Column: Surging copper demand will complicate the clean energy boom

Copper is one of the essential elements of today’s economy, and tomorrow’s. It’s in the turbines and solar modules that generate electrons, the transmission and distribution lines that carry electricity to consumers, the home wiring that delivers it to dishwashers and iPhones, and the motors that move everything from elevators to electric bicycles.

I think of copper as a common carrier, so to speak, of decarbonization. It is literally the wiring that connects the present to the future.

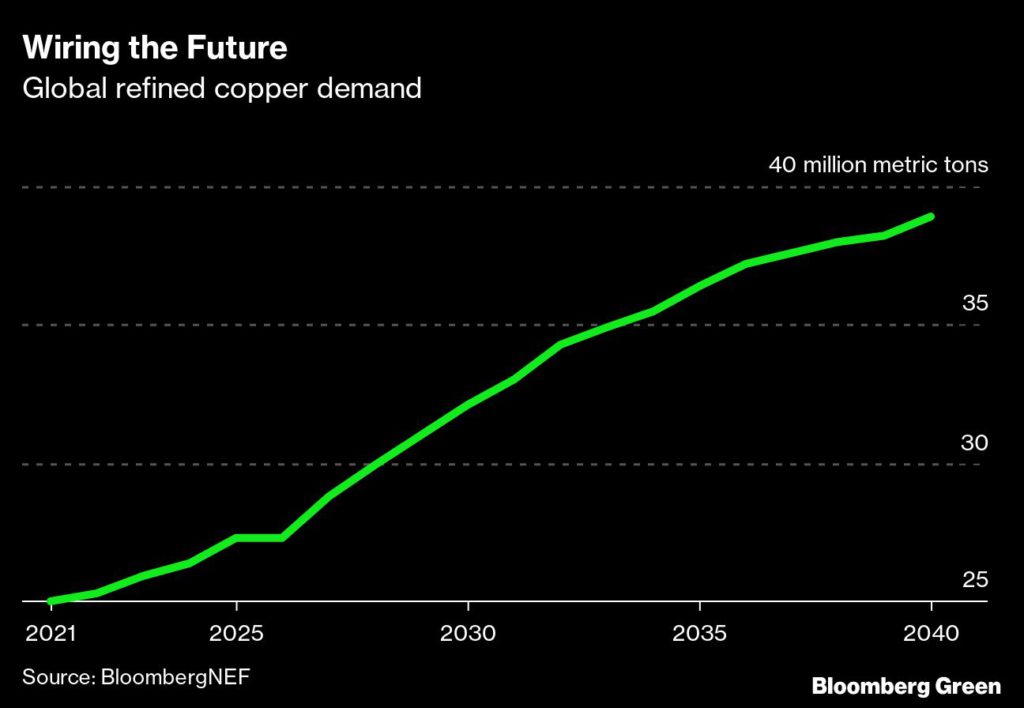

Energy research firm BloombergNEF recently published its first global copper outlook, factoring in demand from the technological changes needed to wean the economy off fossil fuels. Its topline finding is striking: Copper demand will increase by more than 50% between now and 2040.

Demand for copper relating to energy transition activities — clean power and electrified transport, and the infrastructure supporting them — will grow about 4% per year between now and 2040. Demand arising from traditional sources like construction and manufacturing of heating and cooling equipment will grow only 1.5% per year over the same period.

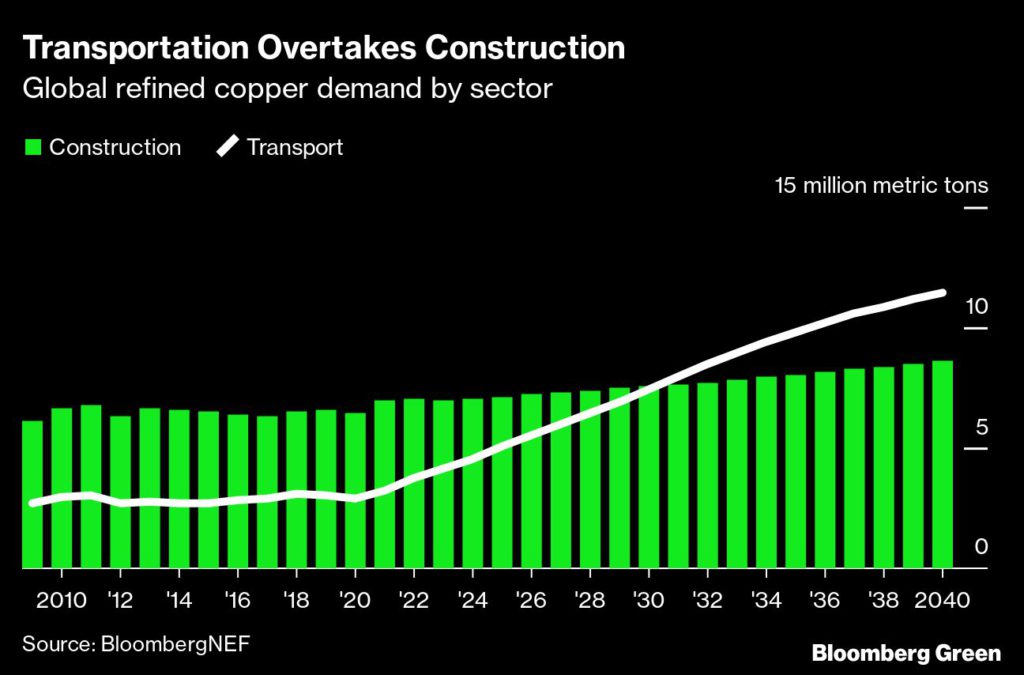

The result of this demand path is that by the end of this decade, transportation will replace construction as the biggest single driver. A decade ago, copper demand for transport applications was less than half of that in construction. By 2040, transportation demand will be one-third greater.

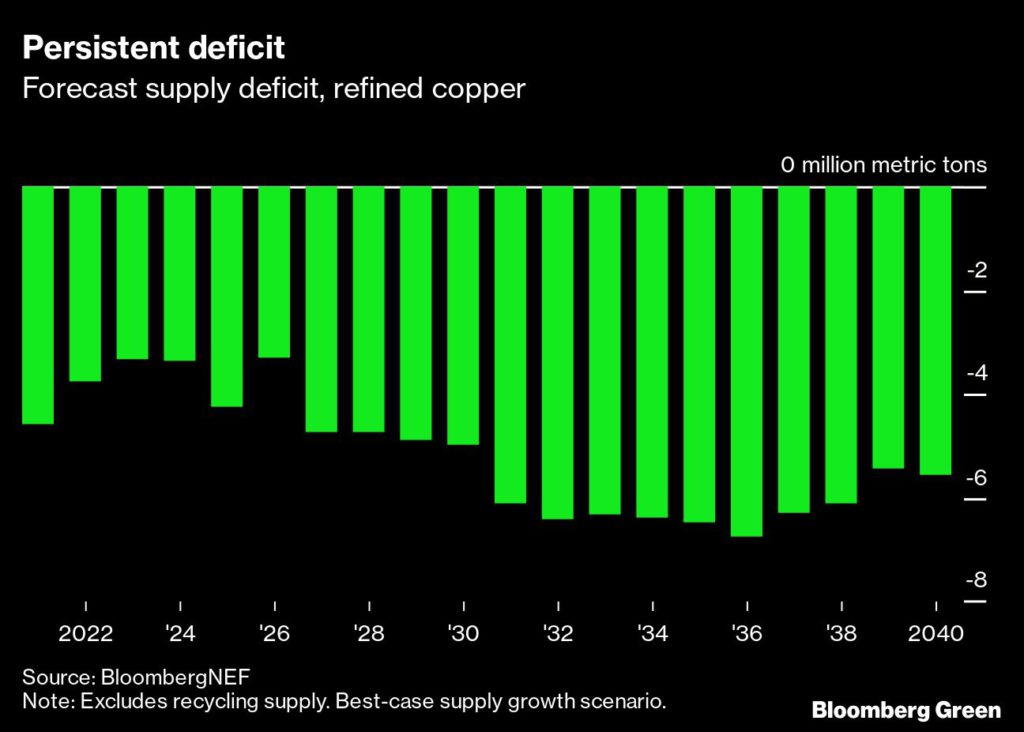

There is a challenge facing this growth trajectory, and it’s not so much acute as it is existential. BloombergNEF expects that primary copper production can increase about 16% by 2040. That increase, needless to say, is rather short of demand. By the early 2030s, copper demand could outstrip supply by more than 6 million tons per year.

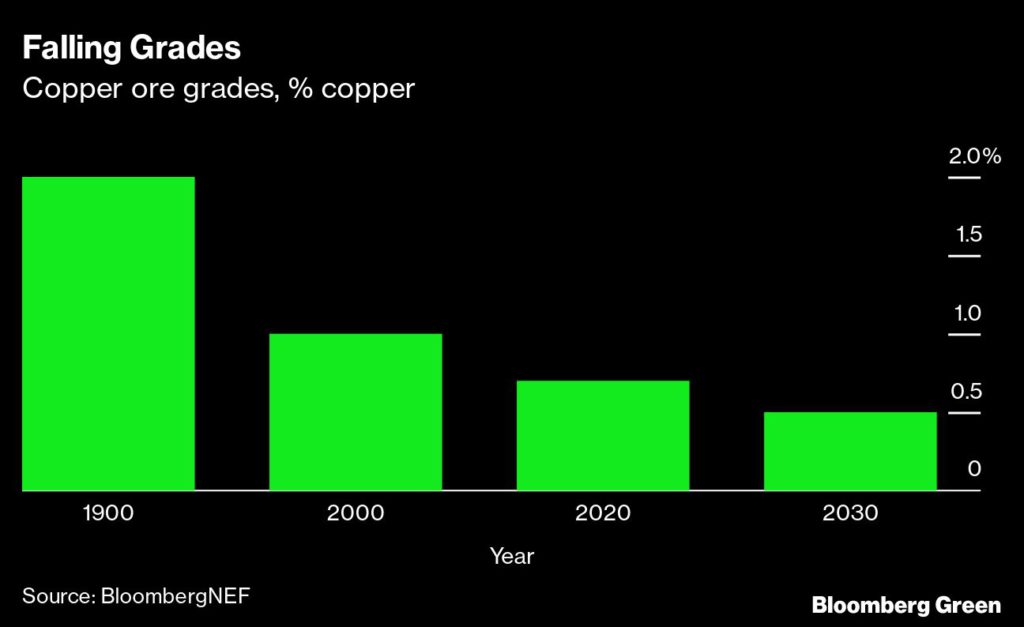

There will be new primary production, but a copper mine is not quick-ramping. In fact, no new copper discoveries are expected to be operational in the next three years. And while global copper supply is not exactly tapped out, miners now use ore grades of 0.5% copper, a quarter the concentration of a century ago.

But this doesn’t mean that the world needs to be structurally short of copper for two decades. For one thing, a shortage leading to high prices could suppress demand, which would reduce the supply deficit. That would happen, however, at the expense of expansions of clean power and electrified transportation.

Also, copper’s very clear demand trajectory should encourage more discovery and exploration. It’s not just companies that will be interested — governments will be too, given the possibility of mining royalties. If a government facilitates mine development with rigorous environmental standards, that’s encouraging. If their royalty ask is too high, it could dampen investor and developer confidence in new production.

Then there is secondary production, or recycling. At the moment, secondary production meets the entirety of the 4.6 million-ton-per-year gap between primary production and demand. Industrial copper scrap is readily available, but consumer scrap is hard to predict and therefore harder to rely on. Today, the copper collection rate for consumer and electronic goods is only 53%.

In order to meet the surge in demand, supply from new mines (regardless of ore quality) and recycled sources (regardless of how efficient they might be) will both be needed. The biggest impetus for more supply is demand itself. And the signal from global efforts to decarbonize economic activity is very clear.

(By Nat Bullard)

More News

Northern Star replaces CEO, activist investor Elliott wants more

July 01, 2026 | 08:29 pm

Ukraine urges swift publication of Irish investigation into alumina exports

July 01, 2026 | 01:22 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments