Zinc’s bull narrative blurred by fog of LME spreads war

(The opinions expressed here are those of Andy Home, a columnist for Reuters)

LONDON, Oct 18 (Reuters) – Zinc hit a 10-year price peak of $3,308.75 a tonne on the London market this month but on Wednesday London Metal Exchange (LME) three-month metal touched a low of $3,040 after a precipitous 3.1 percent slide the previous day.

With further upside barred by profit-takers and producers’ forward selling, investors have scrambled for the exit.

They have also been spooked by some strange goings on in LME warehouse stocks. The previous long-running downtrend has been brought to an abrupt halt.

Zinc has been flowing into LME sheds daily for the past two weeks, with the surge totalling 31,850 tonnes so far. Headline inventory of 271,250 tonnes is back at July levels.

Today’s LME stocks report also showed 61,100 tonnes of “reverse cancellations” — zinc that had been earmarked for physical load-out being delivered back into the system.

Live “on-warrant” stocks in the system are now at 205,350 tonnes. That level hasn’t been seen since February.

This hasn’t helped the bull cause.

Analysts were already fretting about the supply response to stratospheric prices and the whole market is acutely aware that it is almost two years since Glencore mothballed half a million tonnes of zinc mine production when the price bombed out below $1,600 a tonne.

But LME zinc stocks are not telling us anything about the market’s underlying dynamics. They are, rather, the smoking evidence of a ferocious spreads battle on the London market.

Graphic on LME Zinc spreads (Image courtesy of Reuters)

Does it hurt yet?

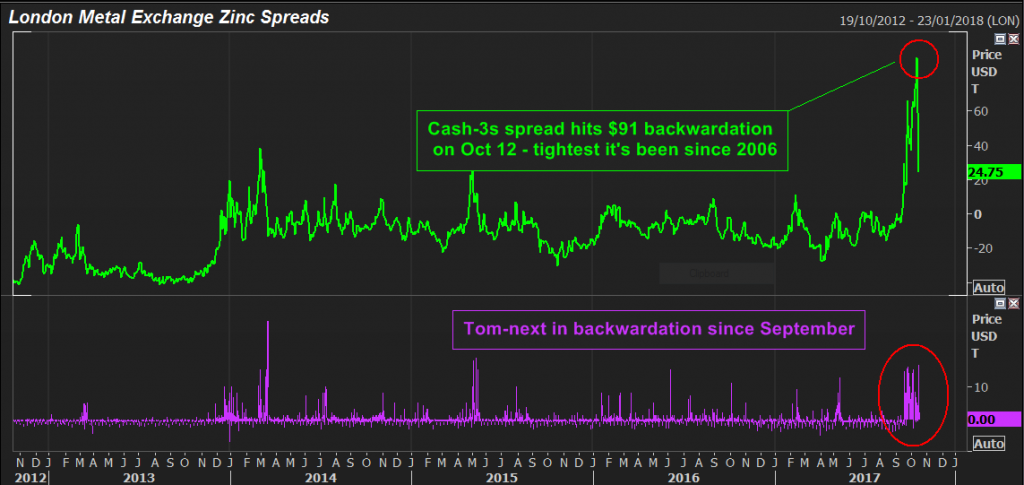

LME zinc time-spreads went wild at the end of September and turned ferocious last week.

The cash-to-three-months period was valued at a backwardation of $91 a tonne on Oct. 12, the highest cash premium in a decade.

That benchmark spread, however, masks a multitude of pain for holders of short positions across the multiple prompt dates traded in the London market.

The cost of rolling a position overnight, “tom-next” as it’s known on the LME, has touched $15 a tonne on several occasions in recent days.

The whole zinc curve has been trading in steepening backwardation as shorts have scrambled away from the cash squeeze on the front part and forward selling by producers on the longer-dated part.

Amid this turbulence has been the constant of the dominant position holder that has been gracing the LME’s daily market reports for many days.

At last Friday’s close, the entity held more than 50 percent of on-warrant zinc stocks and more than 90 percent including cash positions.

That has been punishing short-holders, limited only by the restraints of the exchange’s lending rules.

Not everyone has simply paid up, it seems. Those big stock movements, both inflows and “reverse cancellations”, have been timed around this week’s third-Wednesday monthly prompt date.

Last month’s sudden appearance of 28,425 tonnes of zinc at LME sheds in Antwerp was a taster of the most recent 31,850-tonne flow onto warrant in New Orleans, also the location of today’s mass re-warranting.

Neither the inflow nor the location should be surprising.

Faced with a running cash date squeeze, those who have physical metal will often deliver against their shorts rather than pay the price of rolling.

New Orleans, which has for years held the bulk of LME zinc stocks, has been characterised by massive rotations of metal between on-and-off market storage. That there should be “invisible” stocks in the U.S. port shouldn’t surprise.

Battle over?

The combination of spread stress and large flows of metal in the LME system suggests we’ve just witnessed a big bear-bull battle among physical players — one that has in all probability resulted in a significant change of stock ownership.

Is it over now?

Certainly, today’s reported 875 tonnes of LME zinc inflow was the smallest in the most recent series.

Zinc time-spreads have also loosened up a lot over the past day or so as on-warrant stocks rebuild. Cash-to-threes, for instance, was valued at a backwardation of “just” $24.75 at Tuesday’s close.

As today’s prime prompt date passes, the signs are that things are going to calm down a bit.

But if this was a physical metal grab, what has appeared in the system may not stay too long. Even factoring in the inflows of the past two months, headline LME stocks are still down by 156,600 tonnes on the start of the year.

The LME squeeze, meanwhile, may also have been a factor in the rapid stocks drawdown in the CME warehouse network.

Although trading activity on the CME zinc contract is minimal, there were more than 22,000 tonnes of metal in CME-registered sheds in May.

There are now only 5,168 tonnes, with more than 9,000 tonnes departing New Orleans warehouses over the past two weeks.

Meanwhile, stocks of zinc registered with the Shanghai Futures Exchange currently total only 68,102 tonnes, down by 84,722 tonnes since January.

Combined exchange stocks have fallen by a net 1,920 tonnes this month, LME turbulence notwithstanding, and are down by 248,500 tonnes on the start of the year.

The bigger picture remains one of low visible stocks. And availability of “invisible” stocks has just been severely tested with “only” 31,850 tonnes drawn into the LME system.

The supply chain still looks stressed and, while it remains so, there’s a good probability of more physical showdowns on the LME trading floor.

Blurring the picture

These big shifts of metal around the LME warehouse system have, however, blurred the previous bull market narrative.

Zinc’s extraordinary price gains this year were accompanied by a reassuringly constant downtrend in LME stocks.

LME inventory is only one part of the global stocks puzzle, but it is one that resonates loudest with investors and even with automated trading systems.

There are good reasons for caution on zinc’s prospects after its near 30 percent price surge this year.

Will such price volatility cause demand destruction, particularly in the zinc alloy diecasting sector?

Will miners over react in bringing on new supply to cash in on bonanza prices?

And when will Glencore bring back its mothballed production?

All good questions but none to which LME zinc stocks can provide the answer.

What they do signal, however, is that whoever was long on LME zinc is probably a lot longer now.

(Reporting by Andy Home; Editing by David Goodman).

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments