Canadian economy won’t feel impact of battery metal mining

Hardly three years ago expectations of a demand boom for battery materials used in electric vehicles (EVs) and energy storage reignited interest in the mining sector as the China-induced supercycle in commodities demand started levelling off.

Prices for lithium and cobalt soared (only to fall back again). Same for vanadium. Graphite and rare earth prices made a comeback. Nickel, where EV-related demand is still tiny, was caught up in the euphoria, and the primarily steelmaking metal is holding onto those gains and more.

Longer term mining’s bellwether metal – copper – may benefit the most and aluminum (on a dollar-basis a bigger industry than copper) will feel a sizeable impact.

A new study by Moody’s Investor Services expects “metals consumption for battery electric vehicles (BEVs) will rise sixfold from current levels, as EV penetration reaches 8% of total car sales (our base scenario) by the mid-2020s, and continues to rise rapidly in the second half of the next decade.

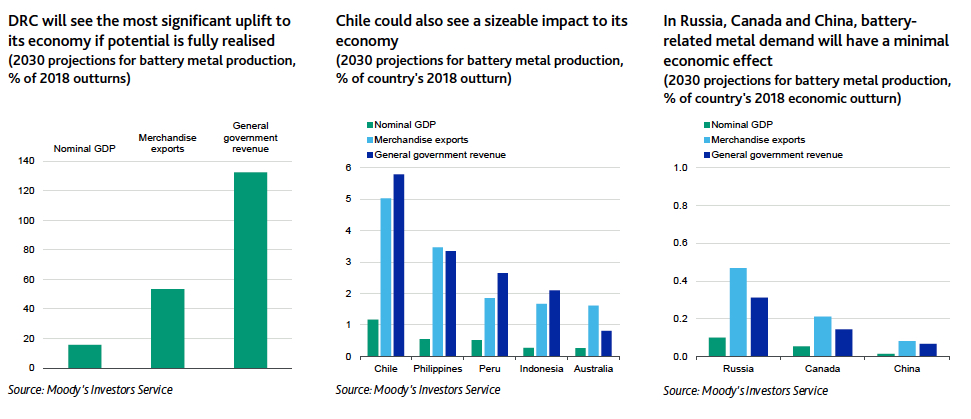

But on a country-wide basis the increased output of battery materials – specifically lithium, cobalt, nickel and copper – probably won’t be felt, at least not in the developed world.

According to the authors, of the top battery metals supplying countries, the economy of the Democratic Republic of the Congo could be utterly transformed, Chile and other developing nations would enjoy a significant boost, and Australia’s coffers would fill up nicely.

But, says Moody’s, among the top suppliers , Russia, Canada and China would remain largely untouched:

Given the sheer size of their economies and government budgets and relative diversification of economic activities, we expect Canada, China and Russia to be the least impacted by higher demand for BEV metals.

Future value estimates of metal production do not exceed 0.5% of 2018 nominal GDP, merchandise exports and general government revenue by 2030 (and would be smaller in relation to the 2030 size of these economies and their governments’ budgets).

Nevertheless, these countries will continue to contribute significantly to the supply of these metals indirectly, through companies investing domestically and overseas.

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments