are becoming increasingly helpful to the platinum market.

“The importance of China to platinum is underlined in today’s report. The final quarter of 2017 has shown welcome, albeit tentative, signs that jewellery demand in the country is improving. We expect this trend to continue through 2018, with ongoing strength across other regions.

“While concerns about automotive demand weigh negatively on platinum sentiment, we believe that these concerns are, once again, overdone. The policy environment for diesel vehicles remains in flux, especially in Europe. Nevertheless, our broad perspective, including the environmental need to reduce CO2 emissions, significant hurdles to mass battery electric vehicle adoption, and automakers already able to genuinely clean up diesel NOx emissions, means we firmly believe clean diesel vehicles will be on the road for years to come.”

Alongside the 2018 forecast, today’s report shows a shift in the market balance for the full year 2017. Total platinum supply grew 1% in 2017, with the market ending 2017 in a 250 koz surplus. This revision is largely due to higher than expected supply from South Africa and a jump in recycling volumes in the fourth quarter of 2017. Global demand, meanwhile, fell 7% year-on-year, amid lower demand in all major market segments.

Automotive demand fell 3% in 2017, due primarily to falling demand in Western Europe. The market did, however, experience growth in commercial vehicles in China and the rest of the world.

Global jewellery demand slipped 2% to 2,460 koz as gains in other regions struggled to offset a decline in China.

Total investment demand was also lower in 2017 at 260 koz, due primarily to a decrease in Japanese bar buying. However, ETF investment rebounded strongly in 2017 after two years of declines, with global holdings rising by 95 koz. The largest increase took place in the US, where investors added 90 koz to their holdings last year.

To download this edition of Platinum Quarterly and/or subscribe to receive the research in the future, without charge, please visit our website: www.platinuminvestment.com

More News

Column: Battery metals recovery runs into stop-start EV market

Prices of lithium, cobalt and nickel have all recovered from their 2024-2025 lows.

July 05, 2026 | 10:09 am

Zimbabwe lab sees regional gold hunt accelerate as prices soar

July 03, 2026 | 11:49 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments