That confidence has been validated by prices for their key product. As we argued a couple of months ago, the trade tensions that have sunk LME copper in recent months actually proved rather benign for rust, which has risen about 10 percent over the past six months. The red metal, meanwhile, has fallen by the same amount.

The mystifying thing about this price action is that it’s confounded by China’s consumption data. Apparent demand – as measured by domestic production, plus net imports, plus drawdowns from port inventory – has slumped this year to its lowest level on a seasonal basis since 2010. August and September are traditionally the peak of the market, but the August figure this year has been lower than what we’ve seen around the Lunar New Year trough of late.

A look at finished-steel production data at first seem to ratify that conclusion. Screen out the swings of the annual-output cycles, and the market appears to have been standing still since 2016, with no significant year-on-year growth.

That seems to defy economic logic. If demand is flat or falling and supply is increasing, prices should be weak. So what gives?

The best explanation is that China’s notoriously sketchy data is finally starting to resemble reality a little more closely. Have another look at those steel production figures in the chart above, for instance: While finished steel is treading water, measures of the intermediate products of pig iron and crude steel have jumped over the past year to record levels.

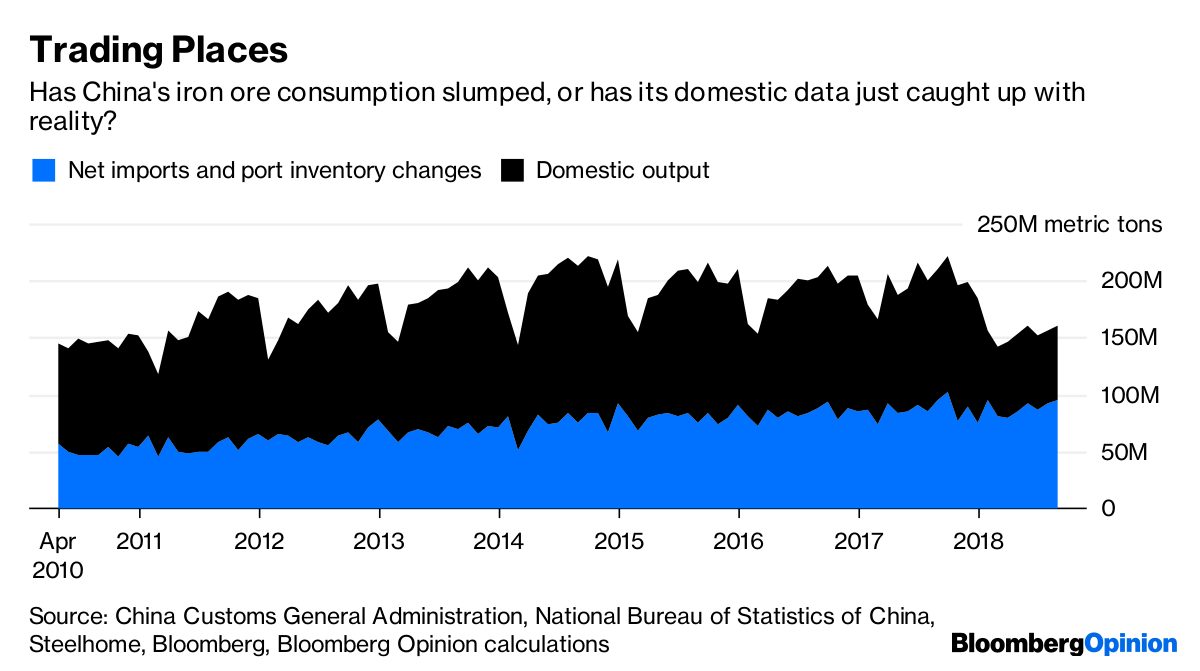

It’s similar when you look at the iron-ore demand data. Shipments reported by China’s customs bureau and movements in port inventory show a remarkably stable pattern. The real trend break this year comes entirely from a collapse in reported domestic output figures:

What seems to be happening is that iron-ore output has been overreported while the figures for pig-iron and crude-steel have been underreported for many years. That’s probably a result of the way China’s statistics bureau leans on data sampling from larger operations, and how the country’s ongoing restructuring of its heavy industry has regularized and consolidated a lot of steel production previously happening off-the-books at small-scale furnaces.

There’s another problem, though. As Sanford C. Bernstein & Co. analyst Paul Gait pointed out in a note to clients earlier this year, finished-steel output should never be consistently greater than that for crude steel, since there tend to be production losses along the way. China also doesn’t import crude steel in any significant quantities.

How does this fit together with the miners’ production data? One argument in favor of Vale, Rio Tinto and BHP has always been that their ore is higher quality than that of China’s mines, with an average iron content of 62 percent or more compared with 40 percent or less in domestic pits. As such, it’s been able to displace costlier, lower-quality local product, especially as tightening pollution controls have increased the attraction of the better imported stuff.

The way China’s iron and steel data have been normalized over the past year suggests this process has further to run, especially as fixed-asset investment in the country’s steel industry has been booming this year. The world’s iron-ore miners have had a hell of a ride over the past decade. It ain’t over yet.

Comments