Column: Sulfur squeeze piles more pressure on Indonesian nickel sector

(The opinions expressed here are those of Andy Home, a columnist for Reuters.)

Surging sulfur prices, driven by the continued closure of the Strait of Hormuz, are starting to impact Indonesia’s giant nickel sector.

The world’s largest producer of the battery metal is heavily dependent on the Gulf for what is a core input for a significant part of its nickel processing capacity.

The sulfur squeeze adds spice to the Indonesian government’s own mix of measures designed to exert greater control over its runaway nickel production sector.

The country’s explosive production growth flooded the global market and cratered prices through 2024 and 2025.

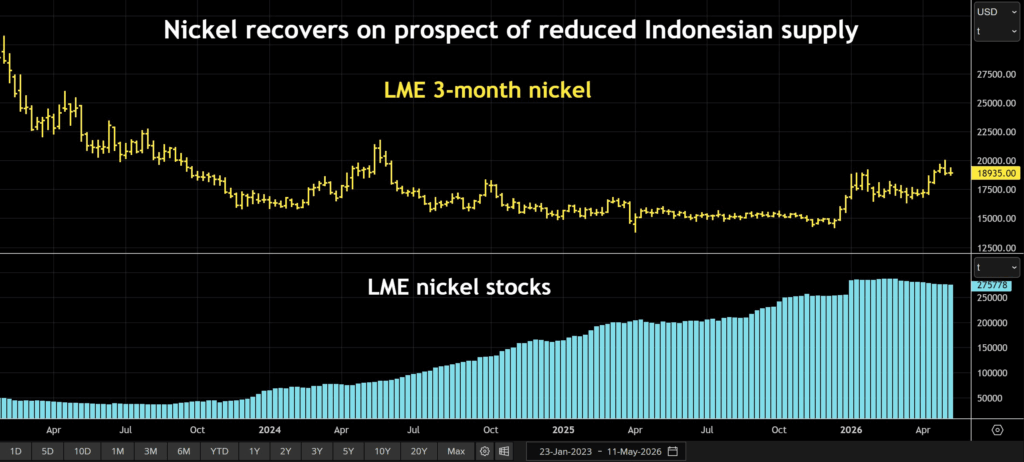

The prospect of lower Indonesian output and a corresponding shift in market balance has this month lifted London Metal Exchange (LME) nickel to its highest trading levels in two years.

War and politics

The Iran war has severely constrained the flow of sulfur from the Gulf, which accounts for around a quarter of global supply.

Indonesia relies on the region for 75% of its sulfur imports. Sulfur is converted to sulfuric acid for use by high-pressure acid leach (HPAL) nickel processing plants. They produce an intermediate product – mixed hydroxide precipitate – destined for the battery sector.

These HPAL plants are a fast-growing component of Indonesia’s production mix. Last year’s output of 450,000 metric tons represented over 10% of global production. Another 100,000 tons of new capacity is due to fire up this year, according to Macquarie Bank.

Or at least it was due to fire up.

The sulfur squeeze has already forced HPAL operators to trim production. Zhejiang Huayou Cobalt has halted half of its operating capacity.

It seems highly likely the next wave of capacity will be put on hold as even existing operators struggle to maintain run-rates.

The war’s sulfurous fallout has compounded the impact of tighter mine production quotas and changes to the government’s minimum selling price for nickel ore.

This year’s quotas of 260 million to 270 million tons fall far short of smelter requirements and are, on paper at least, sufficient to wipe out this year’s expected supply surplus, according to Macquarie Bank.

Meanwhile, the new formula for ore pricing pushes costs for HPAL producers up by more than $3,000 per ton. Combined with rising sulfur prices, break-even prices are now as high as $18,000 per ton, the bank estimates.

Tipping point

Indonesia’s nickel processors are facing multiple headwinds right now and analysts are starting to adjust their expectations of how much the country will produce this year and what that means for the pricing.

The International Nickel Study Group last month forecast the global market will shift from three years of massive supply surplus to a deficit in 2026.

The forecast shortfall of 32,000 tons is modest relative to last year’s calculated excess of 283,000 tons. But it marks a sharp revision from the Group’s October forecast of a hefty 261,000-ton surplus.

The Group cut its 2026 demand growth forecast from 6.2% to 4.2%. Global production, meanwhile, is expected to contract by 4.3% as Indonesian output growth slows sharply or even goes into reverse.

These forecasts, released on April 22, don’t explicitly reference the potential impact of a sulfur squeeze. But then few were expecting the Strait of Hormuz to remain closed for so long.

Recovery

Nickel prices have responded to the combination of rising costs and potentially reduced production in a country that accounts for 60% of global supply.

LME three-month nickel broke out of its previous range below $16,000 per ton in December as the market first started focusing on Indonesia’s intended cut in production quotas.

It hit a two-year high of $20,000 per ton last week and is holding around $19,000 this week, up 14.5% since the start of 2026.

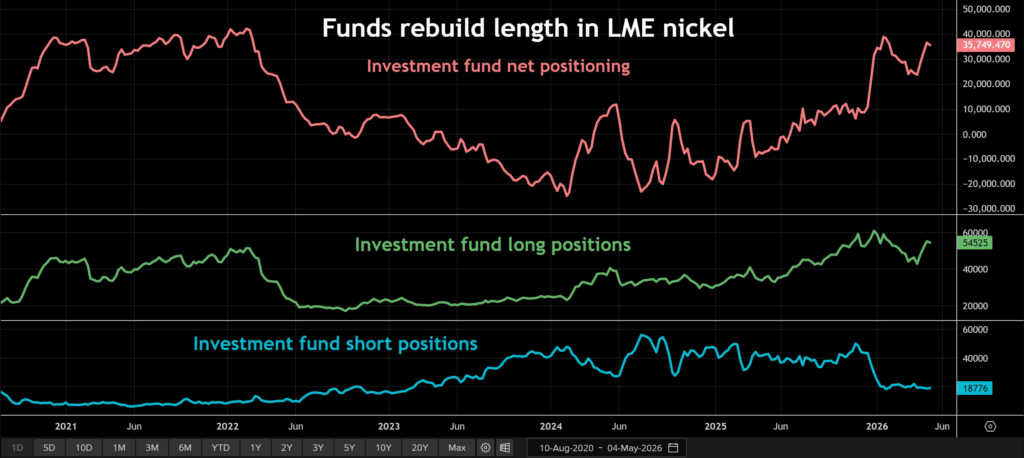

Investment funds have been building long positions over the same time frame. The collective bet on higher prices currently amounts to 35,750 contracts, equivalent to 215,000 tons.

That’s below the January peak but still higher than anything seen since 2022.

In essence, it is a bet that Indonesia stops flooding the market.

Were it just a case of government policy, that might be a risky proposition.

The mining quotas are subject to mid-year review and could be revised significantly higher. There is considerable push-back on both the quotas and the new ore pricing formula. Chinese operators, which dominate the sector, have formally complained to Jakarta, warning that further investment is at risk.

Further policy tweaking is entirely possible.

Jakarta, however, has no control over global sulfur availability. That is rapidly emerging as the single biggest threat to the world’s dominant nickel producer.

More News

Northern Star replaces CEO, activist investor Elliott wants more

July 01, 2026 | 08:29 pm

Ukraine urges swift publication of Irish investigation into alumina exports

July 01, 2026 | 01:22 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments