Why 11 of the largest gold funds and majors are all invested in this junior gold company

Investor #1 is a mining company led by two of the biggest names in finance – billionaire Ned Goodman and mining mogul Sean Roosen.

Investor #2 is a resource fund that has outperformed the TSX Venture by over 60% since its inception in December 2013.

Investor #3 is a C$600 million behemoth on the cusp of becoming the North America’s next significant gold producer.

All three are the largest investors in IDM Mining (TSXV:IDM), a company we believe will be a market darling in 2016.

So why are you still on the sidelines?

IDM Mining, led by Robert McLeod, is the little engine that could. Persevering and advancing in even the most tumultuous bear market, IDM is now in the home stretch. In March of this year, the company announced it was looking to raise $7.5 million to get its 100%-owned Red Mountain project to feasibility. But due to enormous demand, the financing was boosted to $10.84 million – as the popular adage in mining goes, “friend or foe, take the dough.”

When we interviewed IDM’s keystone investors, a common theme was apparent. The Red Mountain project was one of the most technically appealing projects in the world, not to mention its enormous ‘blue-sky’ potential.

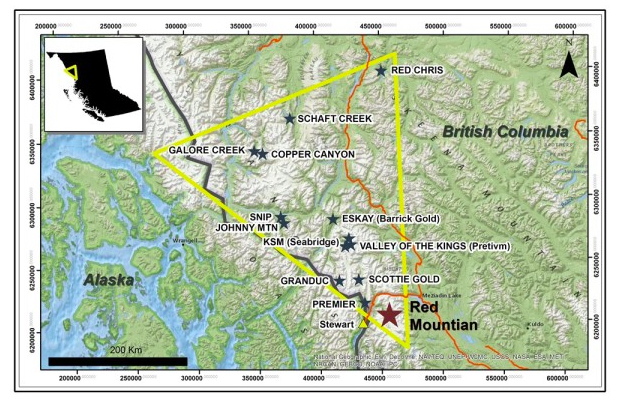

Located in the red-hot ‘Golden Triangle’ of northwestern British Columbia, the project spans over 42,000 acres and is nestled in mining-friendly Nisga’a traditional territory. It is situated 15 kilometres northeast of the town of Stewart, where Rob McLeod was born a third-generation miner. But, most importantly, Red Mountain shares an area code with the likes of Seabridge Gold’s (TSX:SEA) KSM Project and Pretium Resources’ (TSX:PVG) Valley of the Kings Deposit. Both projects host very large previous metal deposits in the same belt of rocks as Red Mountain.

“The Fundamentals Speak For Itself”

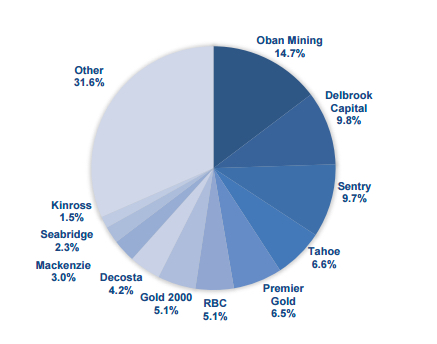

Oban Mining (TSX:OBN) is IDM’s largest shareholder, owning 19.9% of the shares outstanding. It is a mineral exploration company focused on the acquisition, exploration, and development. The company was formed by the same team that built and sold Osisko Mining for $3.9 billion.

From the get-go, Oban’s mandate was to grow the company to a point where critical mass was achieved in terms of owning gold resources and high-potential gold deposits. Following its last transaction in March 2016, Oban owns 5.8 million ounces of gold resource and has completed 15 transactions since its inception.

Oban Mining became involved with IDM back in December 2015, when it invested $1 million in a private placement for 20% of the company. To sweeten the deal, Oban also threw in its portfolio of Yukon assets; properties it acquired from Ryan Gold during a four company merger at its inception. The deal made sense to both sides, Oban bringing its technical expertise to the table, while unloading its shelved Yukon assets to Rob McLeod. Rob made a name for himself as the VP Exploration of Underworld Resources developing the White Gold discovery; a company sold to Kinross for $139 million in 2010 and igniting another Gold Rush in the Yukon.

When we inquired to Oban what was so appealing about IDM, we received a very simple answer: the project’s fundamentals speak for itself. Oban touted the after-tax IRR of over 25%, and maintained that the investment decision was based on current economics alone.

In an updated PEA released in July 2014 that utilizes $1,250/oz gold, Red Mountain yields an after-tax NPV C$57.6 million, after-tax IRR of 32.9%, and a payback of just 1.5 years! The fact that Red Mountain has incredible exploration potential and no significant work since 1996 is the icing on the cake – the blue sky potential.

Retreating Bromley Glacier resulting in newly exposed bedrock.

We asked Oban if it planned on acquiring the rest of IDM Mining, an idea that has been kicked around but Oban maintained near-term acquisitions will take a backseat while it concentrates on progressing its 100% owned Windfall Lake and Marban projects. It appears the internal price target for Oban is C$3.00, meaning it will be remain a long-term shareholder for the time being. After that, we would expect Oban to be a serious suitor. In the meantime, Oban ensured it maintained its significant holding of IDM by investing in the most recent private placement.

“Quality Asset. Successful And Efficient Management Team”

Delbrook Capital is a Vancouver-based alternative investment hedge fund that focuses on the identification of catalyst-driven investment opportunities in the resource sector. Delbrook’s foray into IDM was a bit more traditional. Delbrook purchased $1.0 million, or 7,142,857 in Flow-Through Units, and another $150,000 in Hard Units, in a financing in June of 2015. The fund maintained its position by also participating in the most recent financing.

We spoke with Delbrook and while they do not comment on specific investments or trading decisions, they did give us an overview of what they look for in an investment. This was more than enough to fill in the blanks to why IDM Mining was an attractive investment.

Delbrook is looking for companies with quality assets and a balance sheet to drive catalysts. They utilize an in-house team of technical veterans to scour the world for undervalued opportunities, with emphasis on quality over anything else. Delbrook is an active investor; they are a reporting issuer to over a dozen companies, plus investors in numerous other companies. Thus, they are hands on and utilize their entire arsenal to generate value. This includes fronting their technical expertise, bringing more capital to the table, or working with or shaking up the board of directors.

At this point we understand that Red Mountain is a technically and economically sound project. But what about the management team? Delbrook says they look for teams that understand capital efficiency and to leverage these efficiencies to stretch the dollar.

Rob took over as the CEO and President of IDM Mining, (at the time called Revolution Mining), in October 2013, prior to which he served as the VP of Exploration. He inherited a portfolio of gold projects in Carolina Slate belt and copper-gold targets in the Sierra Madre, Mexico, all of which were floundering and uneconomic in the given environment. With only C$300,000 in cash to work with, Rob realized to survive as a company, IDM Mining needed to pivot hard.

Rob went into action and inked an option agreement with Seabridge Gold to earn 100% of the highly sought after Red Mountain project. The deal included paying C$2 million cash (C$1 million within 90 days and C$1 million within 1.5 years), issuing 29.7 million shares (5.3 million post roll-back) to Seabridge, and spending C$7.5 million in exploration over a period of three years. The company was rolled back six to one, and in the hardest of settings, Rob scrounged up C$2.8 million to finance the first cash payment and to begin work on Red Mountain.

Prior to the recent raise of C$10.84 million, Rob had raised close to C$9.4 million. He paid Seabridge C$2 million in cash and another C$5.0 million in property expenditures. That’s 70% of the funds raised dedicated to progressing Red Mountain, plus cleaning up the balance sheet and grandfathered assets from the Revolution days. All this in less than two years. If this is not capital efficiency, we do not know what is…

Premier Gold (TSX:PG) – The Next Mid-Tier Producer

Enter one of IDM’s newest major shareholder – Premier Gold, a Canadian-based exploration company focused on exploring for and developing gold deposits in North America. Premier Gold entered the foray by an investment of C$1,282,500 for 14.25 million units, or 6.49% of IDM’s common shares outstanding.

Premier’s principal projects include: 50%-interest in the Trans-Canada Property located in the Geraldton-Beardmore Greenstone Belt in Ontario; 100%-interest in the McCoy-Cove Project located in Lander County, Nevada; and a 40%-interest the South Arturo Mine, located in Elko County, Nevada.

Premier has always been the perpetual exploration and development company. Since its inception in 2006, the company has amassed an impressive portfolio of assets; however, never achieved actual production. That is, until now – 2016 will be a banner year for Premier as the company expects to net ~80,000 ounces of gold production from the South Arturo project in Nevada.

Premier’s President and CEO, Ewan Downie, will finally achieve what has alluded him for so long. And all it took was a $20 million payment and transfer of 5% of its Rahill-Bonanza stake in Northwestern Ontario for 80,000 ounces in 2016, or an expected free cash flow of $40 million. Definitely not a bad return, especially with Barrick doing all of the work.

Unfortunately, this new found production can be short-lived. The mine life of South Arturo is less than three years, then Barrick and Co. will be processing heap leach ore that will take cash flow to 2022, however, at significantly lower ounces. Don’t get us wrong, the mine life will be extended as the current pit (phase 2) has underground potential that is currently being permitted; plus phases 1 and 3 which will be the focus of the 2016 program with the emphasis on defining economics and metallurgy. However, we imagine the investment into IDM is for Ewan to hedge some risk for a very cheap price.

Premier Gold’s flagship asset is the Trans-Canada Joint Venture located in Ontario. The project is made up of several claims and have a cumulative length of more than 100 kilometres – a district play that already has 4 million ounces of M&I gold. Premier signed a transformative deal with Centerra Gold in early 2015 and wasted no time, drilling 17,500 meters over 62 holes, gaining a better understanding of the distribution and grade of the gold mineralization within Hardrock. A feasibility study is expected for Q3 2016 with Federal and Provincial Environmental Assessments submitted at the same time.

We believe any sort of production from Trans-Canada is long ways away. There are still a lot of obstacles in the way, but most importantly, the size of the project will dictate a huge price tag. The markets are warming up but the cost of capital is still very high. For Premier Gold, there will be nothing worse than finally becoming a producer and achieving the cash flow premium, only to have it taken away. That being said, Premier’s technical team, along with many others, must believe IDM will become a producer by mid-2018 because IDM itself definitely does not fit the standard mold of a Premier Gold project.

IDM Funded Through To Construction Decision

There you have it, three cream of the crop players in their respective fields, believing in IDM Mining and Rob McLeod. But wait, that’s not even all of them.

Almost 70% of IDM’s stock is now in the hands of either an institutional fund or a household name in mining. Here at Palisade Global, we have done our due diligence. In fact, we have participated in the last three private placements. Seeing the other names involved not only confirms our fundamental investment thesis, but also gives a pat on the back to our technical team, who pointed out Red Mountain a lot earlier than the bigger players.

Now that IDM is funded all the way to a construction decision, or mid-2017, we can sit back and watch Rob knock down the hurdles as they come. And that means plenty of catalysts on the horizon to propel the stock higher as the project de-risks. Next stop includes a resource update towards the end of Q3 2016, and a feasibility study by the end of the year. Permitting should take until mid-2017, and if all goes well, construction will also begin around that time. Finally we have commercial production set for Q3 2018. We believe in Rob and Red Mountain!

More News

BHP seeks to restart Cerro Colorado mine with $1.5B investment

The copper mine has been closed since late 2023 after it was denied its water permit.

July 02, 2026 | 10:43 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments