Tin use stable to slightly stronger by year-end, ITRI Survey shows

ITRI’s twelfth annual survey of tin users gathered data from tin users worldwide between June and August 2016. ITRI analyst Peter Kettle commented: “Generally companies appear a little more optimistic about sales in 2016 than they were at the time of a snap survey carried out late last year. Allowing for a recent strong recovery in the China solder market it looks like global refined tin demand could increase by a little over 1% this year.”

129 companies took part in the survey, accounting for some 45% of estimated global refined tin use in 2015.

Key findings of the survey are:

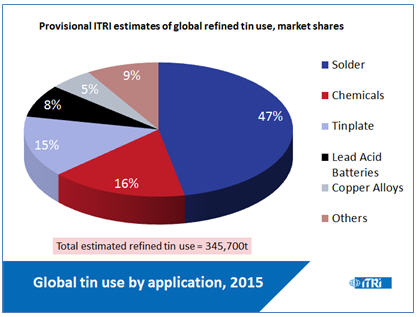

- ITRI’s latest estimate of refined tin use in 2015 is 345,700t, based on data from the 2016 survey. Refined tin demand reported by survey participants contracted in 2015 but is expected to remain static or improve slightly in 2016.

Solder still accounts for the largest global share of tin use although 2015 use was the lowest for a decade. Producers reported on a tough year and several were concerned about threats from miniaturisation and solderless technologies. Automotive and industrial uses are growing, and powder and paste production in China is set to increase.

Solder still accounts for the largest global share of tin use although 2015 use was the lowest for a decade. Producers reported on a tough year and several were concerned about threats from miniaturisation and solderless technologies. Automotive and industrial uses are growing, and powder and paste production in China is set to increase.- Regulatory issues continue to be the key concern in chemicals markets, though major PVC stabiliser producers outside China are positive about market growth in 2016. Markets for inorganic products remain flat. Excess tinplate capacity in China is a concern. Recent rapid growth of tin use in lead-acid battery grids has slowed in China due to overcapacity, market saturation of e-bikes and early competition from lithium-ion batteries.

- Total global tin use including refined and unrefined forms is provisionally estimated at 420,400 tonnes in 2015. The Recycling Input Rate (use of recycled tin in all forms as a proportion of total usage) for the year was calculated at 31%, down from 33% in 2014. This percentage has generally risen over the last decade, with dips largely corresponding to periods of lower tin prices.

- From analysis of refined tin stocks reported by participants, it appears that pipeline stocks held by tin users have fallen by about a third, or over 10,000 tonnes, over the last 5 years to an estimated 21,000 tonnes.

About ITRI:

ITRI is the world’s foremost authority on tin with over 80 years’ experience in tin related technologies. It is a membership based organisation representing major tin producers and smelters and is the premier source of tin related information. ITRI has specialist knowledge of tin use in all the major sectors as well as groups responsible for technology, statistical and market information, regulatory affairs and sustainability. It provides links to the main tin consuming sectors through a substantial network of industry contacts. The organisation hosts seminars, conferences and industry-specific group meetings. It also provides marketing and technical support to its members and the tin industry in general. Further information can be obtained from ITRI (http://www.itri.co.uk)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments