Australia govt’s lithium price outlook is bleak

Despite the lofty expectations for demand from electric vehicles where lithium-ion batteries dominate, prices for the raw material have been in relentless decline for the last 18 months.

Free-on board prices of lithium carbonate from South American brine ponds are down 27% over the past year to average $11,500 a tonne in June, according to Benchmark Mineral Intelligence data. Ex-works prices in China have collapsed from a peak of $24,750 in March last year to below South America export prices.

Producers in Australia now get $300 less for spodumene concentrate (6% lithium used as feedstock for lithium hydroxide) cargoes than in July last year, when prices were above $900 a tonne, according to Benchmark’s June assessment. Lithium hydroxide prices followed carbonate down, but now trade at a premium to the latter at over $13,000 inside China.

Thanks to a slew of new hard-rock lithium mines and expansions at existing operations in Western Australia, the country is now the number one producer of the white metal.

Map of major producing mines and mine development projects of minerals used in Lithium Ion Batteries. Commodities include Lithium, Graphite and Cobalt. Map includes locations of 240+ producing mines, 45 development projects, 110+ projects in economic assessment, and 40 suspended mines.

New supply coming on stream over the next couple of years – thanks in large part from the expansion of Greenbushes, the world’s largest lithium mine – is also dominated by Australia.

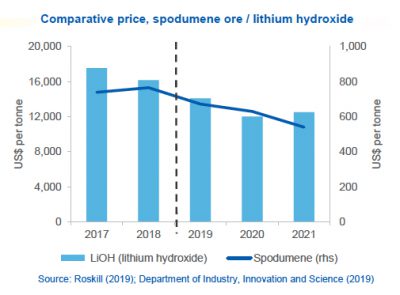

In a new report by Australia’s Department of Industry, Innovation and Science predicts continued decline in the price of lithium hydroxide as spodumene pre-cursor material floods supply chains in China and Europe.

Lithium hydroxide prices are projected to fall by around 15 per cent in 2019, as oversupply persists and inventories grow. Over the outlook period, the supply surplus is projected to gradually close, with the price expected to start turning around after 2020.

Spodumene ore is expected to face a longer period of oversupply, with prices remaining soft through 2021.

The fact that supply is being triangulated against future demand makes it somewhat unlikely that oversupply will correct in the very near future. However, demand growth is likely to outstrip supply by around 2023.

The build-up of stocks worldwide in anticipation of the dozens of so-called gigafactories (named after the Tesla facility in Nevada) being built around the world must be particularly worrying for lithium price bulls.

The office of Australia’s chief economist predicts a 26+% increase in stockpiles worldwide, representing 2-and-a-half years of consumption.

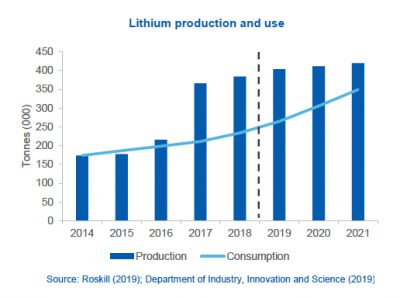

According to the study, the ramp-up in electric vehicle and battery facilities is projected to lift lithium demand from 234,000 tonnes in 2018 to more than 349,000 tonnes by 2021.

Currently, less than half the lithium produced around the world ends up in rechargeable batteries.

More News

Zimbabwe lab sees regional gold hunt accelerate as prices soar

July 03, 2026 | 11:49 am

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

John Smith

The lithium demand is less as compared to the supply of it. As per the latest lithium stock news Lithium prices during 2018 suffered heavy losses so the lithium stocks have been suffered. Various lithium companies in Australia has released their research and study for disruptive technologies to furnish the lithium battery industry with ethical and sustainable supply solutions.